During the week of April 20-24, 2026, both Mobile World Investment (MWG) and FPT Retail (FRT) will release Q1/2026 earnings. This is the first verification for two retail models that have moved in opposite directions after the smartphone market saturated. MWG targets a record VND 9,200 billion net profit for full-year 2026, up 30% from 2025.VnEconomy FRT targets VND 1,550 billion pre-tax profit — an all-time high, up 27% from 2025.Doanh Nhan Sai Gon

Looking at the baseline numbers: MWG closed April 19 at VND 86,900 per share with a market cap of VND 127.6 trillion; FRT at VND 152,100 with a market cap of VND 25.9 trillion. Sharing a phone-retail origin, the two companies now tell different stories to investors, and the market is pricing them under two separate logics.

Two paths from one starting point

When the smartphone market peaked around 2021-2022, both MWG and FRT were forced to find new segments. MWG scaled Bach Hoa Xanh into a grocery chain; FRT scaled Long Chau into the country’s largest pharmacy chain. Both are essential consumer goods — but the unit economics and cost structures diverge sharply.

MWG’s Q1/2026 is estimated at VND 46,000-47,000 billion in revenue and around VND 2,700-2,800 billion in net profit, up 80% year-on-year.CafeF Much of that growth comes from Dien May Xanh — still the profit engine, contributing more than 80% of group-level pre-tax profit. Bach Hoa Xanh only recently turned profitable and remains in a heavy CAPEX expansion phase.

FRT walks the opposite road. The 2026 consolidated revenue target is VND 59,500 billion, up 16% from 2025.DNSE In 2025, Long Chau delivered VND 34,500 billion in revenue, up 36% and exceeding plan by 7%, contributing 68% of FRT’s consolidated revenue.Doanh Nghiep Hoi Nhap Long Chau’s 2025 EBITDA reached VND 1,680 billion — shouldering 83% of consolidated EBITDA and improving nearly 76% versus 2024.

Axis 1: Expansion pace — heavy CAPEX vs lean

The first divergence is store-opening pace. MWG plans to open roughly 1,000 new Bach Hoa Xanh stores in 2026, with 30-40% located in the North and Central regions — meaning the chain is expanding beyond its traditional Southern stronghold. That equals a +44% increase in chain size, a very heavy CAPEX campaign.

FRT chose the opposite route. The 2026 plan adds 450 Long Chau outlets on top of 2,400 pharmacies and 220 vaccination centers at year-end 2025.Bao Dau Tu That’s a +19% expansion — less than half MWG’s pace.

The +1,000 and +450 figures are not just pace — they reflect two philosophies. MWG bets that scale drives operating leverage: warehousing, sourcing costs, and supplier negotiating power only pay off when the chain gets dense enough. FRT has shifted to an optimization phase: focus on margin per store, not total store count.

