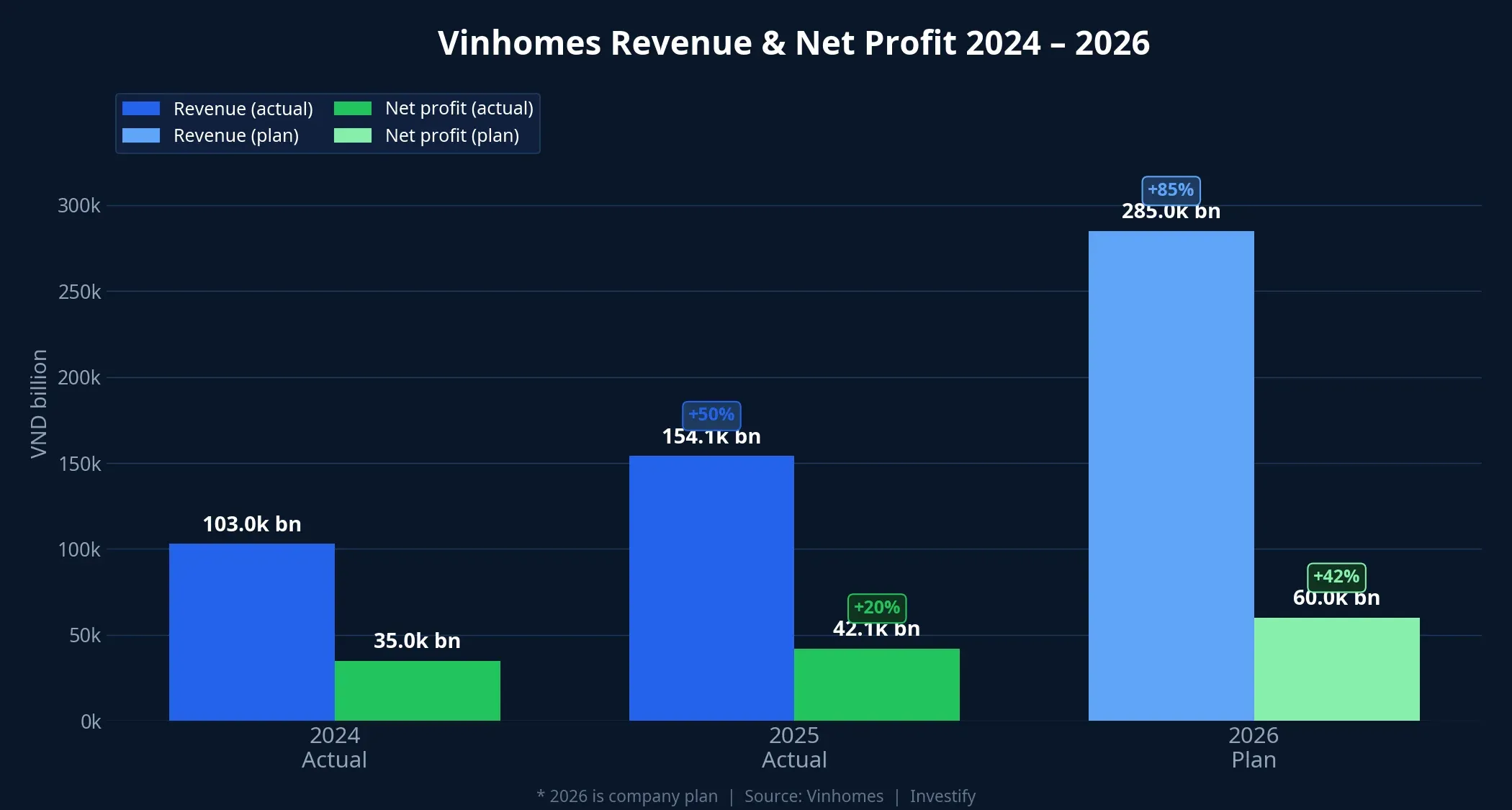

One day before its annual general meeting, the Vinhomes board submitted an upward revision to its 2026 business plan: consolidated net revenue raised to VND 285tn (VND 35tn above the prior plan); consolidated net profit raised to VND 60tn (VND 10tn above the prior plan).Tuoi Tre If delivered, this would be the highest profit figure ever booked by a listed Vietnamese company.

