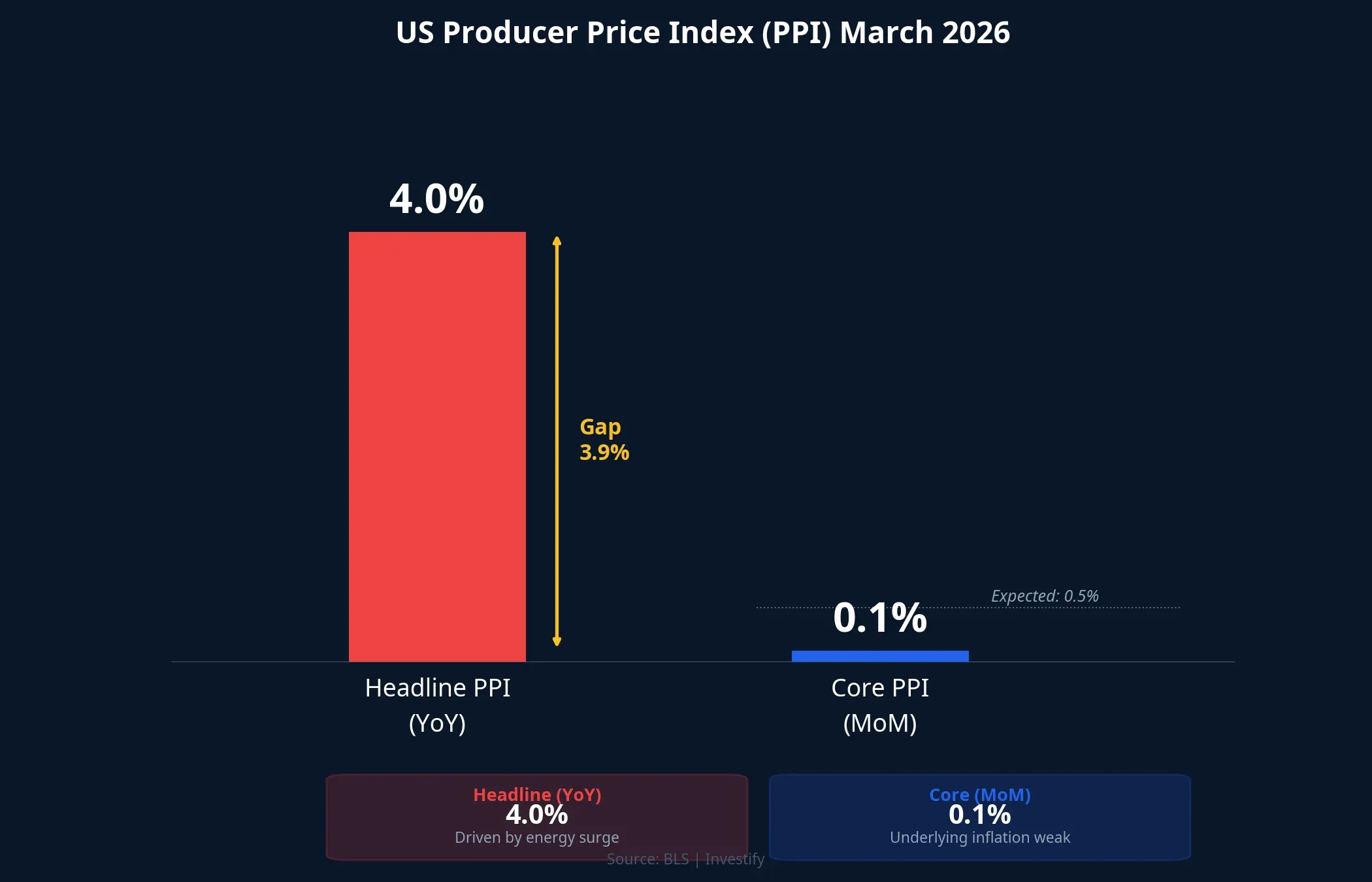

The Bureau of Labor Statistics (BLS) released the March 2026 Producer Price Index (PPI) on the evening of April 14, and the headline number was startling: headline PPI rose 4% year-over-year, the highest since February 2023.BLS But peel back the layers and the story changes entirely. Core PPI — excluding energy and food — rose just 0.1% month-over-month, five times lower than the market’s 0.5% expectation.BLS One report, two different stories. And Wall Street’s reaction reveals which story the market is listening to.

