On April 18, 2026, Hoa Phat Long An Steel Production and Trading — a subsidiary of Hoa Phat Group (HOSE: HPG) — officially inaugurated its steel pipe plant at the expanded Thuan Dao Industrial Park in Tay Ninh province. The event took place three days before the company’s annual general meeting, scheduled for the morning of April 21 at Melia Hanoi.VietTimes

This is not a market-moving event — HPG closed the April 20 session at VND 28,100, a market cap of VND 215.7 trillion, edging up just 0.36% in the two sessions after the launch. Over the past 30 days, HPG has gained roughly 4.9% (from VND 26,800 to VND 28,100), modestly outperforming the VN-Index over the same window. The price reaction is muted, but the strategic message is clear: Hoa Phat is locking in the final piece of its downstream value chain ahead of Dung Quat 2 lifting crude steel output to 16 million tons per year.

Thuan Dao plant: VND 2,600B, 15 ha, 460,000-ton capacity

The Thuan Dao plant sits on 15 hectares with total investment of VND 2,600 billion, a designed capacity of 400,000–460,000 tons per year.Tuoi Tre The integrated production line, imported as a turnkey package, manufactures black pipes, galvanized pipes and coiled steel for residential, industrial and infrastructure construction.

Four parameters stand out from a financial lens:

- International standards compliance — ASTM (US), BS EN (UK), JIS (Japan) — already deployed in flagship projects such as Long Thanh Airport and Tan Son Nhat Terminal T3.Phap Luat TP.HCM

- 10 MW rooftop solar system covers more than 50% of operational power demand — reducing energy cost and improving cost competitiveness.

- Over 800 local jobs, with the line running steadily since early 2026 before the official inauguration.

- Strategic location — Tay Ninh borders Ho Chi Minh City and the Mekong Delta, shortening delivery times to the southern market where Hoa Sen (HSG) and Nam Kim (NKG) currently dominate distribution.

The new plant lifts Hoa Phat’s total pipe capacity to 1.2 million tons per year, reinforcing its #1 domestic position with nearly 35% market share.SGGP

Why expand downstream when HRC is rising?

The natural question for investors: why is Hoa Phat sinking VND 2,600 billion into pipes — a downstream product — just as HRC (the input material) is climbing?