The market reacted immediately. On 20 April, VHM hit its 6.93% ceiling at VND 145,100 per share, with market cap reaching VND 596tn; VN-Index was pulled up by VHM and VIC to 1,837.11 points, a gain of 19.94 points. But the rest of the property sector did not benefit: HOSE real-estate stocks fell 1.11% that session, with 35 advancers, 41 decliners and 46 flat in the 122-ticker bucket. The extreme divergence is the first thing to read: investors are separating Vinhomes from the rest of the industry — they are not betting on a broad real-estate rally.

Looking at the numbers, this piece unpacks three layers: (1) where the VND 285tn revenue comes from, (2) why VND 60tn in net profit has no precedent, and (3) the VND 24,644bn cash dividend and the cash-flow question — the issues shareholders need to raise at the 21 April AGM.

Layer 1: Where the VND 285tn revenue comes from

The 2026 plan is not built on new assumptions but on an already-accumulated backlog. Vinhomes closed 2025 with consolidated net revenue of VND 154,102bn, adjusted consolidated total revenue of VND 183,923bn, and net profit of VND 42,111bn — 20% above the annual plan.Nguoi Do Thi More importantly, contracted sales in 2025 reached VND 205,252bn, up 98% YoY, and the volume of contracted sales not yet booked as revenue at end-2025 was roughly VND 186,400bn.

Put differently, more than 65% of the 2026 revenue plan is already “pre-ordered” from the end-2025 backlog. This is structurally different from a plan that depends on new launches: Vinhomes does not need to convince new buyers — it simply needs to hand over units on schedule to book most of the revenue. That is why the 85% revenue jump and 42% profit jump versus 2025 are not distant growth expectations, but a mechanical result of percentage-of-completion accounting, where sales booked in 2023–2025 are progressively recognised as revenue when construction milestones are hit.