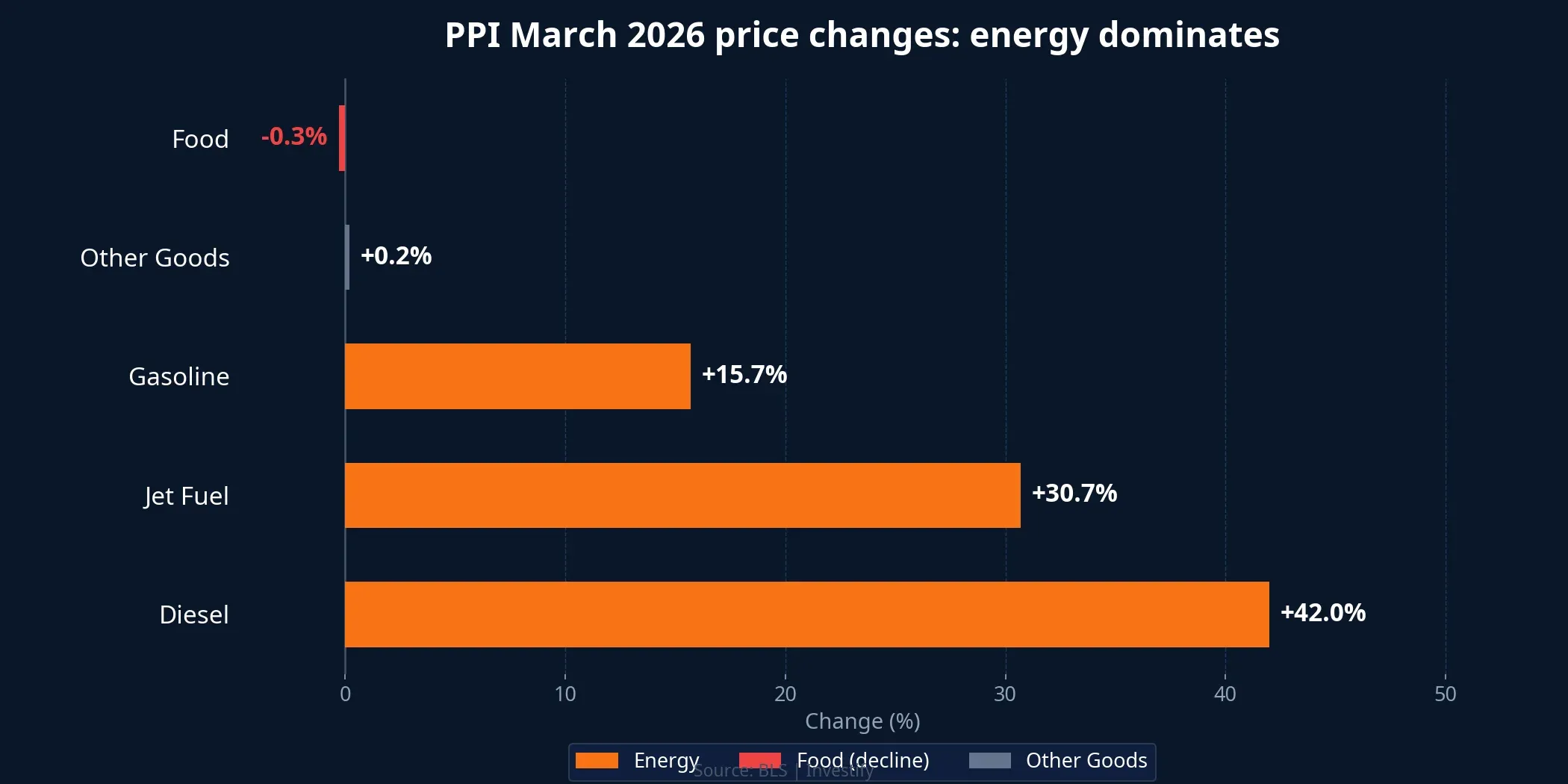

Energy dominated the entire headline increase

Even headline PPI on a monthly basis rose just 0.5%, significantly below the Dow Jones consensus estimate of 1.1%.CNBC So what pushed the annual figure to 4%? The answer lies in a single category: energy.