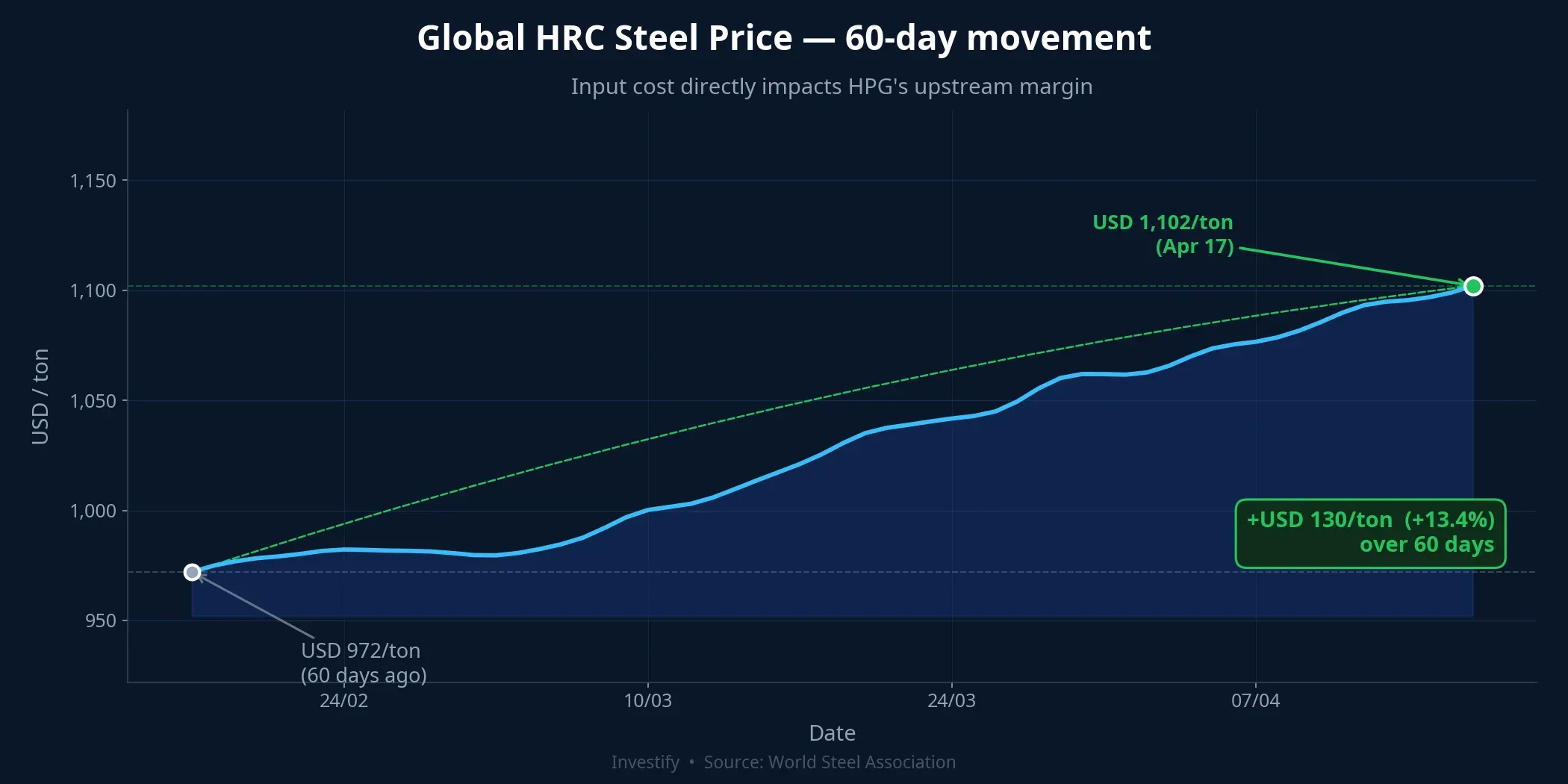

Global HRC prices have risen from USD 1,058/ton on March 17 to USD 1,102/ton on April 17, up 4.16% in a month.Trading Economics Since late January 2026, HRC is up roughly 13.4% (from around USD 972 to USD 1,102/ton). For HPG — which owns the full value chain from iron ore through pig iron, HRC rolling, to finished pipes — rising HRC is both an opportunity (upstream margin expands) and a risk (input cost for the pipe segment rises).

Expanding downstream in this context carries three layers of meaning.

First, it converts internal HRC volume into higher-margin finished pipes. Pipes can pass through HRC input changes into selling prices, while HRC itself is a globally traded commodity whose margin depends on the China cycle. When Dung Quat 2 reaches full operation by end-2026, Hoa Phat’s HRC output will exceed domestic demand. Self-consuming HRC through the pipe channel offers better margin control than dumping raw material into the market.

Second, it hedges the upstream cycle. When HRC prices fall, upstream margin compresses but pipe margin expands on cheaper input — provided pipe selling prices hold up. When HRC rises, pipes can still pass costs through. Combining upstream and downstream produces a less volatile consolidated EBITDA than HRC-only exposure.

Third, it defends southern market share against HSG and NKG. Hoa Sen leads in distribution networks, Nam Kim focuses on technology and exports — both have large plants in the south. Hoa Phat had previously concentrated in the north (Hung Yen) and central region (Dung Quat), so placing a 460,000-ton/year plant in Tay Ninh is a head-on competitive move, cutting delivery time and logistics cost for southern projects.