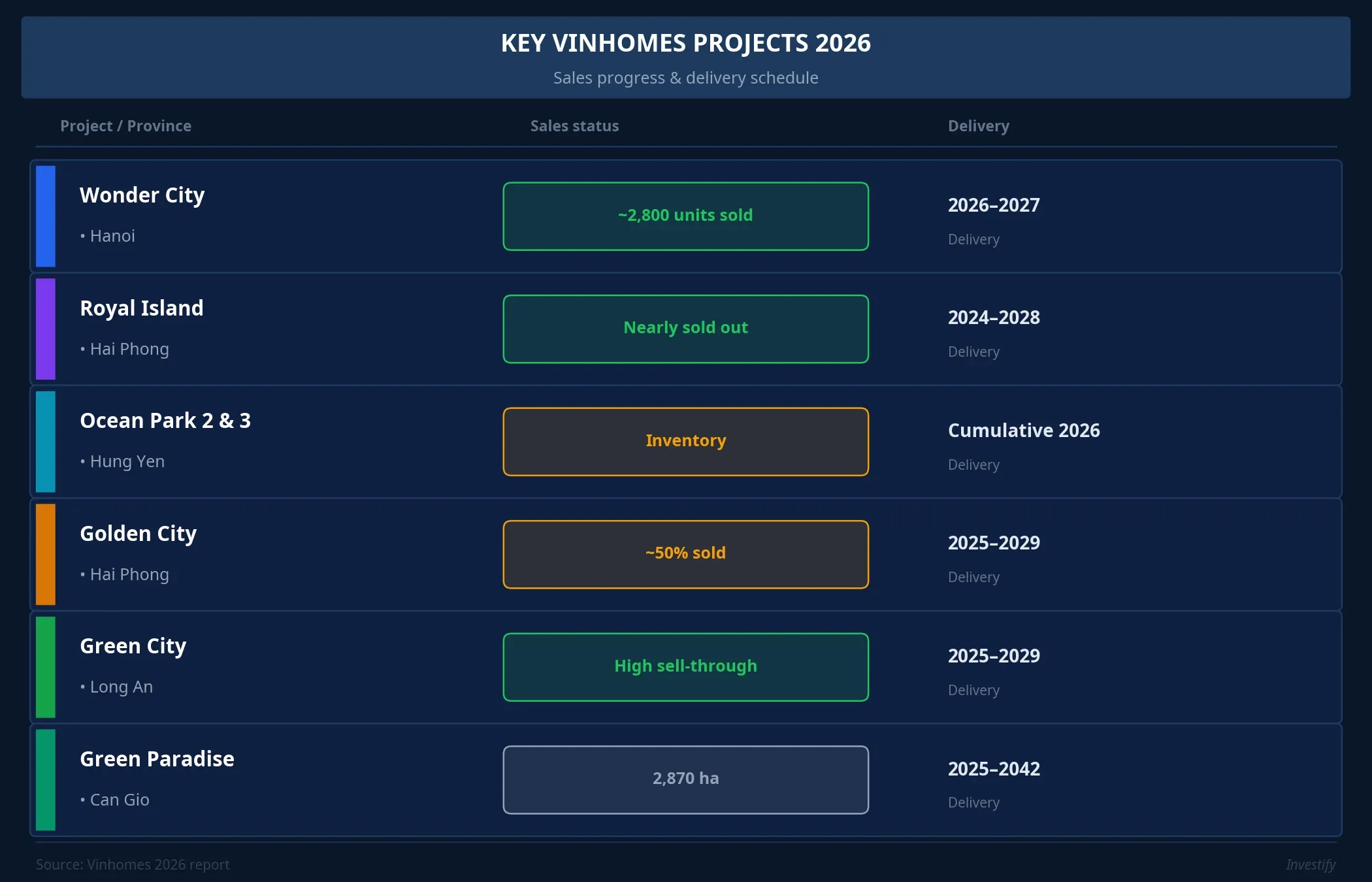

On project composition, 2026 is a “harvest” year for urban developments launched during 2024–2025. Wonder City in Hanoi, with roughly 2,800 units already sold, is the largest recognition driver for 2026. Royal Island in Hai Phong is nearly sold out, with a 2024–2028 delivery phase, and continues to contribute large revenue recognition in 2026. Ocean Park 2 and 3 in Hung Yen still carry inventory, with cumulative recognition rolling into 2026. Golden City in Hai Phong and Green City in Long An are in partial-recognition mode, with delivery phases spanning 2025–2029.

Green Paradise in Can Gio — 2,870 hectares, with total investment of around USD 10bn — contributes modestly to 2026 because its 2025–2042 delivery phase spans more than 15 years. This project is not the driver for 2026 results; the company positions Can Gio as the sales growth engine for the next three years — in other words, backlog for the 2027–2029 window.

