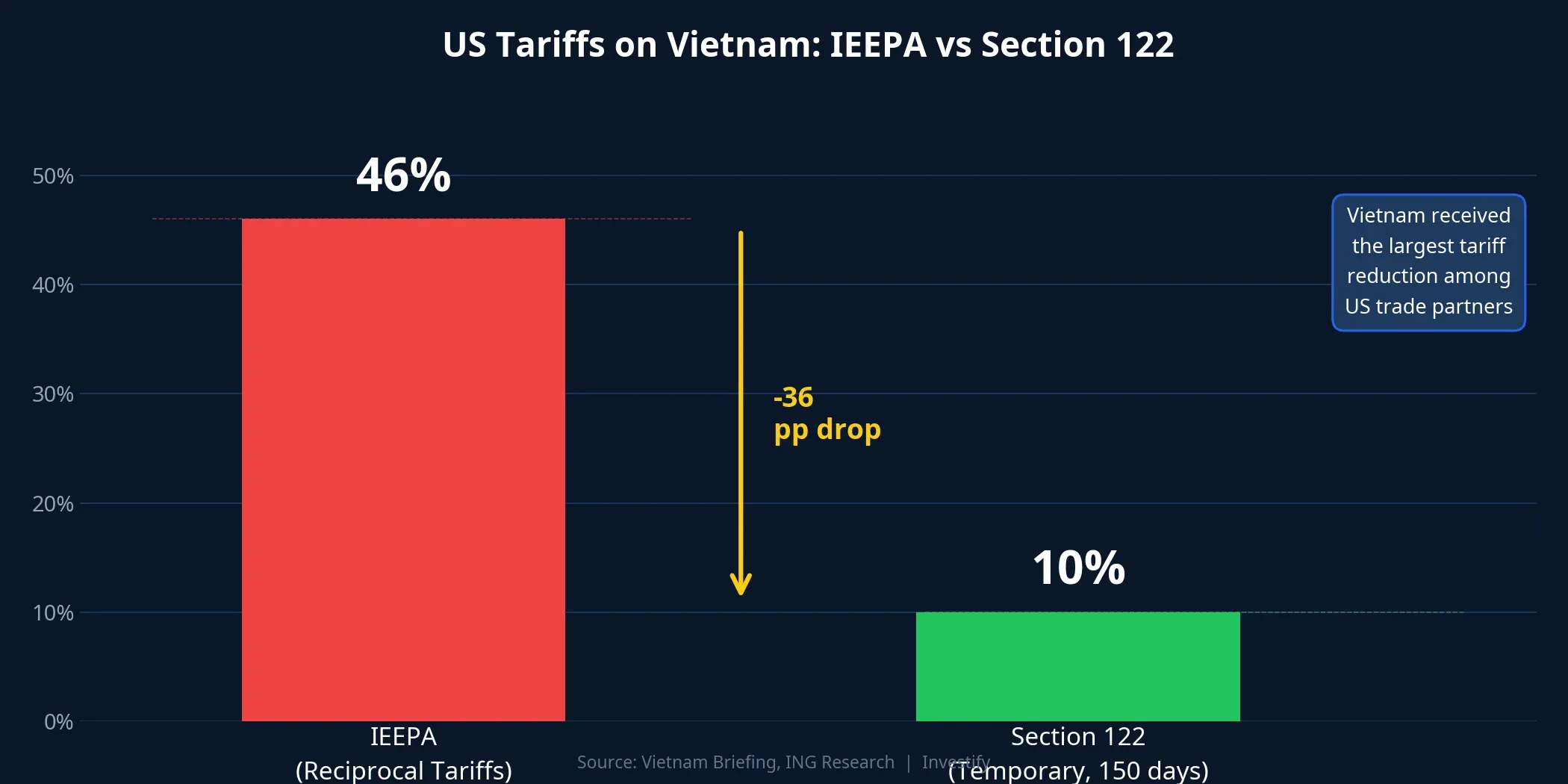

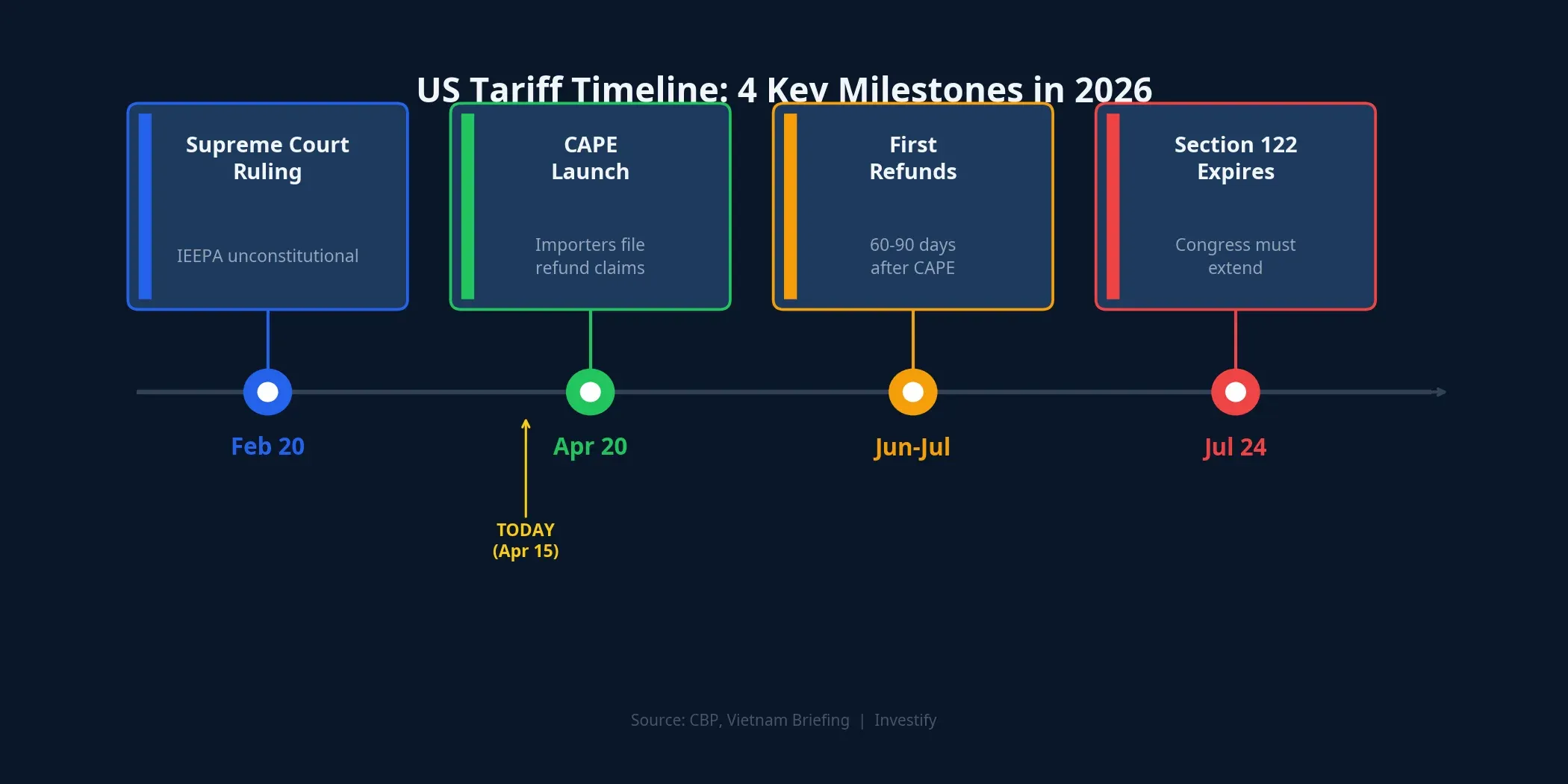

On April 20, the CAPE system officially launches in the US, opening the path to refunding approximately $166 billion in IEEPA tariffs to over 333,000 importers. For Vietnam — the country receiving the largest tariff reduction from 46% to 10% — this is a positive signal for export stocks. However, Section 122 is only valid for 150 days, and the real question lies beyond the July 24, 2026 deadline.

The IEEPA Ruling: A Legal Watershed in the US

On February 20, 2026, the US Supreme Court issued a 6–3 ruling in Learning Resources, Inc. v. Trump, affirming that President Trump exceeded his authority by using the International Emergency Economic Powers Act (IEEPA) to impose global tariffs. Chief Justice John Roberts authored the majority opinion, stating that IEEPA does not grant the President tariff-imposing powers, as this authority belongs to Congress under the Constitution.Wikipedia

This ruling invalidated most of the reciprocal tariffs imposed by the Trump administration since April 2025, including the 46% tariff on Vietnamese goods.Vietnam Briefing Immediately after, the President switched to Section 122 of the Trade Act of 1974, applying a 10% tariff to all countries. For Vietnam, this represented a 36 percentage point reduction — the largest among US trade partners.ING Research

The critical point: Section 122 has a 150-day limit and requires Congressional approval for extension. The 10% tariff will expire around July 24, 2026 if not extended, and the administration could switch to Section 301 or Section 232 with different tariff rates and calculations.

