Vietnamese savers are facing a striking paradox. In the same week of mid-April 2026, 29 commercial banks cut deposit rates after meeting with the State Bank of Vietnam (SBV) Governor on April 9, while FiinRatings released its Vietnam Corporate Credit Conditions 2026 report warning that deposit rates could rise another 0.5-1 percentage point within this very year. The two signals are not contradictory: the current cut is a short-term administrative response to support corporate borrowing, while the upward pressure stems from the capital supply-demand structure of the whole banking system, which cannot be adjusted by a single meeting. For those holding idle cash, the question is no longer “which tenor to pick” but “which scenario should my tenor bet on over the next 12 months”.

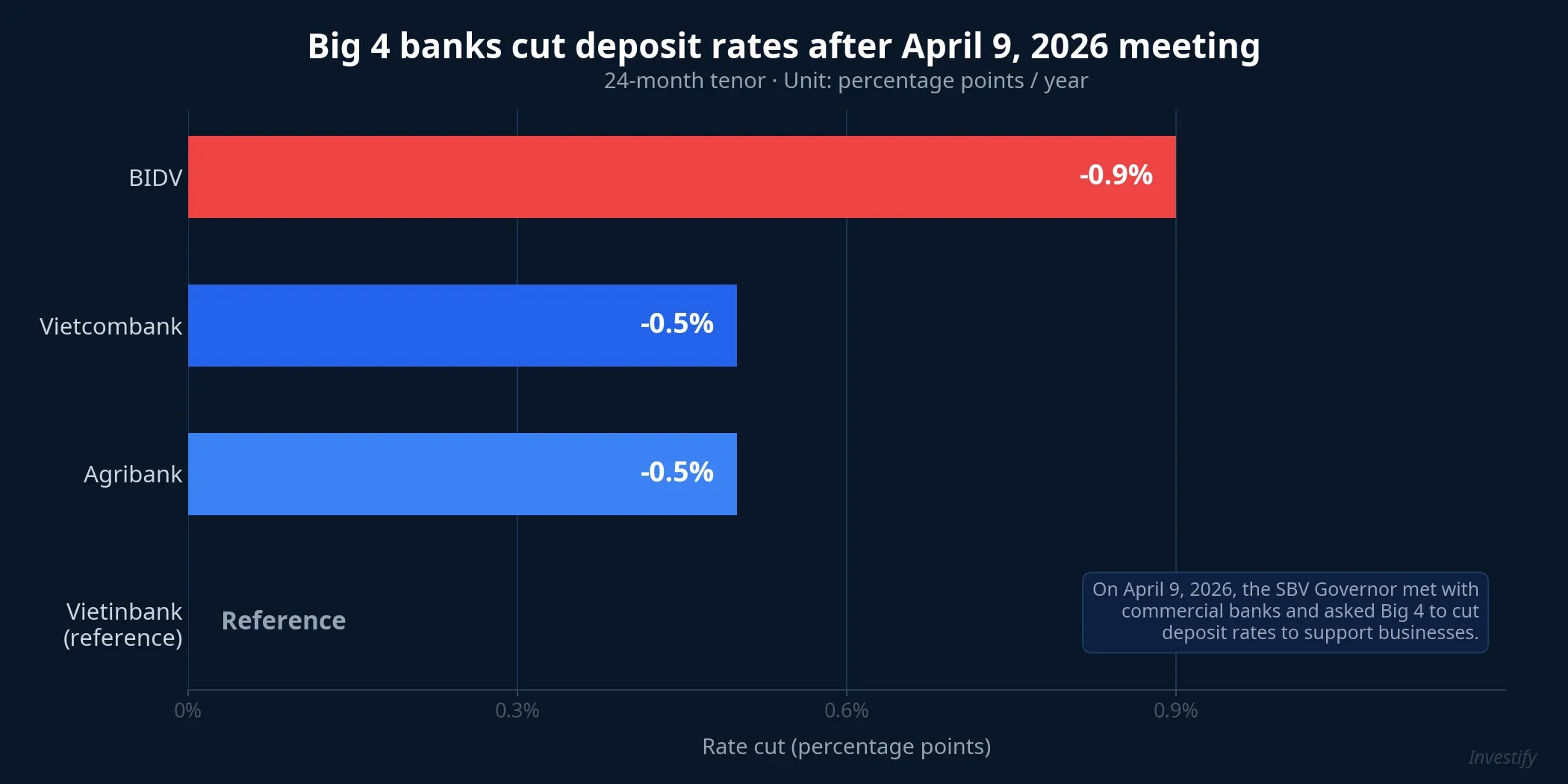

Big 4 lead the cuts, rates settle around 5.9-6.5%

The big picture shows the Big 4 state-owned banks leading this adjustment. After the April 9 meeting, Vietcombank cut 0.5 ppt at the 24-month tenor to around 6%/year, Agribank cut 0.5 ppt on tenors from 24 months up, while BIDV was the most aggressive, cutting 0.8-0.9 ppt across multiple tenors from 6 to 36 months.CafeF In total, 29 banks joined the adjustment in this round.Thoi Bao Ngan Hang

