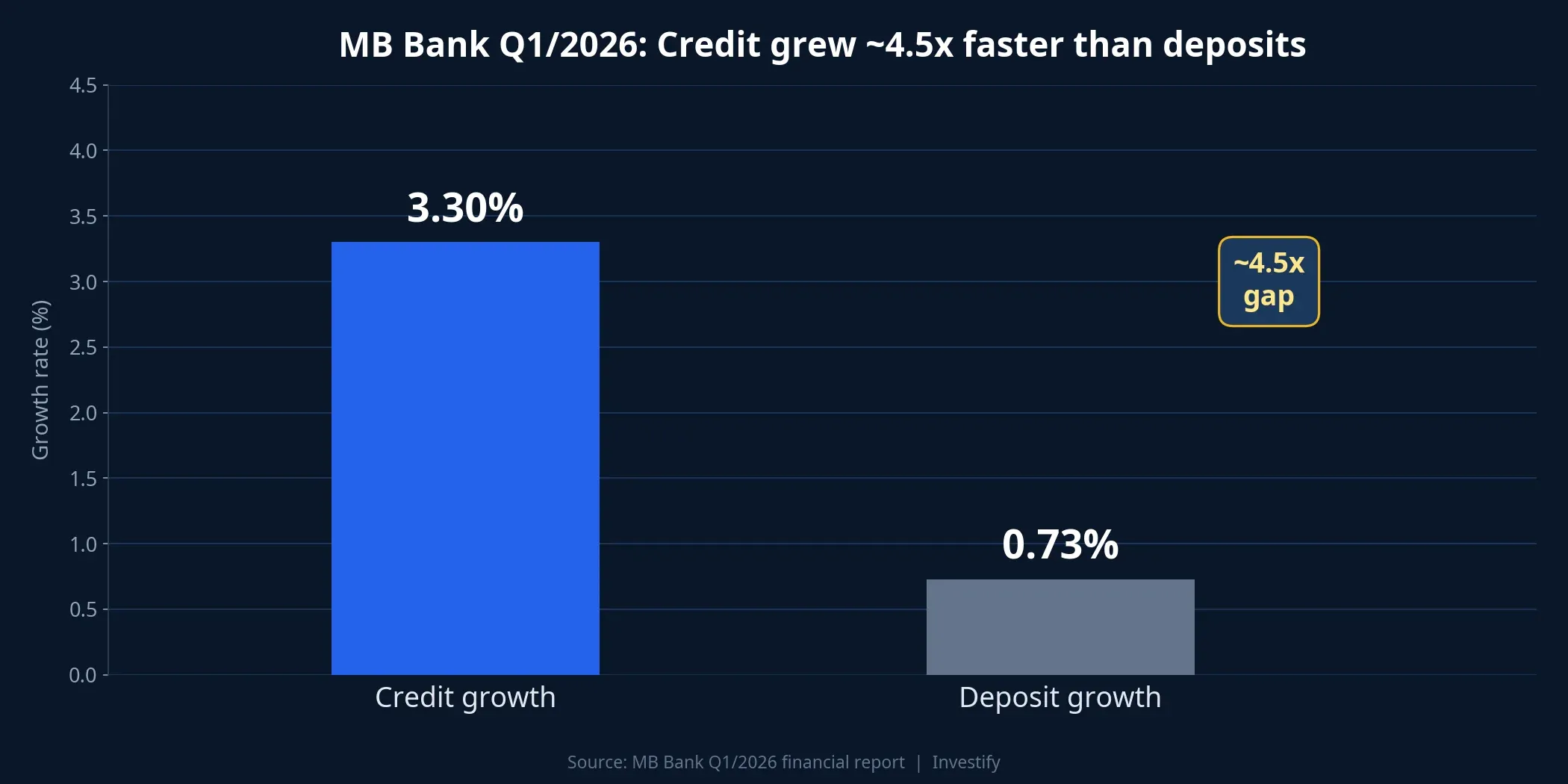

On the morning of 18 April 2026, at MB’s annual general meeting, CEO Phạm Như Ánh made a statement rarely spoken publicly by the head of a top-tier Vietnamese bank: “The market is fundamentally short of cash.” The numbers behind the line were even more striking — in Q1/2026, MB’s credit grew 3.3% while deposits grew just 0.73%.Vietstock

The big picture immediately reveals a paradox: if the system is that short of cash, why did 29 banks just simultaneously cut their savings rates last week? The answer lies not in a short-term episode but in three structural mechanisms simultaneously squeezing net interest margin (NIM) across the sector ahead of Q1 earnings. Reading these three mechanisms correctly is the precondition for telling apart banks that have a buffer from banks that are about to come under pressure.