The energy price index within PPI surged 8.5% in March, with specific items posting dramatic gains: gasoline +15.7% (accounting for nearly half the increase in all final demand goods), diesel +42%, and jet fuel +30.7%.BLS The cause is clear: the Iran conflict that began in late February drove global oil prices sharply higher, pulling the entire fuel chain upward.

Meanwhile, other categories remained remarkably quiet. Food fell 0.3%, contributing negatively to PPI. Goods excluding food and energy rose just 0.2%. Services maintained low growth, consistent with core PPI at only +0.1% month-over-month.BLS The bigger picture shows that US producer inflation is not broadening. Price pressure is concentrated in a single commodity group driven by war-cycle volatility, not by underlying economic trends.

Wall Street read it right: core is the real signal

The US stock market’s reaction on April 14 showed investors looking through the headline figure. The S&P 500 gained 1.18%, closing at 6,967.38 points. The Nasdaq rose nearly 2%, led by tech stocks. The Dow Jones added 0.66%, or 317.74 points.247 Wall St

US Treasury yields cooled, reflecting expectations that the Fed need not react aggressively to the headline PPI number since core inflation remains under control. The market has clearly separated the two narratives: energy is an exogenous factor (a supply shock from war), not endogenous demand-pull pressure. Strip out that variable, and the actual producer inflation picture is quite benign.

Bessent: “Rates should be cut,” but understands if the Fed wants to wait

Treasury Secretary Scott Bessent made notable remarks immediately after the PPI data release. He stated: “I am very confident that core inflation — which is well under control and actually declining in many categories — will continue to come down.”CNBC

Bessent said plainly that he believes rates should be cut, but immediately added: if the Fed wants to wait for more clarity, he understands. This represents a shift in tone from earlier in the year. In January 2026, he called rate cuts “the only ingredient missing” for a stronger economy.CNBC Now he still supports cuts but acknowledges that the Iran war’s impact on energy prices gives the Fed legitimate reason to be cautious.

The Fed: holding in May, uncertain from June

According to the CME FedWatch tool, the probability of the Fed holding rates at the May meeting (May 6-7) stands at approximately 95%. The market is nearly certain the Fed will not act at its next meeting.

From June onward, the picture becomes more uncertain. Minutes from the March FOMC meeting revealed that some officials are willing to consider rate hikes if oil-driven inflation spreads to other categories.CNBC The Fed’s March dot plot projects just one 25-basis-point cut in 2026.Yahoo Finance

However, the just-released core PPI data supports the case for rate cuts. If core CPI in the coming months sends a similar signal, pressure on the Fed to act will increase, especially as the labor market shows signs of cooling.

Implications for Vietnamese investors

Foreign capital flows: cautious but not in retreat

Data from April 8-14 shows foreign investors still leaning toward net selling on the Vietnamese market, averaging approximately -684 billion VND per day. However, the April 14 session recorded net buying signals in covered warrants and derivatives — channels that typically react fastest to shifts in US rate expectations.