Layer 2: Why VND 60tn has no precedent

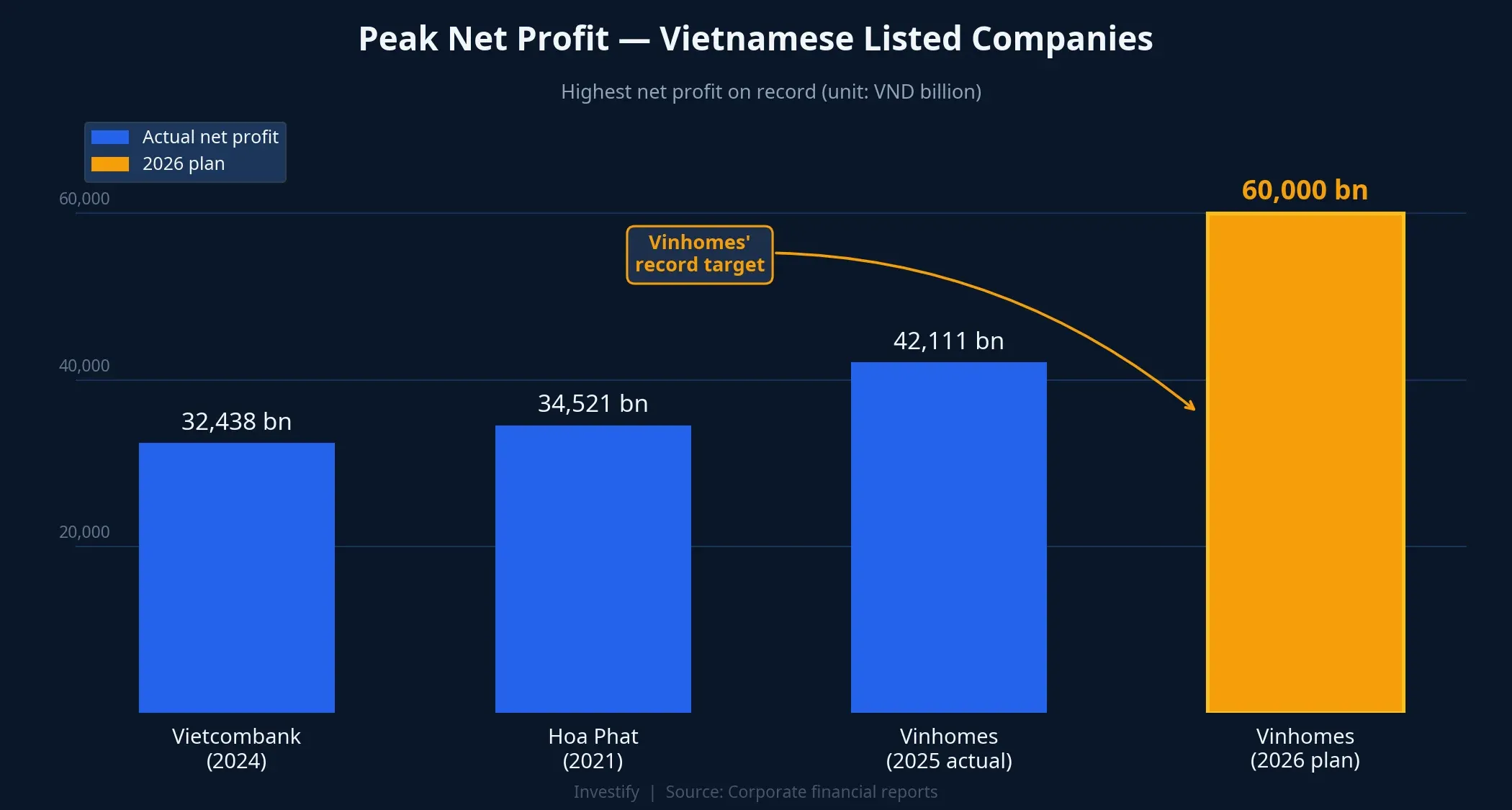

Placing VND 60tn next to the peak net-profit figures ever recorded by Vietnam’s largest listed companies reveals a meaningful gap. Vietcombank — the country’s top bank — hit its parent-only net-profit peak of VND 32,438bn in 2024.Dan Viet Hoa Phat, at the top of its 2021 steel cycle, posted VND 34,521bn.Tien Phong Vinhomes itself set its own company record in 2025 at VND 42,111bn.

The VND 60tn mark is nearly double Vietcombank’s peak and well above Hoa Phat’s record. Versus Vinhomes’ own 2025, the 2026 target is 38% higher. The notable point in the financial statements is that two factors let the Vinhomes model reach a margin profile that other industries cannot easily match. First, integrated high-end real estate supports a gross margin above 30%, versus roughly 10–15% in steel and 3–4% NIM in banking. Second, percentage-of-completion accounting concentrates the revenue of several sales years into a single fiscal year — unlike the recurring revenue streams of banking or manufacturing.

