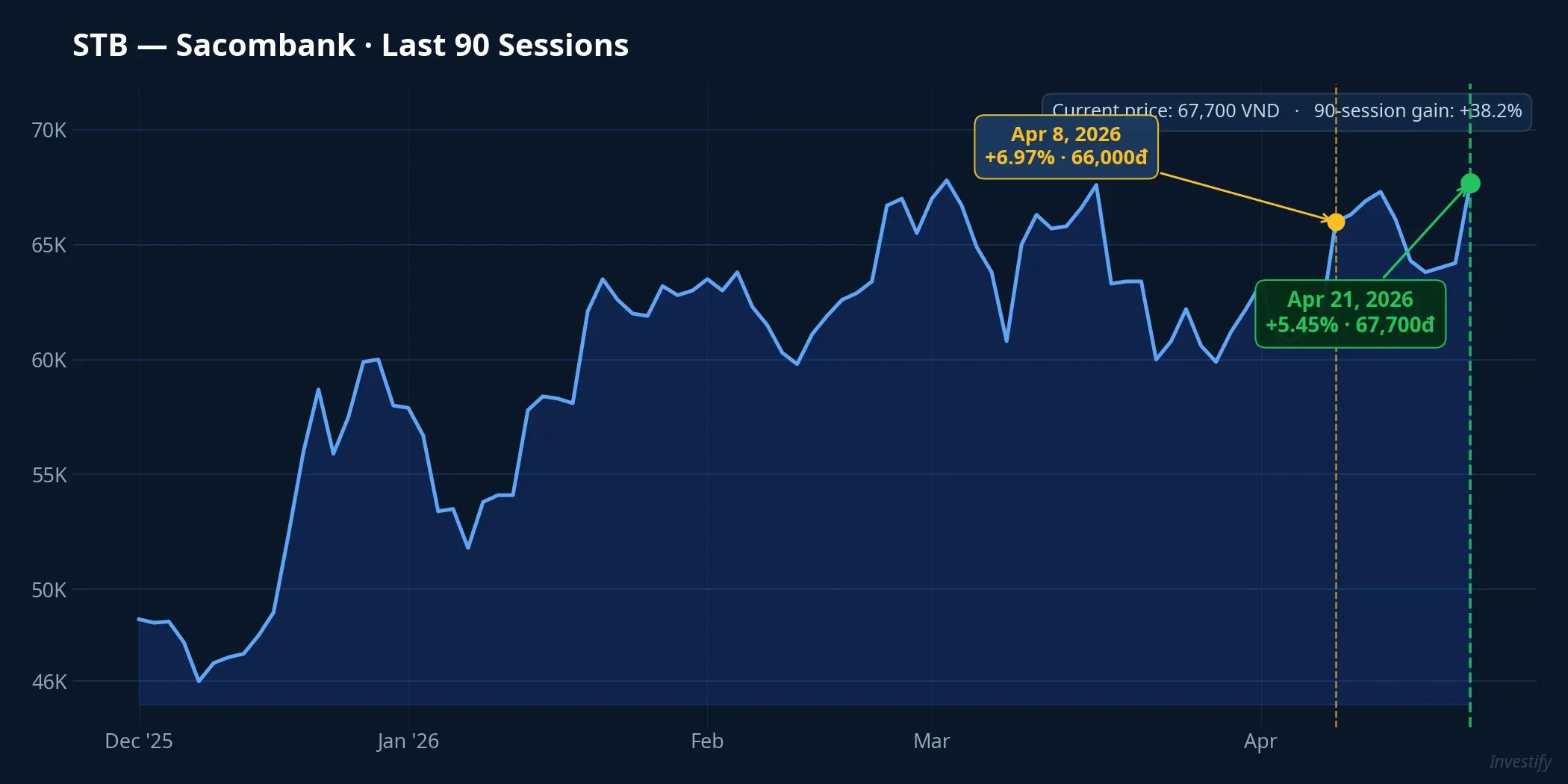

On April 21, 2026, STB closed at 67,700 VND, up 5.45% on volume of 14.1 million shares, briefly hitting the ceiling at 68,600. The move came exactly one day before Sacombank’s 2026 annual general meeting at Saigon Hotel – Phú Thọ. On its own, 5.45% is not a shocking move for a bank stock with a 127.6 trillion VND market cap. But placed next to the three items Sacombank just added to the meeting agenda, the number tells a story Vietnam’s market has seen before.