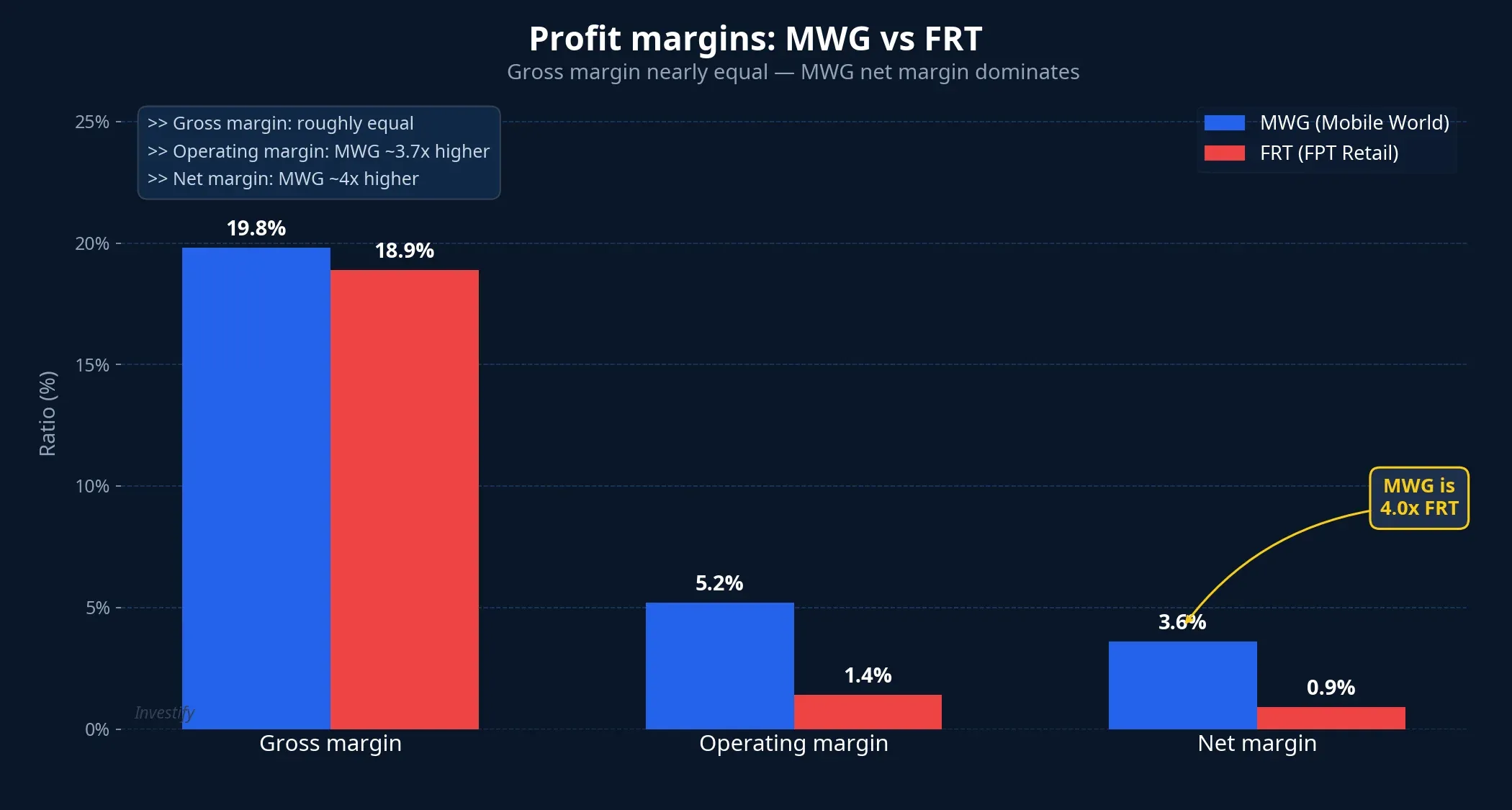

Axis 2: Unit economics — gross margins roughly equal, net margins 4x apart

This is where the two models separate most clearly, and where the data says what the industry label alone doesn’t.

On the surface, gross margins are roughly equal: MWG at about 19.8%, FRT at 18.9%. But at the operating margin level, MWG stands at 5.2% versus FRT’s 1.4% — a gap of nearly 3.7x. At net margin, the gap widens to 3.6% vs 0.9%, meaning MWG is 4x higher than FRT. This is not a price or product-cost difference — it is a difference in operating and financing costs.

At MWG, Dien May Xanh anchors net margin thanks to steady inventory turnover and fully depreciated store costs. Bach Hoa Xanh is only recently profitable, so the consolidated net margin still leans on the electronics arm. At FRT, Long Chau contributes most of the EBITDA, but the chain sits in a rapid-expansion phase — CAPEX for 2,400+ outlets still weighs on depreciation and interest costs, compressing net margin. Pharmaceutical gross margins typically outpace essential consumer goods, but the fixed costs for licensed pharmacists and vaccination centers eat that spread.

Axis 3: Valuation — the market is paying a premium for the high-margin story

At April 19 closing prices, MWG trades at a trailing P/E of about 18x, FRT at about 26x. If both hit 2026 targets (assuming a 20% tax rate for FRT), forward P/E compresses to roughly 17.6x (MWG) and 20.5x (FRT). The market is pricing FRT at a clear premium, and that premium reflects Long Chau growth expectations and the healthcare-ecosystem expansion story.

The key observation is that FRT’s premium mostly reflects future expectations. With MWG, the market has largely priced in Dien May Xanh’s earnings and is just starting to credit Bach Hoa Xanh’s contribution. If BHX delivers the planned 10% SSSG (same-store sales growth), MWG’s forward P/E has room to compress further. Conversely, if Long Chau slows down or margin dips, FRT’s premium faces a fast stress test.

Q1/2026 earnings: Three metrics per company, not the same on both sides

This is where many investors slip. There is no single reading framework for both ICT retail stocks — the key metrics differ on each side.

For MWG, three metrics to track:

- Net new Bach Hoa Xanh stores (openings minus closings) — to gauge progress toward the full-year 1,000-store plan.

- Bach Hoa Xanh SSSG — full-year target is 5-10%, and Q1 must show at least 5%.

- Consolidated gross margin — if it slips below 20% due to new-store launch costs, the VND 9,200 billion profit plan faces pressure from the opening quarter itself.

For FRT, three metrics to track:

- Q1 new Long Chau openings — must prove the 450-per-year pace is feasible.

- Long Chau gross margin — if it drops on price competition or expansion costs, the high-margin story gets tested.

- FPT Shop loss or margin — this segment is restructuring and must not become a drag on the VND 1,550 billion target.

12-month risks: two different risk types

MWG carries execution risk. 1,000 new stores, 30-40% outside the strong Southern base, mean higher logistics costs and longer ramp-up time. Fresh produce is exposed to supply-chain volatility and direct competition from traditional wet markets. Dien May Xanh remains the profit pillar, so any shift in electronics consumption drags consolidated earnings.

FRT carries concentration risk. Long Chau delivers 83% of EBITDA, so any change in pharmaceutical policy, rental pressure, or competition from other pharmacy chains hits the bottom line hard. Vaccination centers are a newer segment and need time to prove their financial contribution.

Conclusion: Two problems, two evaluation frameworks

MWG is the “scale + execution” story: VND 9,200 billion in profit only materializes if Bach Hoa Xanh opens all 1,000 stores and SSSG stays at 10%. FRT is the “high margin + concentration” story: VND 1,550 billion in profit depends almost entirely on Long Chau sustaining its opening pace and pharmaceutical margin.

The evidence doesn’t yet point to a clear winner. Both models have reasonable cases: MWG has scale and superior net margin; FRT has a growth story and valuation premium. The Q1/2026 earnings during April 20-24 will be the first concrete test.

The deciding factors are what Q1 reveals: store-opening pace and SSSG for MWG; Long Chau opening pace and gross margin for FRT. After this quarter, investors will have clearer data to choose an evaluation framework for each stock — instead of forcing a single formula onto two companies that no longer look alike.