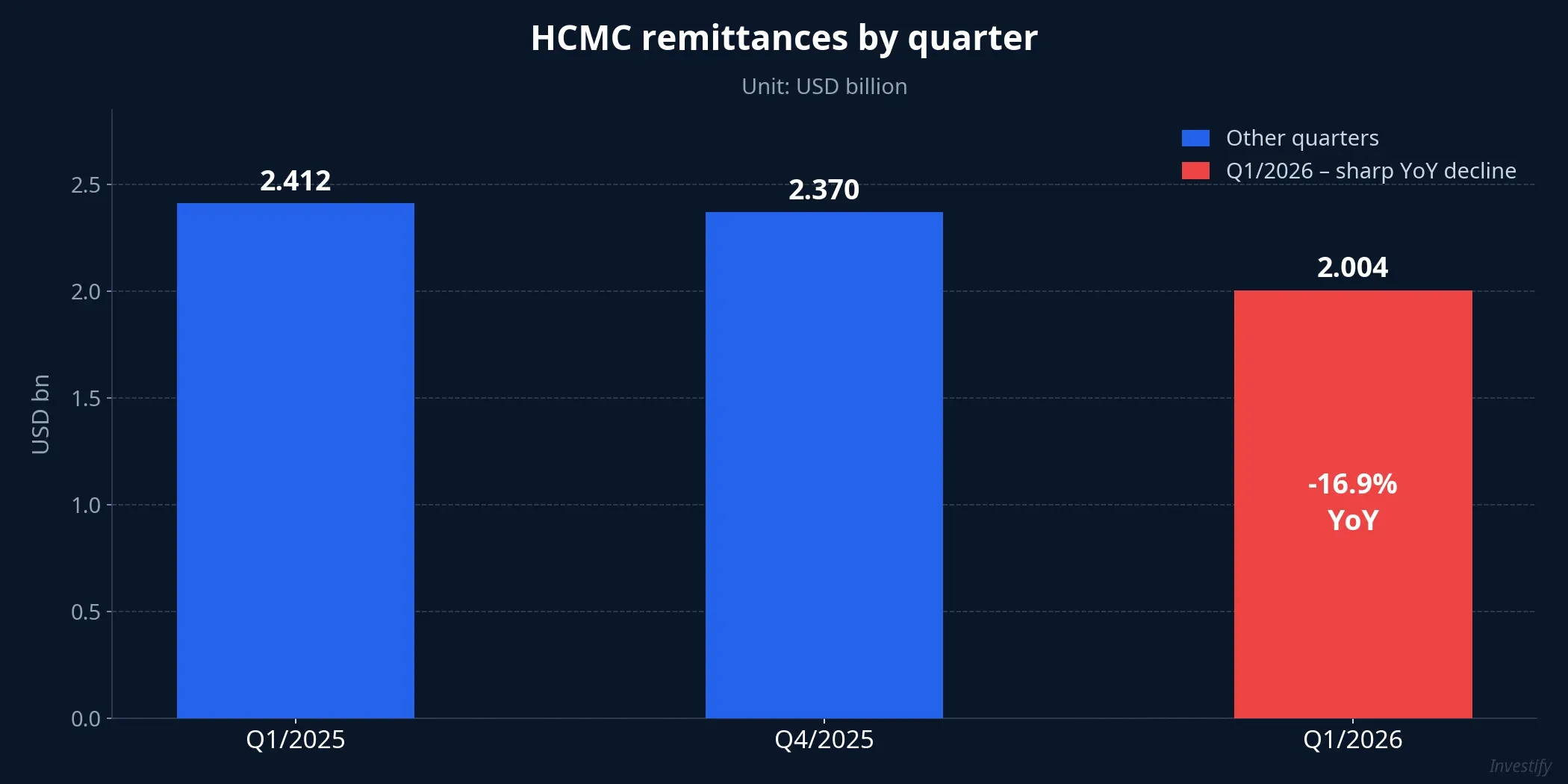

On 18 April 2026, the State Bank of Vietnam’s Ho Chi Minh City branch published a figure that FX analysts will want to sit with: remittances into the city in Q1/2026 reached USD 2.004 billion, down 16.9% YoY and 15.6% QoQ.Tien Phong After years of steady growth — full-year 2025 hit USD 10.34 billion, up 8.3% from 2024DNHN — this is the first quarter to register a double-digit drop.

The bigger picture shows this is not a one-off shock but the compound effect of three pressures acting simultaneously on how overseas Vietnamese send money home. And three domestic financial channels will feel it most clearly: mid-to-high-end real estate, domestic USD supply/demand, and household savings.