Post-adjustment, the rate grid is fairly uniform: the 12-month tenor at Big 4 banks sits around 5.9%/year, and 24-month around 6.5%/year.VietnamBiz On the interbank market, liquidity has eased temporarily. The SBV net-withdrew nearly VND 74 trillion through OMO during April 14-17, the second consecutive week,Fili bringing overnight interbank rates down to about 3.9%/year, well below the 8.58% range seen earlier this month.Bao Dau Tu

On the surface, things appear to be cooling exactly as policymakers intended. But the macro picture points the other way. March 2026 CPI came in at 4.65%, the highest in three years, leaving the real return on a 12-month deposit at just around 1.25 ppt. Q1 2026 GDP grew 7.83%, indicating that credit demand for production and investment remains strong and shows no sign of slowing into the next quarter.

Three structural signals a single meeting cannot fix

FiinRatings does not focus on short-term market prices. It looks at three structural indicators, and all three are stretched.VnEconomy

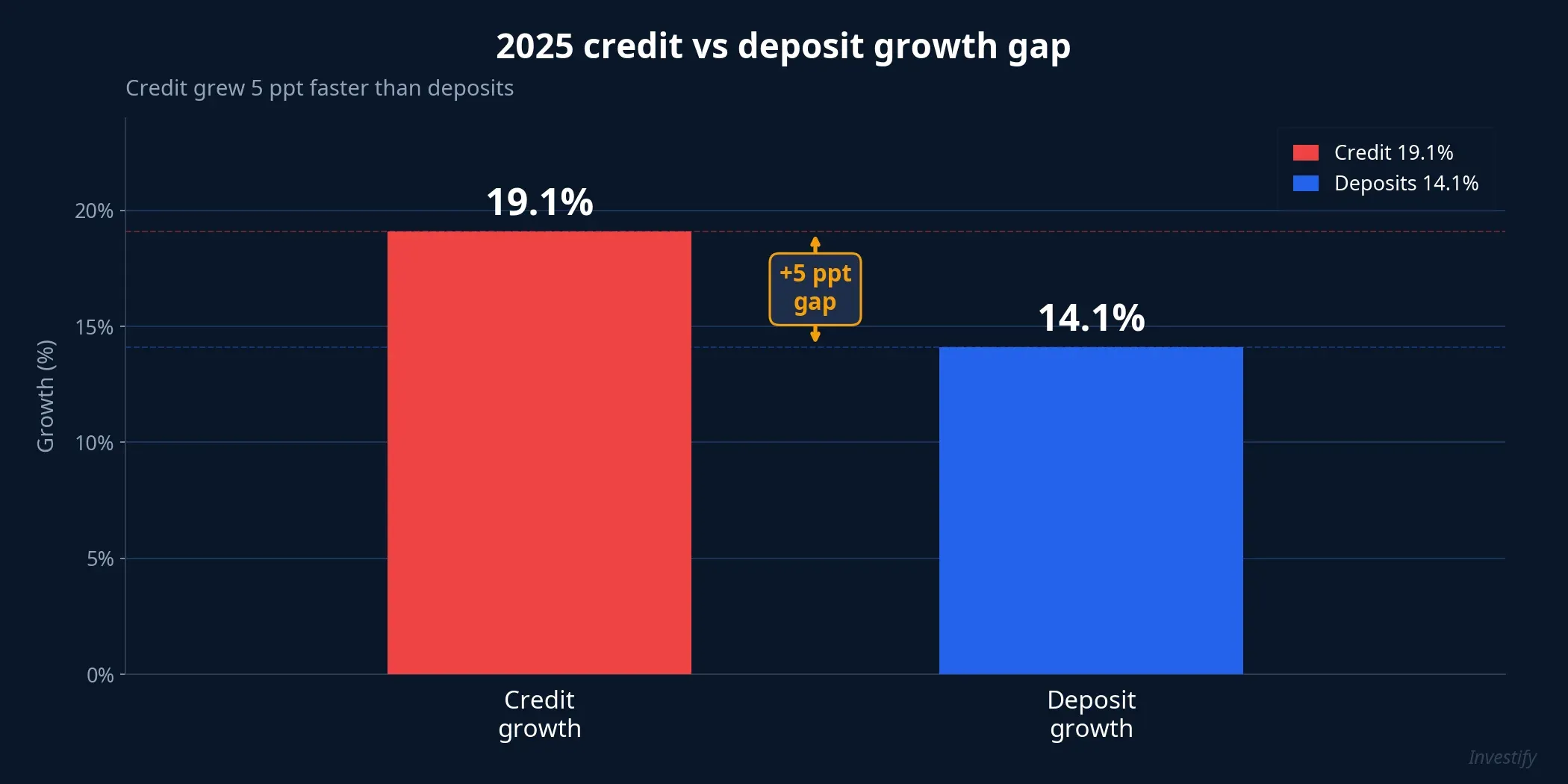

First, LDR near the ceiling. The loan-to-deposit ratio at many banks has touched the 85% regulatory ceiling. The reason is clear: 2025 credit grew 19.1% while deposits grew only 14.1%, creating a 5 ppt gap that ran across the full year.Bao Dau Tu In early 2026, excluding State Treasury deposits from the LDR calculation tightened the measure further, forcing banks to compete harder for retail funding.

Second, NIM is thin. Industry-wide net interest margin fell to about 2.9% in 2025, and FiinRatings forecasts 2026 NIM could slip further to around 3%.Thoi Bao Tai Chinh When NIM is already thin and funding costs climb, banks have only two options: raise lending rates (hard, given the mandate to support corporates) or accept a profit hit to defend market share.

Third, maturity mismatch. About 80% of deposits are short-term, while nearly 50% of loans are medium- and long-term. This maturity gap is a structural risk and does not disappear merely because of a VND 74 trillion OMO net-withdrawal.

Capital flows follow this structural logic. When banks lack long-term funding, they compete on deposit rates, and the current administrative cut only delays rather than removes that pressure.

Three rate scenarios for the next 12 months

Based on the structural signals above, three scenarios are worth weighing for savers.

Scenario 1: Rates stay low and stable (moderate probability)