$166 Billion in Refunds: When Does the Cash Actually Flow?

US Customs and Border Protection (CBP) confirmed that the CAPE system (Consolidated Administration and Processing of Entries) launches on April 20, 2026 — just 5 days from today.The refund scope: approximately $166 billion in IEEPA duties collected across 53 million entries from over 333,000 importers.Tradlinx

Phase 1 from April 20 will process unliquidated entries and entries within 80 days of liquidation. Importers submit CAPE Declarations via the ACE Portal as CSV files, with refunds expected within 60–90 days of acceptance.Retail Dive

The bigger picture shows this is effectively a massive liquidity injection into the US goods distribution system. However, refunds will be processed in batches — not all importers receive payments simultaneously. Real cash flow back into the distribution system is expected from June–July 2026, and that is when the impact will ripple through the supply chain, including to Vietnamese suppliers.

Vietnam’s Q1/2026 Exports: Strong Growth Despite High Tariffs

Vietnam’s exports to the US in Q1/2026 reached approximately $39 billion, up 24.3% year-over-year, according to the General Statistics Office.VietnamPlus The trade surplus with the US alone reached approximately $33.9 billion. Electronics and computers led with approximately $30.7 billion (global), up 45.5% YoY.VietnamPlus Textiles reached approximately $8.8 billion but grew only 1.9% — reflecting the period still under the 46% IEEPA tariff.Doanh nghiệp Tiếp thị

The key takeaway: the Supreme Court ruling came on February 20, but the actual effect on new orders takes several more weeks to materialize. With tariffs dropping to 10% under Section 122, Q2 and Q3/2026 will be the periods that truly reflect the positive impact — especially for textiles, where the US accounts for approximately 44% of export revenue.

