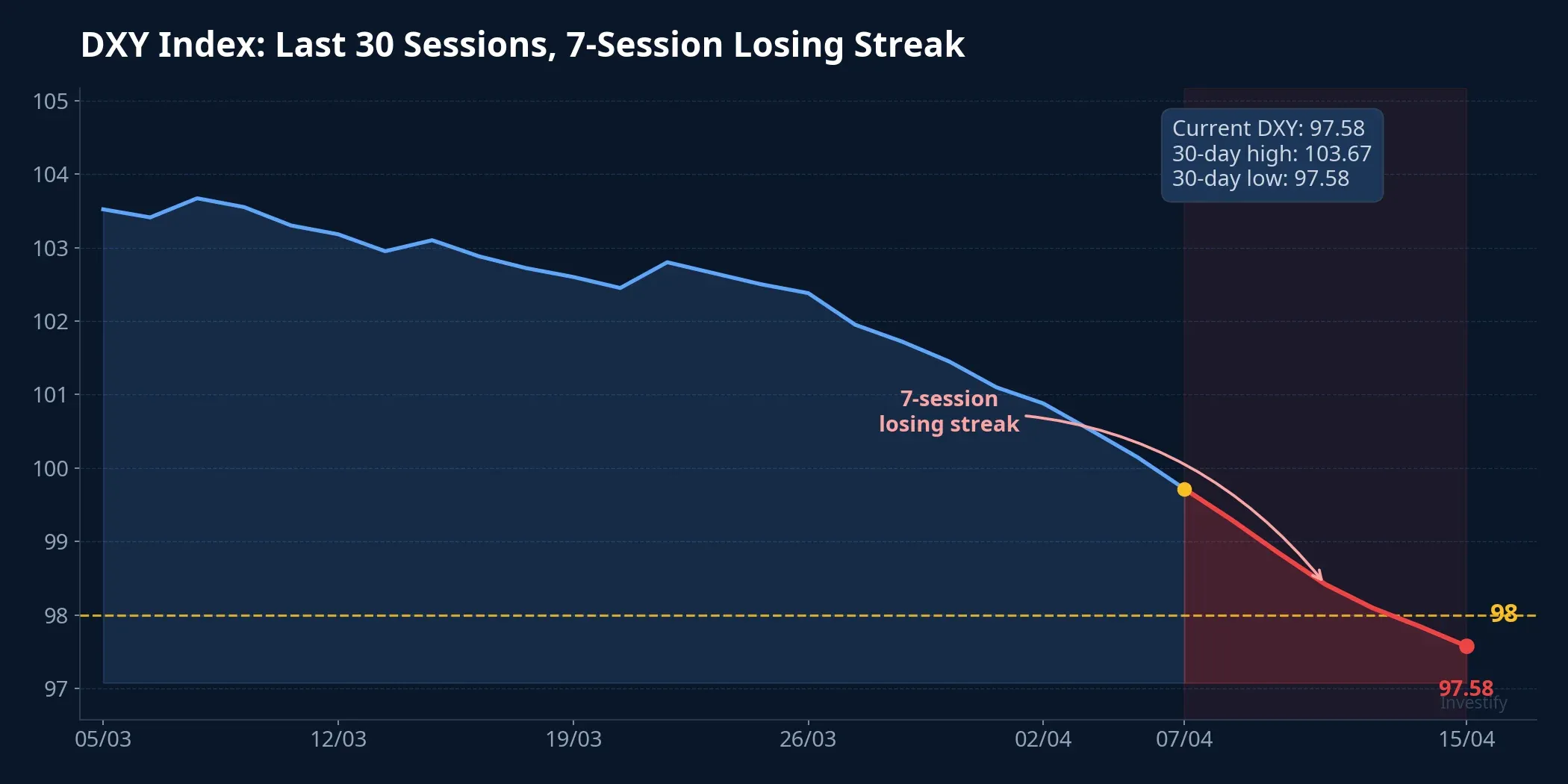

The US Dollar Index (DXY) has just experienced a seven-session losing streak, falling to around 98 points — its lowest level since late February.Trading Economics This is no ordinary technical correction. Three forces are simultaneously weighing on the greenback: an escalating trade war, rate-cut expectations, and most critically, a crisis of confidence in the Federal Reserve’s independence.

The big picture reveals this isn’t merely a domestic American issue. Given the central role of the USD in the global financial system, every signal of eroding independence at the world’s most powerful central bank transmits directly to exchange rates, capital flows, and the cost of capital in emerging markets, including Vietnam.

From Verbal Attacks to Criminal Investigation

The relationship between President Trump and Fed Chair Jerome Powell has been strained for years, but the recent escalation exceeds all precedent.