The three additions: CEO Nguyễn Đức Thụy (widely known as Bầu Thụy) stands for election to the board, the bank proposes renaming to “Saigon Treasure Commercial Joint Stock Bank” (Sài Gòn Tài Lộc), and it plans to relocate its headquarters from 266-268 Nam Kỳ Khởi Nghĩa.VnExpress This is the fourth time Vietnam’s market has watched the same pattern take shape around Bầu Thụy: take operational control, rebuild the brand, reposition the strategy. This post unpacks those three layers through LPBank, HAGL and Hưng Thịnh, then places Sacombank against them — to answer the question retail investors are holding: is 67,700 VND pricing in one man, one piece of news, or a belief about a name change?

The three layers of the “change clothes, change fortune” playbook

Layer 1 — Take operational control. At LPBank, Bầu Thụy took the chairmanship in late 2022 after Huỳnh Ngọc Huy stepped down for personal reasons.VietTimes At Sacombank, the sequence repeats in a slightly different form: the State Bank of Vietnam approved his appointment as CEO, he officially took office on March 3, 2026, and he is now standing for the board.DNSE If the April 22 AGM approves his nomination, he will simultaneously control execution (as CEO) and hold a seat shaping strategy (on the board) — the same configuration he started with at LPBank.

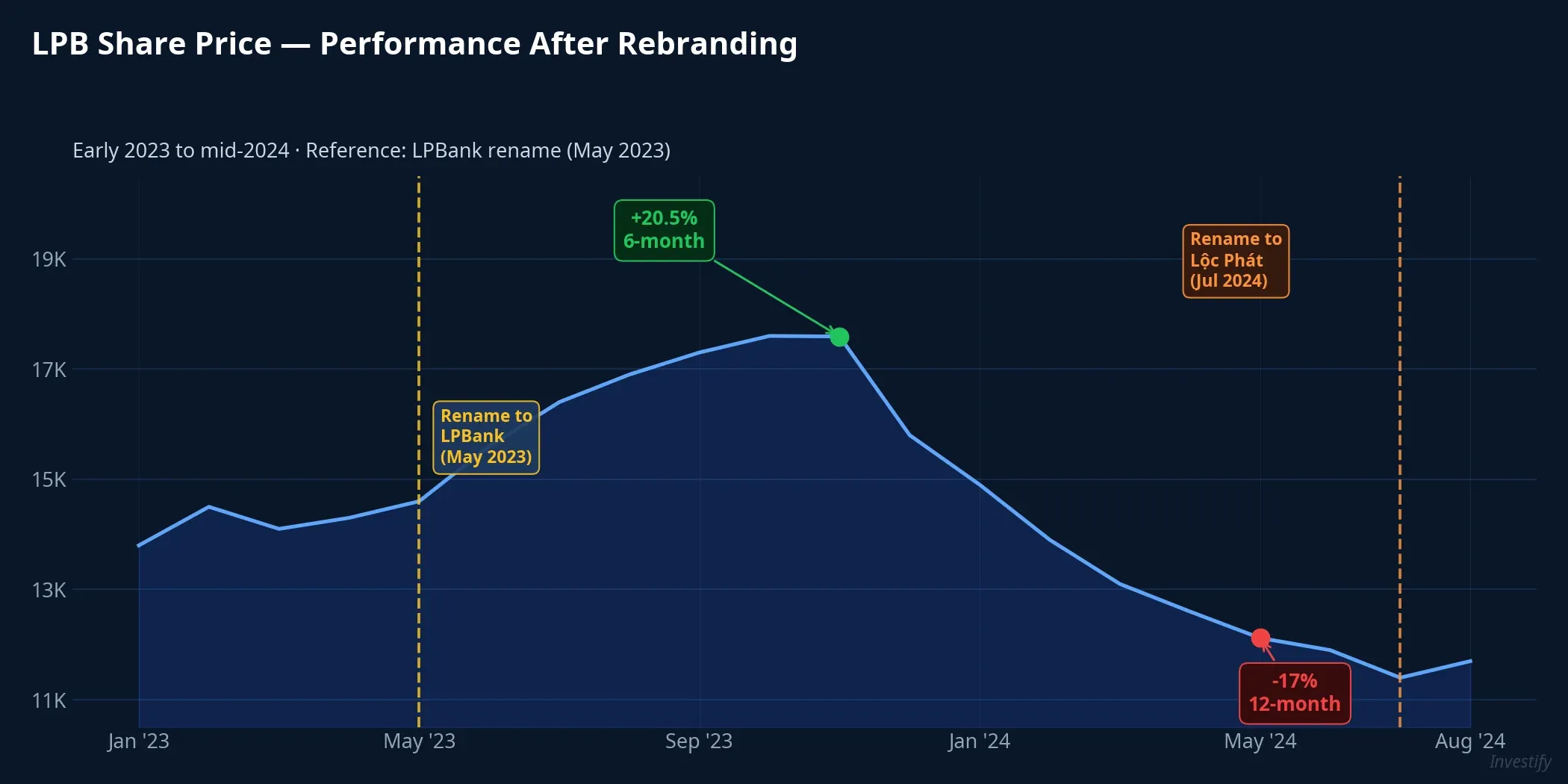

Layer 2 — Rebuild the brand. In May 2023, the central bank approved renaming LienVietPostBank to LPBank — exactly one year after Bầu Thụy took the chairmanship.NhaDauTu In July 2024, the full legal name changed again to Lộc Phát Vietnam Commercial Joint Stock Bank.VnExpress At HAGL and Hưng Thịnh, this layer shows up as new logos and refreshed visual identities; Hưng Thịnh unveiled its new brand identity in July 2024, a year after receiving a 5,000 billion VND credit line from LPBank.DNSE At Sacombank, layer 2 is now on the AGM table: new name (Saigon Treasure), new English trading name, new headquarters.TuoiTre

