A company with a market cap of roughly VND 20,700 billion is operating with only 2 of 5 board seats filled. That is not a common situation among HoSE blue chips, and it is precisely why the extraordinary general meeting (EGM) on May 8, 2026 is the most important governance event of the year for Duc Giang Chemical Group (ticker: DGC) shareholders.

The real risk is not the recent price drop. It is the path to rebuilding the board, resolving the delayed 2025 audited financial statements, and whether management can preserve the strategic ambition in battery materials. All three are observable directly from the EGM resolutions, without waiting for the final investigation outcome.

From 5 board members to 2: who is steering DGC now

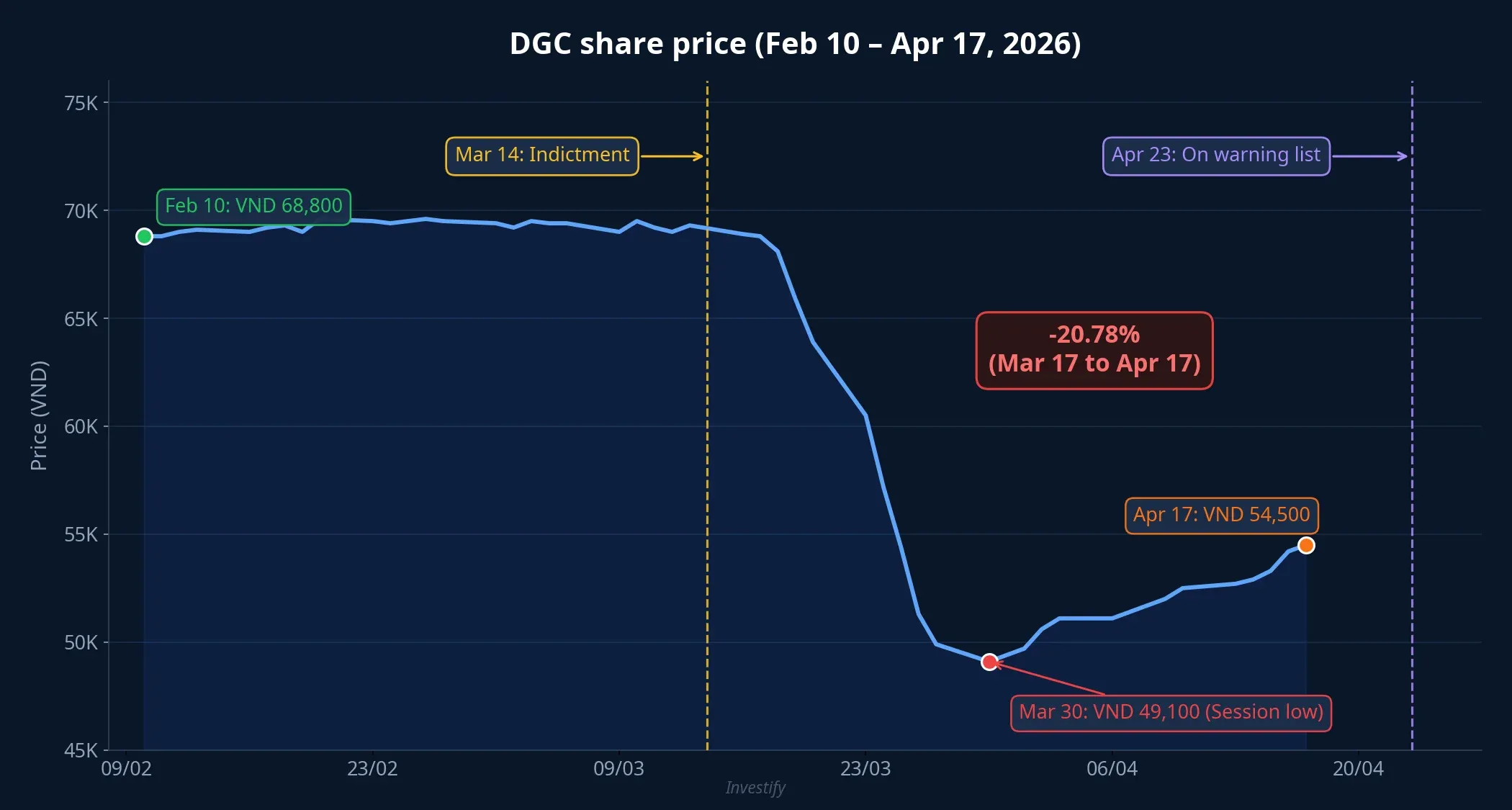

After the Ministry of Public Security’s Investigation Police Agency opened a criminal case on March 14, 2026, three of the five board members for the 2024–2029 term were indicted.Nhadautu They are Chairman Dao Huu Huyen, Vice Chairman Dao Huu Duy Anh (the chairman’s son), and board member Pham Van Hung. In total, approximately 14 individuals across the DGC ecosystem have been indicted, from chairman and vice chairman down to branch directors and chief accountants.Cafef

The two remaining members are CEO Luu Bach Dat — appointed in March 2025 specifically to replace Mr. Dao Huu Duy Anh — and Nguyen Thi Thu Ha, the only independent board member not named in the indictment. The 2/5 figure matters not because it violates the law (HoSE still allows a minimum of three members for public companies) but because it forces the company to accelerate board restructuring in order to legitimize strategic decisions.