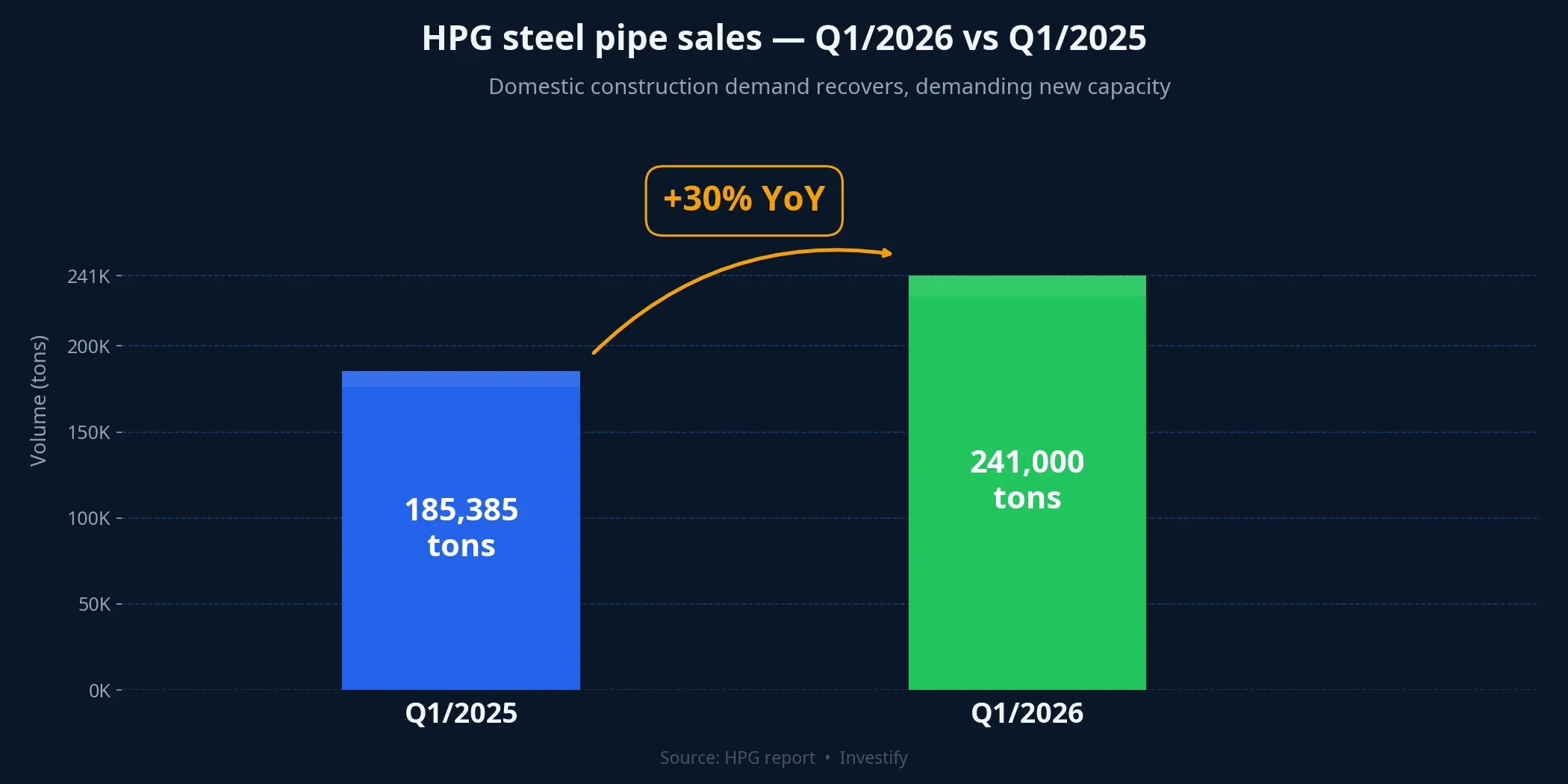

Q1/2026: pipe sales +30% YoY

The Q1/2026 print is a yardstick for the domestic construction cycle: Hoa Phat’s pipe sales exceeded 241,000 tons, up around 30% year-on-year. Combined with construction steel D10 prices climbing from VND 14,260/kg in early March to VND 15,430/kg on April 20 (+8.2% in six weeks), the data suggests the domestic construction cycle is in clear recovery — not just a wave of global commodity prices.

Three context points to frame the 30% number:

- Hoa Phat products are already deployed in major infrastructure projects: Long Thanh Airport, Tan Son Nhat Terminal T3. Public investment in 2026 is a direct driver of pipe demand — not just a function of the residential property cycle.

- The current ~35% pipe share is largely concentrated in the north and central regions. The Tay Ninh plant opens room to expand share in the south, where HPG is thin relative to HSG’s distribution reach.

- Pipe capacity rises from ~800,000 to 1.2 million tons (+50%), but if Q1 already absorbed 241,000 tons (close to 1 million annualized), the new capacity may not stay “surplus” for long if the construction cycle extends into 2027.