In July 2025, Trump told a group of Republican lawmakers in the Oval Office that he would fire Powell “soon.”ABC News He later walked it back, calling it “highly unlikely.”NBC News In late December 2025, Trump called Powell a “fool” and accused him of “gross incompetence.”Fox Business

But the most serious escalation came in January 2026, when the Department of Justice under federal prosecutor Jeanine Pirro opened a criminal investigation targeting Powell over his congressional testimony about the Fed headquarters renovation project.Al Jazeera Judge James Boasberg subsequently quashed the subpoenas, finding “abundant evidence” that the primary purpose was to pressure Powell into complying with the president or resigning.CNBC

Former Fed Chair Janet Yellen warned this was the “road to a banana republic.”Talk Business She called the Powell probe “extremely chilling” for Fed independence.CNBC

DXY Down Approximately 2%: Three Converging Forces

Over eight trading sessions (April 7-15), the DXY fell from approximately 100.08 to around 98.09 points — a decline of roughly 2%. The magnitude isn’t particularly dramatic, but the consistency of the streak and its context make it noteworthy.

First, the trade war. Escalating tariff policies are eroding confidence in the US economic outlook, gradually shifting international capital flows away from USD-denominated assets.

Second, rate expectations. Markets are pricing in Fed rate cuts in the second half of 2026. Lower rates mean reduced attractiveness for USD-denominated assets.

Third, and most importantly: confidence in Fed independence. When the president openly threatens to fire the central bank chair, international investors begin questioning whether US monetary policy will remain data-driven or serve political objectives. Deutsche Bank warned: if Fed independence is seriously compromised, “both the currency and the bond market could collapse.”Yahoo Finance

An important distinction: these three factors are converging simultaneously, but the precise contribution of each to the current DXY decline is difficult to isolate. Markets are reflecting all three at once, not just the Fed story.

30-Day Countdown: Who Will Lead the Fed?

Powell’s term as Fed Chair expires May 15, 2026, though he retains his seat on the Board of Governors until January 2028.Federal Reserve He has not indicated whether he will remain at the Fed after his chairmanship ends.

Trump’s nominee to replace Powell is Kevin Warsh, a former Fed Governor from 2006-2011. Warsh recently filed financial disclosures showing estimated personal assets of $135 million to $226 million — far exceeding any previous Fed chair.CNBC His confirmation hearing is scheduled for April 21, 2026 before the Senate Banking Committee.CNBC

However, Warsh’s path is far from smooth. Republican Senator Thom Tillis has vowed not to vote for any Fed chair nominee until the DOJ drops its investigation of Powell.CNBC The committee has 13 Republican and 11 Democratic seats — a single Republican defection is enough to block the nomination. If Warsh isn’t confirmed before May 15, the question of who leads the Fed during the transition becomes a complex legal puzzle.

Historical Precedent: Consequences Are Always Severe

Political pressure on central banks is not new, and history shows the consequences are always significant.

Nixon 1971: President Richard Nixon pressured Fed Chair Arthur Burns to keep rates low before the election while closing the “gold window” — ending the gold standard. The result: US inflation exceeded 12% in 1974 and persisted throughout the 1970s.

Erdogan 2019-2021: Turkish President Erdogan fired three central bank governors in two years for refusing to lower rates. The result: the lira lost over 80% of its value against the USD from 2018-2023, with inflation exceeding 85%.

The critical difference in the current case: scale of impact. The USD accounts for approximately 58% of global central bank foreign exchange reserves. A crisis of confidence in the Fed would propagate across the entire international financial system — from US bond yields to exchange rates in emerging economies.