Mechanism 1: The credit-deposit gap isn’t MB’s alone

The 3.3% vs 0.73% gap at MB might look like a one-off. In reality, it is a typical slice of the whole system in 2025 — and this is the first point to see clearly.

The capital flow is shifting in a way the State Bank already documented in December: from the start of 2025 through 24 December, system-wide credit grew 17.87% while deposits grew only 14.11%.Chinhphu That ~4 percentage-point gap represents close to VND 2 quadrillion that the system had to plug from sources other than household deposits. The sector’s loan-to-deposit ratio reached 111% by end-Q3/2025 — the highest in years.CafeF

For MB specifically, the regulatory LDR was 79% at end-2025, but the bank supplements funding through several channels: ~VND 150 trillion in equity, nearly USD 3 billion borrowed from international institutions, and the interbank market. These alternative layers of funding, replacing household deposits, are why MB has been able to grow credit at nearly 5x the deposit pace in three months without breaching safety limits. Put differently, the 3.3% vs 0.73% gap is not a sign that “MB is weak at funding” — it is an early signal of a condition affecting the whole sector.

Mechanism 2: Real rates near zero are pushing money out of banks

Why is deposit growth so slow? This is the second link, and it explains why the rate cuts last week do not contradict the “short of cash” condition.

March 2026 CPI came in at 4.65% — the highest in three years. At the same time, 29 banks cut deposit rates, bringing the 12-month tenor at many major banks to around 5–5.5% p.a. When nominal savings rates barely exceed inflation by one percentage point, the real rate is close to zero on longer tenors and negative on some short tenors. The last time real rates sat at this level was during the 2020–2021 easing cycle, when idle money left banks faster than policymakers had anticipated.

The structural consequence matters more than the specific numbers in any single channel. The VN-Index closed the week at 1,817.17, reflecting a flow of capital toward yield profiles higher than savings deposits. Similarly, gold and affordable real estate have seen demand return. These observations are not short-term speculation signals but the familiar logic of near-zero real rates: money seeks spread.

This is the classic NIM-compression loop: lower deposit rates push money out of banks, slower deposit growth widens the credit-deposit gap, and banks lean more on high-cost funding to keep lending. The logical next question: why don’t banks raise deposit rates again to attract funding back? That is the third mechanism.

Mechanism 3: The lending-rate commitment is capping NIM room

This is the part that gets less airtime in the media, yet it is the factor that will shape bank profits this year.

The State Bank’s 2026 credit-growth guidance is set around 15%, lower than 2025’s 19%, with a mandate to prioritise production credit and keep lowering the cost of capital for the economy.Tuổi Trẻ The 29-bank deposit-rate cut last week is, in effect, the groundwork for the next round of lending-rate cuts. In other words, the system cannot push deposit rates up to quench its funding need, because the output side has been committed to stay low.