In other words, VND 60tn does not mean Vinhomes has suddenly outperformed the rest of the economy. It reflects the concentrated recognition cycle of a real-estate model when many projects hit their delivery phase together. This matters when reading the number: VND 60tn is large in absolute terms, but it is not a recurring revenue base that automatically repeats the following year.

Layer 3: VND 24,644bn dividend and the cash-flow question

Alongside the business plan, the board proposed a cash dividend of VND 24,644bn (60% of charter capital, VND 6,000 per share) plus a 100% stock dividend (1 share becomes 2).Tuoi Tre The total cash outlay is roughly USD 1bn — one of the largest cash-dividend rounds in Vietnamese equity-market history.

But three feasibility layers need to be separated to understand what the number is actually worth to shareholders.

Accounting profit is the most achievable layer. The VND 186,400bn end-2025 backlog covers most of 2026’s revenue. This is a construction-schedule variable, not a market variable — a risk that can be managed through execution capability and existing contractor systems.

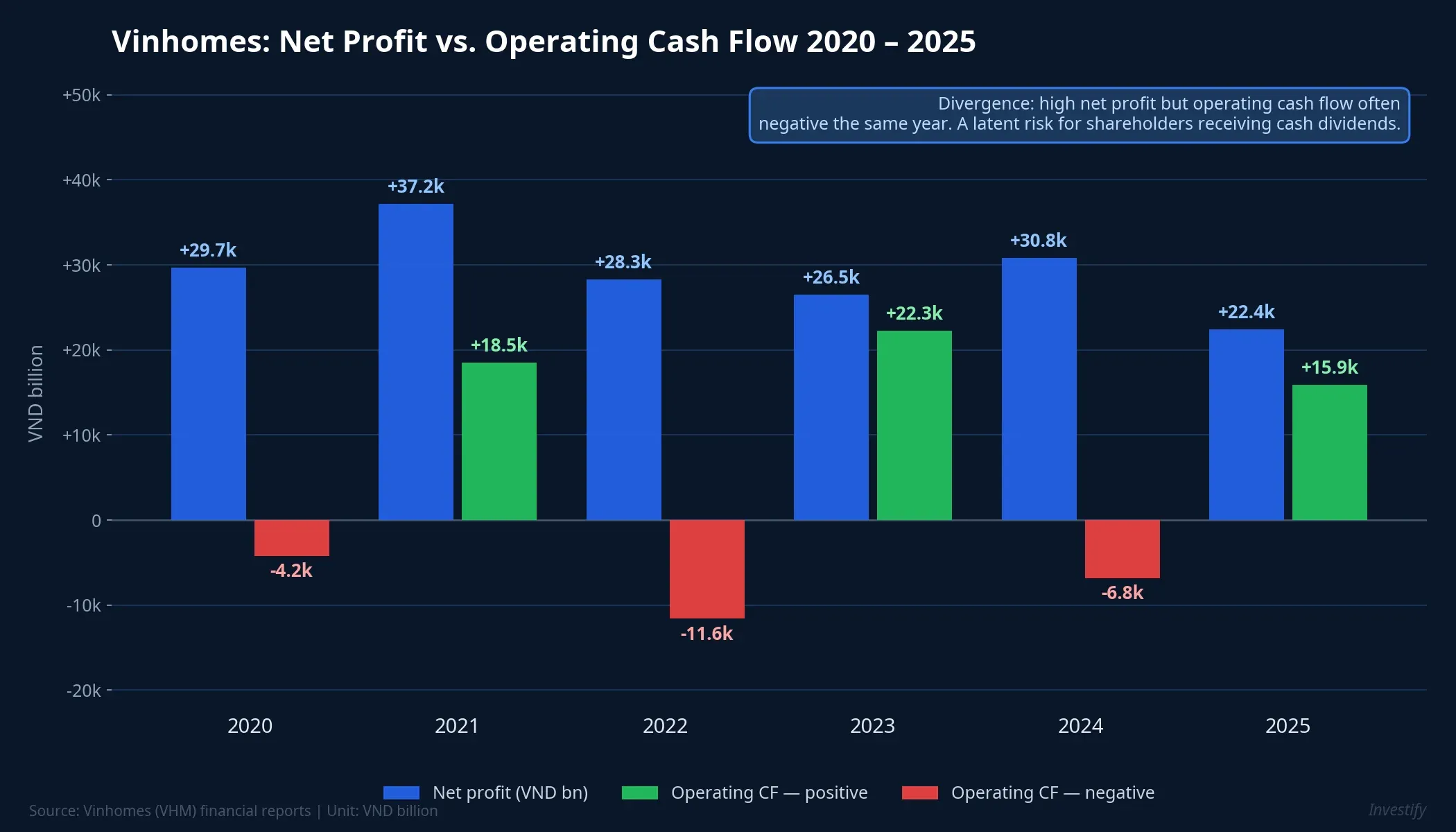

Real cash flow is a variable independent of accounting profit. Across the 6-year 2020–2025 cycle, operating cash flow diverged materially from net profit. In 2020, 2022 and 2024, operating cash flow was negative (−VND 4,200bn, −VND 11,600bn, −VND 6,800bn respectively) while net profit remained high at VND 29,700–30,800bn. In 2025, operating cash flow was +VND 15,900bn against VND 22,400bn net profit — a cash-conversion ratio of about 71%, still not high.

The cause of this divergence is the nature of the real-estate model: when ramping up launches, the company must fund land clearance, construction and acceptance upfront, ahead of collecting full customer payments under milestone contracts. When mass handovers happen in 2026, the question is what share of the VND 60tn profit will translate into actual cash inflow. Paying VND 24,644bn in dividends requires real cash, not accounting profit.

Credit conditions in 2026 are a systemic variable. According to market forecasts, 2026 is the peak year for corporate real-estate bond maturities, with pressure concentrated in Q4. Credit-disbursement pace in real estate and mortgage rates will determine the absorption speed at new projects — particularly Can Gio and the next phase of Wonder City. If credit conditions tighten, sales velocity could slow, affecting the 2027–2028 backlog even if the 2026 result is unaffected.