Impact on Vietnamese Investors

USD/VND: Stable but Risk Lurks

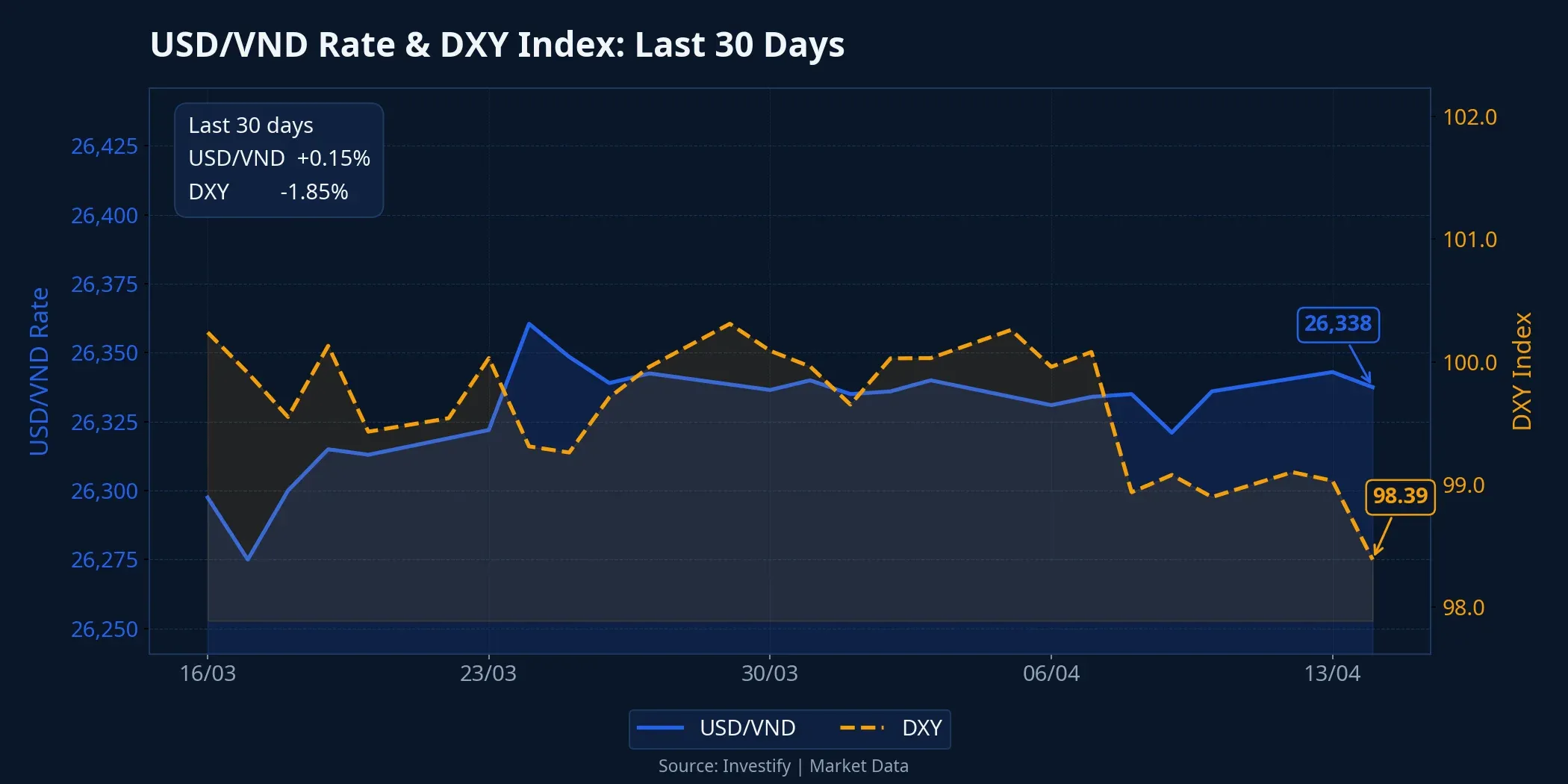

As of April 14, the interbank USD/VND rate stood at 26,337.50 VND, virtually unchanged from the start of the month (26,335 VND on April 1). The State Bank of Vietnam’s central rate hovered around 25,103-25,105 VND.

This stability could be disrupted if the Fed crisis escalates further. Three key transmission channels to monitor: (1) foreign capital outflows — if global risk-off sentiment intensifies, selling pressure would create greater volatility; (2) the USD-VND interest rate differential could narrow if the Fed is forced to cut rates early; and (3) psychological effects, as any signal of compromised Fed independence amplifies volatility across all forex markets.

The State Bank of Vietnam has multiple intervention tools: spot USD sales, cancellable forward contracts (to conserve reserves), and short-term interbank rate management. Foreign exchange reserves are estimated at over $100 billion, providing a substantial buffer.

VN-Index: Short-Term Benefit, Medium-Term Risk

On April 15, the VN-Index closed at 1,800.65 points, up 25 points (+1.41%). Vietnamese equities may benefit in the short term from a weaker USD: reduced exchange rate pressure and increased relative attractiveness of VND-denominated assets.

However, the relationship between a weaker USD and Vietnamese stock gains is not linear. If the cause of USD weakness is systemic volatility (global risk-off), foreign capital may actually accelerate outflows rather than flow in, affecting liquidity and valuations on Vietnamese exchanges.

Three Factors to Watch Over the Next 30 Days

The institutional crisis at the Fed is a real risk, not a theoretical scenario. History shows that every time central bank independence is compromised, the consequences for currency and inflation are severe. The Fed case is particularly significant given its global reach.

The primary risk remains the scenario where Warsh fails to get confirmed in time, creating a leadership vacuum at the Fed precisely when Powell’s term ends. This scenario has a meaningful probability given Tillis’s continued blocking stance.

Three factors worth monitoring over the next 30 days:

-

Warsh’s confirmation hearing (April 21): The content and market reaction will reveal the level of confidence in the incoming nominee.

-

DXY and long-term US Treasury yields: If the DXY continues falling below 97 while 10-year yields rise simultaneously (signaling a loss of confidence in the USD rather than rate-cut expectations), this would be the most serious escalation signal.

-

Foreign capital flows on HOSE: Whether the net selling trend accelerates following Fed-related events will be the most direct measure of impact on the Vietnamese market.