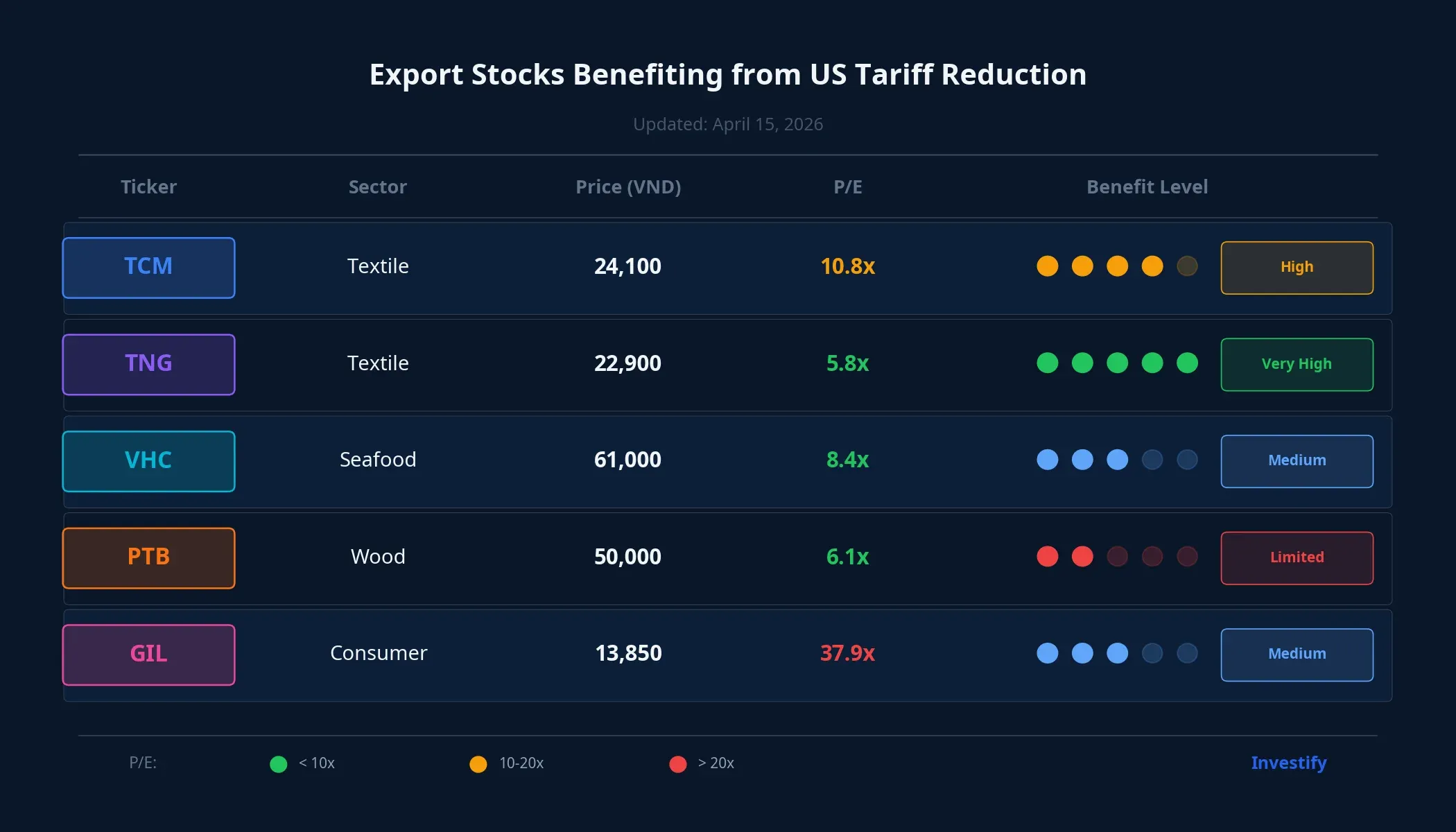

Export Stocks: Who Benefits Most?

Capital is clearly flowing into the export group. The VN-Index on April 15 reached 1,800.65 points, up 25 points (+1.41%), with textiles being the fastest to react.

TCM (Thanh Cong Textile): Priced at VND 24,100 on April 15, P/E 10.79, market cap approximately VND 2,700 billion. The US market accounts for a significant share of its order book. TCM rose from VND 22,150 to VND 24,100 over the last 7 trading sessions, equivalent to +8.8%. However, VCBS assessed that short-term outlook remains challenging due to weak demand signals and lower Q1/2026 advance orders compared to last year.Người Quan Sát

TNG (TNG Investment and Trading): Priced at VND 22,900, P/E 5.81, market cap approximately VND 2,900 billion. Client portfolio concentrated in the US–EU, with large-scale manufacturing. 2026 profit is forecast to grow 7% YoY thanks to market diversification.Dân Việt TNG dropped from a peak of VND 26,400 (March 31) to VND 22,200 (April 6) before recovering to current levels — the price range suggests the market is searching for a new equilibrium.

VHC (Vinh Hoan Corporation): Priced at VND 61,000, P/E 8.36, market cap approximately VND 13,700 billion. January 2026 revenue rose 13% YoY, but exports to the US in January fell 21% YoY according to BSC Research.Doanh Nhân Báo Pháp Luật The tariff reduction from 46% to 10% improves pangasius price competitiveness, but VHC still faces separate anti-dumping barriers — the benefit level is not as decisive as for textiles.

PTB (Phu Tai Corporation): Priced at VND 50,000, P/E 6.12. Wood and stone exports to the US account for a high share, but PTB still faces separate Section 232 tariffs on wood products at 30–50% — this tax was not affected by the IEEPA ruling.StockBiz VNDIRECT forecasts PTB’s profit may decline over 14% in 2026 due to weakness in the wood segment.

Four Key Milestones to Watch

Beyond the refund timeline, two macro risks deserve consideration. First, the DXY index declined for 7 consecutive sessions to the 98.08 level on April 15 — a 6-week low.Trading Economics A weaker USD supports US import demand but could pressure the USD/VND exchange rate. Currently, the rate remains stable around VND 26,338, with no unusual signals. Second, Section 232 tariffs (steel, aluminum, wood) remain intact — the IEEPA ruling only invalidated IEEPA-based tariffs, not the entire tariff barrier.

Conclusion: Positive Signal, but a Limited Window

The Learning Resources v. Trump ruling marks an important legal watershed, and the reduction from 46% to 10% creates clear competitive advantages for Vietnamese exports in the short term. Textiles (TCM, TNG) are reacting fastest thanks to high US exposure and tariff-sensitive margins. VHC and the wood group need more time for evaluation due to separate barriers.

However, investors should distinguish between two types of benefit: (1) short-term sentiment waves as refund news spreads, and (2) substantive improvement from new orders with lower tariff costs — this will only be reflected in Q2–Q3 business results. Section 122 is only a temporary solution, and tariff risk has not fully disappeared until the US Congress takes a clear stance.

Three factors worth monitoring over the next 3 months: (1) CAPE refund progress and the US supply chain response, (2) Q1/2026 earnings reports from TCM, TNG, VHC — the real test for the tariff reduction thesis, and (3) US Congressional action on extending Section 122 before the July 24 deadline.