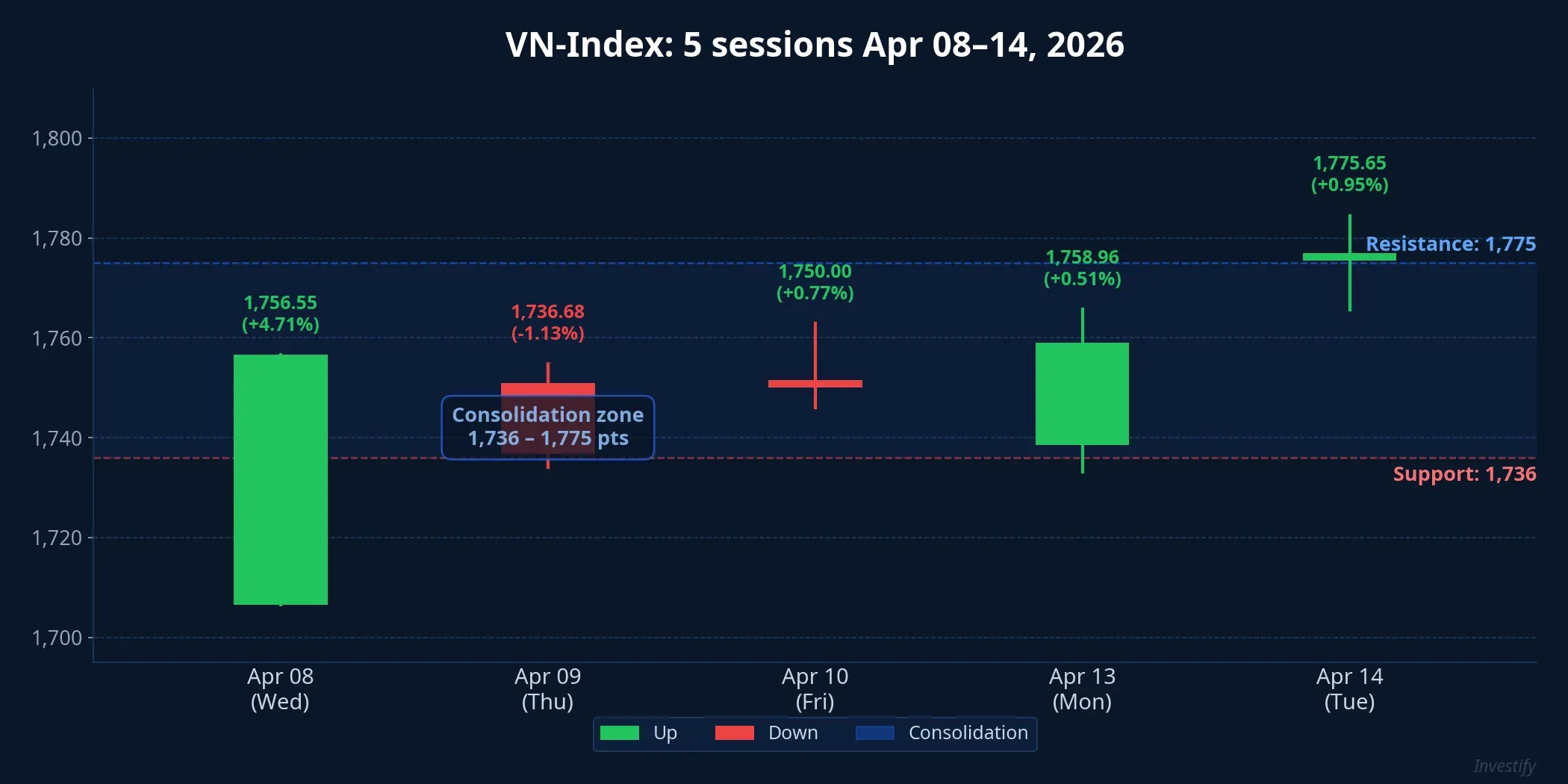

VN-Index: consolidating in the 1,736-1,775 range

The VN-Index closed the April 14 session at 1,775.65 points, up 0.95%. Over the past 5 sessions (April 8-14), the index rose from 1,736.68 to 1,775.65, equivalent to approximately 2.2%. The USD/VND exchange rate remained stable around 26,337 VND, indicating that exchange rate pressure is not yet a concern — a supportive factor for foreign capital flows.

A two-sided impact

The scenario of the Fed holding rates in May (probability approximately 95%) has two sides for Vietnam. On the positive side, US rates not rising further means the USD won’t strengthen, reducing exchange rate pressure and giving the State Bank of Vietnam room to maintain low domestic interest rates. On the limiting side, US rates not falling means the US-Vietnam rate differential remains wide, giving foreign capital no strong incentive to return.

Conclusion: weak core inflation is good news, but oil is the key variable

March PPI data sends a clear signal: US producer inflation is concentrated in energy, not spreading to the broader economy. This supports expectations for rate cuts in the second half of 2026, though the Fed will likely hold steady in May while waiting for more data.

The main risk lies in oil price developments. If the Iran conflict drags on and energy prices continue to climb, pressure could begin spreading to other categories — and at that point, the narrative changes entirely. Three factors worth monitoring over the next 2-4 weeks: Iran negotiation developments (which determine oil prices), April CPI data (confirming or refuting the declining core inflation trend), and signals from the US labor market. If energy cools and core inflation remains low, the probability of a Fed rate cut from September will increase, and that would be the moment foreign capital could meaningfully pivot toward emerging markets like Vietnam.