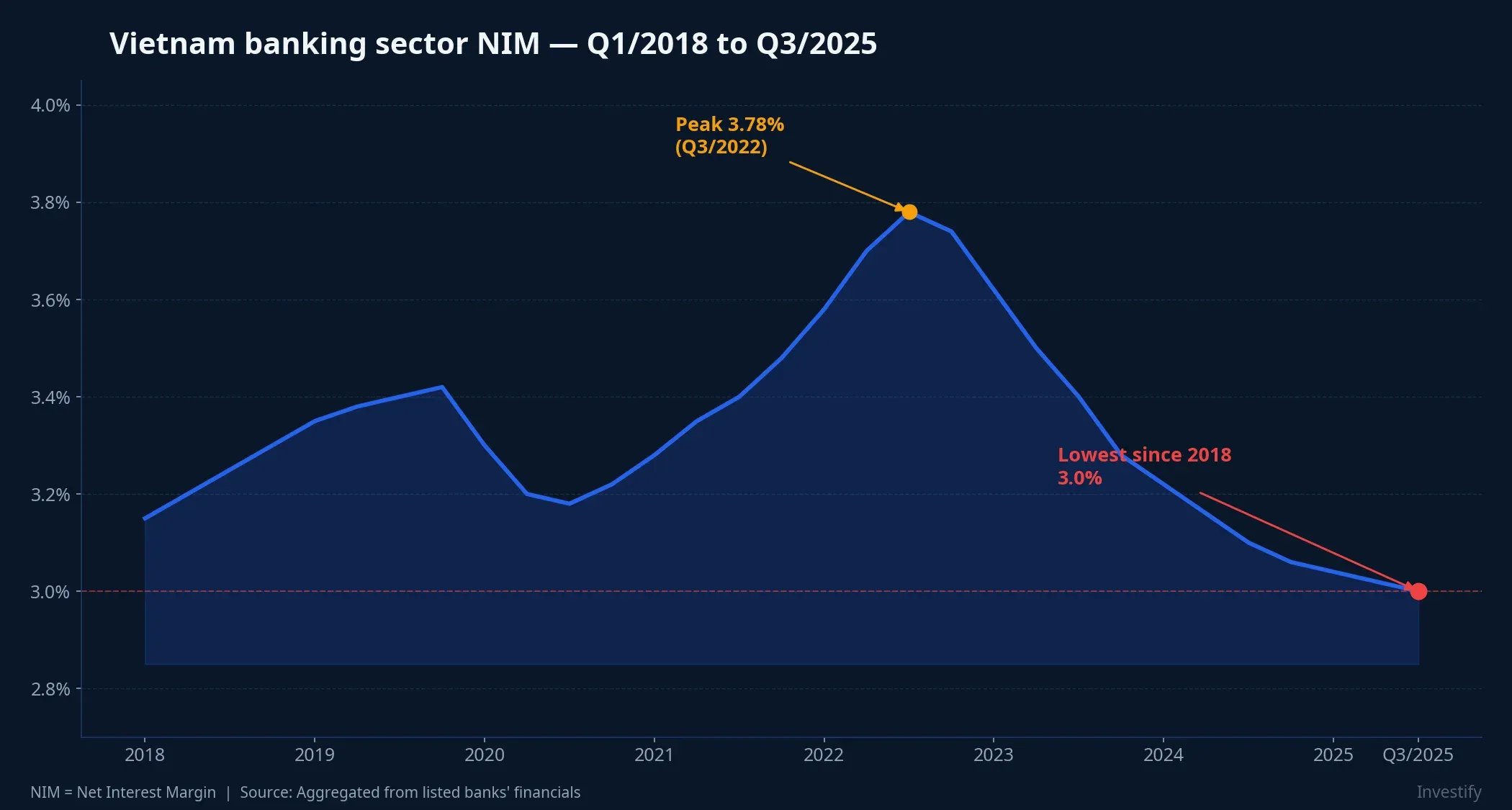

The result: sector NIM has declined for 10 straight quarters. NIM fell from 3.25% in Q1/2025 to 3.0% in Q3/2025, with the trailing four-quarter average at 3.15% — the lowest since 2018.CafeF

The crucial point is this: what will shape 2026 bank profits is not the pace of credit growth, but the ability to control funding cost. Banks with high CASA ratios (Vietcombank, MB, Techcombank) hold a better buffer because they rely less on high-priced term deposits. Banks that lean heavily on long-tenor, high-cost term deposits will face more visible NIM pressure over the next two to three quarters. It is worth emphasising, however, that NIM is only one variable — asset quality, non-interest income growth, and NPL control also materially affect the bottom line.

Q1 implications: read bank earnings through three lenses

MB’s 2026 plan is a textbook case to test the three mechanisms in practice. The bank targets pre-tax profit of VND 39.4 trillion (+15%), total assets heading toward VND 2 quadrillion (+28%), with credit and deposits both rising 30%.TNCK Charter capital is set to rise from VND 80.55 trillion to a maximum of VND 102.687 trillion, adding another layer of buffer to absorb liquidity pressure.24hMoney Q1 has already delivered VND 9.5 trillion (+13%), equivalent to 24% of the full-year plan.

Three lenses to apply when dissecting any listed bank’s Q1 report:

- Credit vs deposit growth gap: banks that narrow the gap will have a more stable NIM base in H2.

- CASA share: the most important lever for withstanding funding cost when lending rates are kept low.

- Newly formed NPLs: when credit accelerates while deposits lag, the quality of new loans is the hidden variable to scrutinise.

Conclusion: read the three mechanisms before earnings season

MB CEO’s phrase “the market is fundamentally short of cash” is not a disaster warning — it is a blunt description of a macro condition that has already existed. The three mechanisms that come with it — a system-wide credit-deposit gap, real rates near zero, and NIM room held down by lending-rate commitments — are likely to keep shaping bank profits over the next two to three quarters.

The core thesis stands: 2026 will be the year when differences among banks show up in funding-cost control, not in credit-growth speed. Two specific risk triggers could flip this thesis: (1) the State Bank raising the credit-growth cap or lifting policy rates, which would reopen room on deposit rates; (2) CPI cooling materially below 3.5% in Q2, restoring clearly positive real rates and keeping deposits inside the system.

The upcoming Q1 financial reports are the first test. The three lenses — gap, CASA, and newly formed NPLs — form the frame for reading those reports without being swept up in headline profit growth.