Why only VHM rose while real estate sector fell on 20 April

Back to the opening point: VHM hit its 6.93% ceiling while HOSE real-estate stocks fell 1.11%. This is not a “real-estate sector recovery” story — it is an “investors separate Vinhomes from the rest of the sector” story. The VND 186,400bn backlog and the VND 60tn net-profit target are assets that other listed developers do not have — Novaland, Dat Xanh, Phat Dat, and Khang Dien are all at different points in their cycles. Money flowed into VHM because of backlog quality, not because of expectations for a broad sector wave.

This matters for how to read the session: the VHM signal should not be extrapolated to the full listed real-estate bucket. The Vinhomes story is a story of specific projects — Wonder City, Royal Island, Green Paradise — not a story of interest rates, policy shifts, or cyclical recovery waves.

Three questions shareholders need to raise at the 21 April AGM

The VND 60tn plan needs three layers of validation to convert from commitment to result. Each layer maps to a specific question:

- Specific handover schedule — quarterly milestones for Wonder City, Royal Island, and Ocean Park 2 and 3 in 2026. A one-quarter slip is enough to push VND 10,000–15,000bn of revenue into 2027.

- Profit-to-cash conversion ratio — the plan for collecting cash from customers so the VND 24,644bn cash dividend can be funded without additional borrowing.

- Financial plan for 2026 bond maturities — debt structure, refinancing channels, and the average interest rate Vinhomes currently pays.

These three questions are the reality check on the VND 60tn figure. A business plan is only a commitment; cash-flow quality and delivery pace are the mechanisms that confirm that commitment. From a financial-statement perspective, the Q1/2026 reporting season — expected late April — will show whether Vinhomes has already booked the first VND 6,000bn of net profit, and whether Q1 operating cash flow is positive. That is the first signal of whether the VND 60tn plan is on track, or whether expectations need to be recalibrated.