Why does a short-handed board matter? Because major investment decisions — phased expansion of FePO4, the PCl3 plant, or additional capital raising — cannot be approved unless the board is fully constituted and sufficiently independent. The May 8 EGM is the nearest legal window to restore that structure.

Two layers of market sanction now sit on DGC

What the reports do not say plainly: on top of the legal crisis, DGC has absorbed two separate layers of sanction from HoSE, and they compound on trading sentiment.

Layer one — margin ineligibility from April 9, 2026, due to delayed publication of the 2025 audited financial statements by more than 5 working days. Investors using margin have been forced to reduce leverage or face forced selling.

Layer two — placement on the warning list from April 23, 2026, due to delay of more than 15 days against the regulatory deadline.Dantri DGC argues this is force majeure: many accounting documents and records are currently sealed and held by the investigation authority, so the company cannot cooperate with auditors to complete the report on time.VnEconomy

The two layers compound clearly onto the price. From March 17 (close: VND 68,800) to April 17 (close: VND 54,500), DGC fell 20.78%. Peak drawdown from March 17 to the March 30 bottom reached 28.63%, with consecutive floor sessions of -6.9% on March 17–18 and 19–20 immediately after the indictment news. The subsequent rebound has not restored pre-crisis levels.

Point worth noting for current DGC holders: once a stock enters the warning list, margin ineligibility continues. The path out depends on the company completing the 2025 audit with an unqualified opinion — which in turn depends on how fast the investigation authority returns the accounting documents. This is a dependency chain that individual shareholders cannot control.

EGM on May 8: three decisions that reframe the company

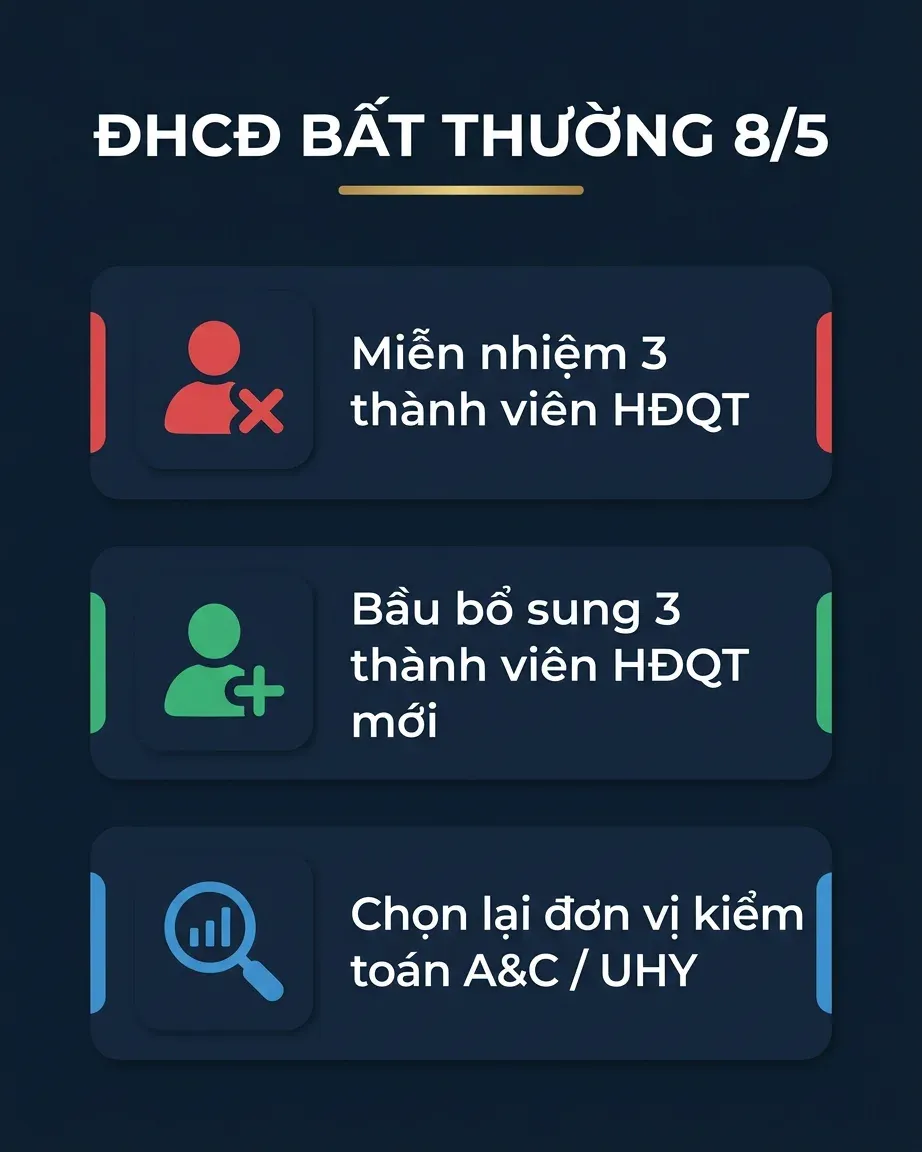

According to the resolutions published on the HoSE system, the May 8, 2026 EGM will decide three main items:Cafef Vietstock

- Dismiss 3 board members — Mr. Dao Huu Huyen, Mr. Dao Huu Duy Anh, and Mr. Pham Van Hung.