This plays out if 2026 credit growth slows below 16%, USD/VND holds below 26,000, and CPI eases back toward 4%. The SBV would continue modest net-withdrawals to keep interbank rates around 4-5%. Deposit rates would sit flat within 5.5-6.0% at Big 4 for the 12-month tenor, and 6-7% at top private banks. Savers don’t gain a higher yield, but also don’t need to rush into long tenors to lock in rates.

Scenario 2: Rates rise per FiinRatings forecast (highest probability under current structural setup)

Triggered by credit continuing to outpace deposits, USD/VND breaking above 26,500, and the Fed keeping rates high for longer. LDR pressure forces banks to raise deposit rates 0.5-1 ppt during H2 2026, pushing Big 4 12-month rates into the 6.4-6.9% range and top private banks to 7.5-8%. This is the path the three structural indicators (LDR, NIM, credit/deposit gap) currently point to, though “highest probability” does not mean certain.

Scenario 3: SBV pivots back to easing (lower probability)

This requires Q2 GDP below 7%, CPI falling fast toward 3%, and the SBV loosening credit to support growth. Short-term rates would drop further, with Big 4 12-month rates potentially reaching 5-5.5%. With CPI around 3%, real returns stay positive but only at 1.5-2 ppt. This is the worst-case scenario for savers because both nominal and real yields compress.

What idle cash can consider

Given that scenario 2 has the strongest structural backing, some portion of capital should not rush into 24-36 month tenors at current low rates. A 3-6 month tenor preserves flexibility, allowing savers to catch a rate uptick if LDR pressure forces banks to lift deposit rates in H2 2026. The portion of capital that requires absolute safety should still sit at Big 4 banks within the VND 125 million deposit insurance limit per person per bank.

For capital that does not need immediate liquidity, fixed income products on fintech platforms can serve as a complementary layer worth considering. With Big 4 12-month rates around 5.9% and real returns only 1.25 ppt above CPI, some fixed income products currently offer notably higher yields. A key caveat: fixed income is not insured like deposits. The trade-off between higher yield and issuer credit risk must be evaluated carefully before allocation.

Rather than guessing the rate peak, three indicators are worth tracking weekly: OMO net-withdrawal/injection volume, overnight interbank rates, and the USD/VND central rate. When all three move in the same direction for 2-3 consecutive weeks, that’s a signal the scenario is being confirmed. Q2 earnings season will release the next LDR and NIM figures. This will be the first test of whether FiinRatings is right or whether the SBV can contain the structural liquidity pressure.