Four questions for the April 21 AGM

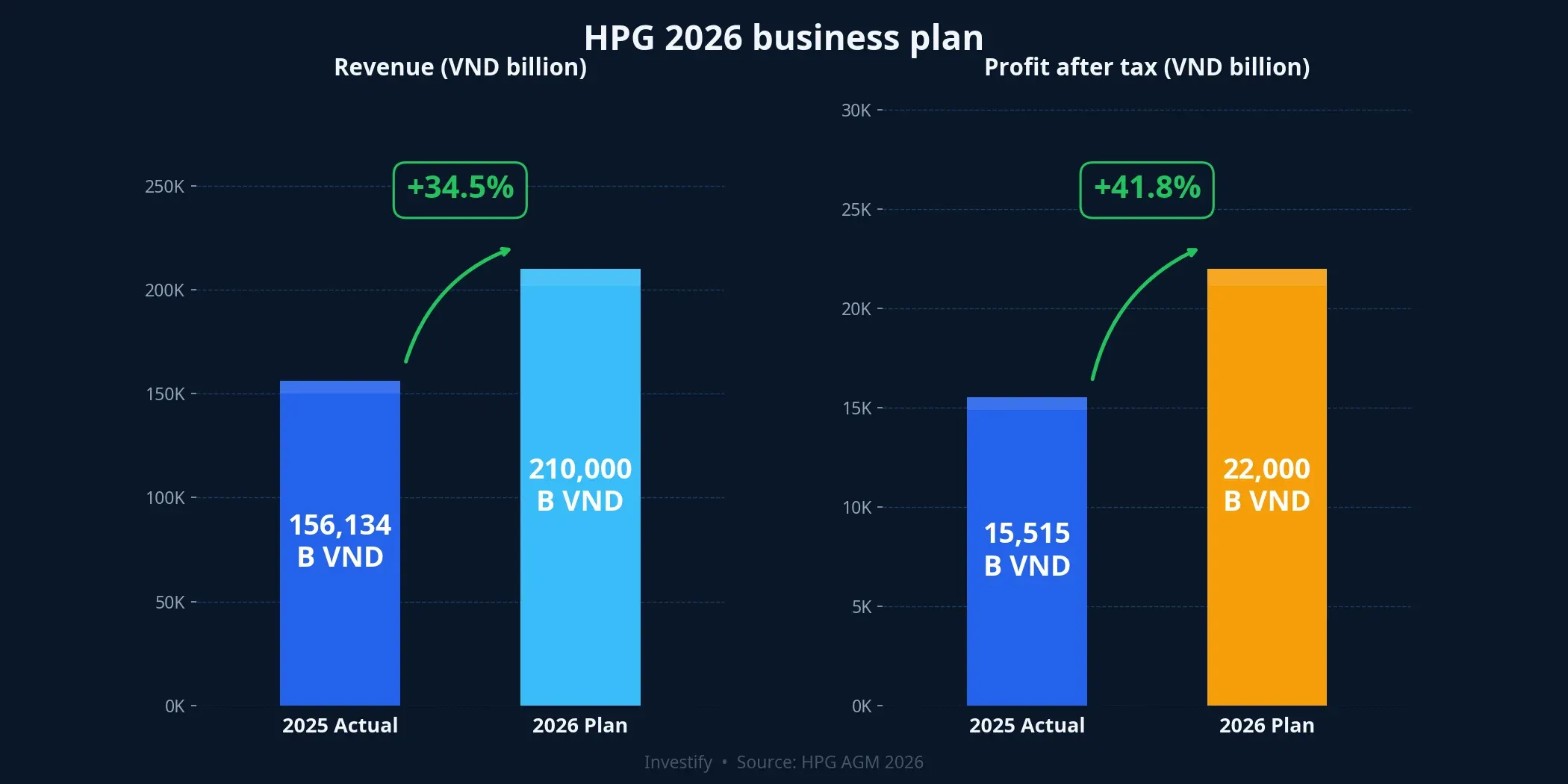

Hoa Phat has announced its 2026 plan: revenue of VND 210,000 billion (+34.5% vs 2025), profit after tax of VND 22,000 billion (+41.8%), dividend of 15% in cash and stock.CafeF The main driver is Dung Quat 2 — 280 ha, VND 85,000 billion in capex, blast furnace #2 already running since September 2025, expected to be fully completed by end-2026 to lift crude steel capacity to 16 million tons per year.Thi Truong Tai Chinh Tien Te

Four questions worth asking management:

- Pipe gross margin versus upstream HRC — with the Tay Ninh plant just operational, what gross margin does management expect for the pipe segment in 2026, and how wide is the spread versus HRC margin?

- Dung Quat 2 timeline — when exactly will blast furnaces #3 and #4 come online? How would a delay versus the end-2026 target affect the VND 22,000 billion PAT goal?

- Imported steel competition — how will trade-defense measures, particularly anti-dumping duties on Chinese HRC, affect domestic selling prices in 2026?

- Interest expense — as Dung Quat 2 enters full principal and interest repayment, how much will 2026 financial costs rise, and what is the specific impact on PAT?

Bottom line

The Tay Ninh plant is not a market-moving event — HPG’s muted price reaction has already reflected that. It is a deliberate strategic step: converting part of internal HRC volume into higher-margin finished pipes, defending southern market share against HSG and NKG, and completing the value chain ahead of Dung Quat 2 lifting crude steel output to 16 million tons per year.

Thesis for investors tracking HPG: the +41.8% profit plan is ambitious but has physical grounding — Dung Quat 2 unlocks upstream capacity, Tay Ninh absorbs part of that volume through a higher-margin pipe channel, and Q1 domestic construction demand has confirmed the recovery cycle. That said, the thesis is not without risk: it depends on three variables the April 21 AGM will help clarify — actual Dung Quat 2 progress, downstream margin from Tay Ninh, and the trajectory of global HRC prices in the second half of the year.

The Q2/2026 report and management commentary at the AGM are the next two data points to watch in confirming or adjusting the thesis.