How important are HCMC remittances in Vietnam’s USD picture

To weigh this USD 2 billion figure, place it in the context of Vietnam’s USD supply. In 2024, total nationwide remittances were an estimated USD 16 billion, of which HCMC alone contributed USD 9.6 billion, roughly 60%.HCMC Gov Portal In 2025, the HCMC figure rose to more than USD 10.3 billionTinnhanh CK, holding the 55–60% share of the national total.

Benchmarking against other USD sources helps calibrate the signal. FDI disbursements in 2025 were around USD 25–26 billion; the goods trade surplus ranged USD 20–25 billion per year. HCMC remittances alone are nearly half of FDI disbursements, or the entire trade surplus of several years. This is soft USD supply in the truest sense: no payment obligation attached, no rollover risk, no sensitivity to foreign-investor sentiment on the stock exchange. It has been one of the most important cushions for the VND exchange rate over the past decade.

On source composition, per SBV HCMC’s late-2025 disclosure, Asia accounted for nearly 50%, led by Japan, Korea, and Taiwan — home to large communities of Vietnamese labor exporters. The Americas ranked second, mostly from the US and Canada, at around 30%. The remainder comes from Europe, Oceania, and Africa. This composition is the key to why Q1/2026 fell so sharply.

Three layers behind the Q1/2026 drop

Layer 1 — seasonality and a high base. Q1 is always lower than the preceding Q4 because overseas Vietnamese concentrate remittances around Tet. But a 16.9% YoY drop cannot be explained by seasonality — Q1/2025 was also Tet-affected and still posted USD 2.412 billionVnEconomy. The high base is part of the story, but not enough to close the gap.

Layer 2 — host-country economic conditions. Per SBV HCMC, slow global recovery, prolonged Middle East conflict, and sticky inflation in several labor markets have pressured disposable income of Vietnamese workers abroad.Tien Phong The effect is sharper in Middle Eastern host countries, but their share of HCMC remittances is small, making it a secondary driver. The bigger story is Japan and Korea — the two main Asian sources — where real wage growth has slowed as inflation lingers. When JPY and KRW purchasing power lags, the surplus available to remit to Vietnam shrinks.