- Elect 3 new board members. As of April 18, the specific list of candidates has not been officially published.

- Select a new audit firm for 2025 financial statements, the 2026 semi-annual review, and the 2026 audit. Two proposed candidates are A&C Auditing and Consulting and UHY Auditing and Consulting.

The new board candidate list, if not released before the EGM, will be the most price-sensitive piece of information in the following week. Shareholders should read the official resolutions as soon as they are released, rather than relying on rumors.

Scope of charges: three categories, damage value not yet disclosed

To gauge how long the legal risk could last, it helps to understand the scope of the charges. The case has been opened under three categories of offense:Cafef

- Environmental pollution — related to illegal dumping of millions of tons of waste at Tang Loong Industrial Zone.

- Violation of regulations on research, exploration, and extraction of natural resources — illegal extraction of hundreds of thousands of tons of apatite ore, worth hundreds of billions of dong.

- Violation of accounting regulations causing serious consequences — off-book records, revenue concealment, causing tax damage in the tens of billions of dong.

Mr. Dao Huu Huyen is charged with all three offenses; Mr. Pham Van Hung with two (accounting and environmental); Mr. Dao Huu Duy Anh with one (accounting). The investigation conclusion and formal indictment have not been published as of April 18, 2026, so the final damage figure and penalties remain unknown. The gap from indictment to formal charges in large economic cases typically runs several months — during which the stock continues to trade at a legal-risk discount.

Battery materials ambition: strategy intact, execution team replaced

The question many long-term investors are asking: does the strategy of moving into battery materials — the “second gold mine” after phosphorus — remain intact now that all three senior leaders have been indicted at once?

According to analyst reports on DGC, the 2026 strategy focuses on battery input materials, not finished battery cells. FePO4 (iron phosphate) from DGC has been accepted by Japanese, Korean, and Taiwanese customers; the company is also developing LFP and PCl3 (used to produce the LiPF6 electrolyte salt). The Nghi Son project (caustic soda — chlorine) is expected to reach commercial operation in Q2/2026, supplying chlorine for in-house PCl3 production.

This ambition sits in the annual report published before the indictment. Technical operations at the chemical plants do not directly depend on the three indicted board members; CEO Luu Bach Dat and the management team continue to run production. However, three factors could slow execution:

- Major investment decisions (phased FePO4/LFP expansion, the PCl3 plant) require board approval. Until the board is fully rebuilt, such resolutions can be deferred.

- Credibility with foreign partners, particularly Japanese and Korean conglomerates known for strict ESG and compliance standards, may suffer while environmental and accounting allegations are under investigation.

- New investment inflows from partners or additional share issuance are hard to execute while the stock remains on the warning list.

The existing phosphorus business pillar is likely to continue running stably; but the two new growth engines — battery materials and the Nghi Son project — will depend on how quickly the board is rebuilt and how much partner trust is preserved.

Three governance signals to read at the May 8 EGM

Not to conclude buy or sell, but to assess governance risk over the next 6–12 months, individual shareholders should read three signals carefully.

First — the identity and independence of the 3 new board members. Do they come from outside (independent experts, institutional shareholder representatives) or are they internal promotions from the management ranks? The latter may move faster on operational knowledge, but creates a concentration-of-power risk similar to the pre-crisis structure. The share of independent members on the new board is the clearest signal.

Second — the 2025 audit timeline and commitment on exiting the warning list. At what risk level do A&C or UHY accept the audit mandate? Does the company commit to a specific date for publishing the fully audited statements? Is there a clear timeline from the investigation authority for returning the seized accounting records? These three questions directly affect the path back to margin eligibility.

Third — the continuity of the battery materials strategy. Does the new board reaffirm the FePO4/LFP/PCl3 plan, or defer it to focus on crisis management? Is the Q2/2026 commercial operation timeline for Nghi Son preserved in the EGM materials? These two answers will reframe DGC’s long-term growth story.

A pattern for reading governance risk

The DGC case illustrates a fairly specific risk pattern among listed companies in Vietnam: power concentrated in the founding family, combined with operations in a sector with high environmental and extractive risk. When these two factors meet, early warning signals tend to arrive in this order: (1) administrative environmental violations or prolonged tax inspections, (2) complex related-party transactions and cross-ownership, (3) low share of independent board members. The final signal — the stock entering the warning list — usually comes only after the chain above has accumulated visibly.

The May 8 EGM will answer most of the open questions on DGC over the next two weeks. The three signals above are observable directly from the resolutions and minutes, without waiting for the final investigation outcome.