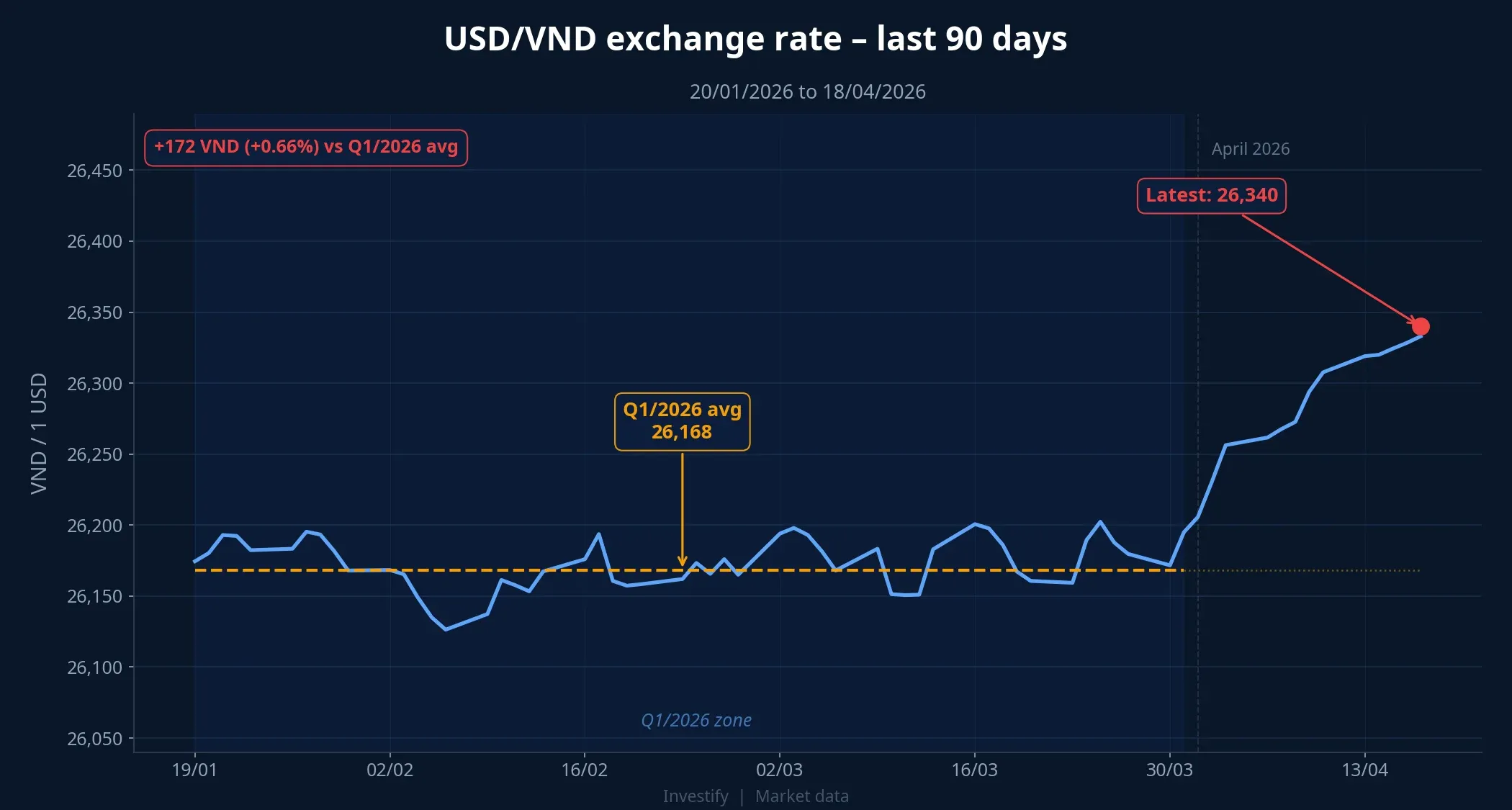

Layer 3 — exchange rate levels and remittance channels. USD/VND in Q1/2026 averaged around 26,168 VND/USD, roughly 3% higher than the same period 2025. The most recent quote stood at 26,340 VND/USD on 17 April 2026.SBV DXY stayed above 98 all quarter, briefly touching 100 in mid-March. When USD is strong in host countries, overseas Vietnamese tend to hold USD for local spending or investment rather than remitting. In parallel, as the spread between the official rate and the free market narrowed (free market now only ~0.3–0.5% higher), informal remittance channels lost their edge — though this does not automatically mean those flows reroute to official channels absent a domestic spending need.

These three layers are not mutually exclusive; they compound. Seasonality explains part of the YoY gap; weaker Japan–Korea conditions explain why the Asian source softened; a strong USD dampens the incentive to remit from both Japan–Korea and US–Canada.

Three channels that will feel it most

Mid-to-high-end real estate in HCMC. Remittances have long been a meaningful funding source for mid-to-high-end apartments and peri-urban land, particularly central-coast beach projects funded indirectly by HCMC-based investors. A one-quarter shortfall of roughly USD 400 million is not enough to collapse the segment. But combined with net foreign selling of VND 5,751 billion on VHM during 13–17 April and tightening real-estate credit, liquidity pressure in the mid-to-high-end tier will become more visible in Q2.

Domestic USD supply and demand. The remittance drop coincides with rising energy imports tied to elevated Middle East oil prices, and FDI registrations showing signs of slowing at large projects. The USD balance is therefore less favorable than in 2025. This is partly why SBV sold USD forward in March to keep the market stable. Near-term, exchange-rate risk tilts upward unless other USD sources — especially FDI disbursements and the trade surplus — improve.

VND savings and household consumption. For households whose income depends on remittances, weaker foreign inflows translate directly into lower VND deposit flows. With 12-month Big4 savings rates at just 5–5.5% and March CPI at 4.65%, real yields are marginally positive. Some overseas Vietnamese therefore choose to hold USD in cash or buy gold — SJC sell price has reached around VND 172 million per tael — rather than convert to VND deposits. Money is rotating out of traditional deposit channels, and remittances are just one link in the chain.

The 2026 picture and signals to watch

A single quarter is not enough to conclude that remittances have entered a structural reset. But the macro backdrop is not supportive: UOB cut Vietnam’s 2026 GDP growth forecast from 7.5% to 7.0%, with Q2, Q3, and Q4 growth projected at 6.5%, 6.8%, and 7.0% respectively.VnExpress If the Middle East conflict does not cool and Japan–Korea real wages remain weak, Q2 remittances will likely undercut the same period in 2025.

The reverse scenario is not excluded. When the Fed resumes cutting rates in 2H/2026 — the scenario markets are pricing — DXY should ease, USD weaken, and remittance behavior may reverse: holding USD abroad becomes less attractive, and converting to VND for gold, stocks, or real estate becomes more rational.

Three signals worth watching in the months ahead: (i) Q2/2026 HCMC remittance data, due in July — a second double-digit decline would confirm a restructuring trend; (ii) DXY and USD/VND after the Fed’s May and June meetings; (iii) real wage growth in Japan and Korea, the two sources that together account for nearly half of Asian remittances into HCMC.

Remittances are not a “drama” indicator. They are a stable, low-volatility inflow — and precisely because of that, the first double-digit decline in years deserves attention from retail investors. Not for panic, but for the understanding that one of the softest USD cushions in Vietnam’s economy is thinning, at the same time other cushions (FDI, trade surplus) have yet to show stronger signals.