Layer 3 — Reposition the strategy. This is the hardest layer to observe from the outside, and the one that actually decides whether shareholders are rewarded. At LPBank, layer 3 meant doubling down on retail banking, leveraging the postal network, issuing large credit facilities to real-estate partners, and resuming cash dividends. At HAGL, support from Thaiholdings and LPBank helped the group refocus on agriculture instead of spreading itself thin.TheLeader At Sacombank, layer 3 has yet to appear. Pulling the proposal to extend its post-merger restructuring plan merely signals that the bank believes an old chapter is closing — not that a new chapter has been announced.

Does price history actually support the rebrand story?

LPB is the longest and most complete sample among the four iterations. After the May 2023 rename, the share price nearly doubled in the first six months of the year, reaching 31,600 VND on July 16, 2023.CafeF But when the observation window is stretched, the picture gets more balanced: measured from the reference rename date, LPB gained roughly 20.5% over six months and was down roughly 17% over twelve months. In other words, layer 2 (the rename) quickly lifted sentiment on repositioning hopes, but the medium-term return depended entirely on whether layer 3 delivered real business results.

Thaiholdings and the broader ecosystem around Bầu Thụy show a similar shape: strong positive reactions around governance changes, followed by differentiation based on operating results. HAGL and Hưng Thịnh are not directly listed under his name, so their price paths are harder to compare, but industry reporting notes that every time his capital touches a business, that business changes its logo.CafeF The pattern is recognizable. The business outcome, case by case, is not. That is the distinction retail investors need to hold on to.

Why did the market price in April 21 the way it did?

Three plausible explanations coexist, and the evidence leans toward a combination rather than a single driver.

- Pricing the operator. Bầu Thụy joining the board while keeping the CEO seat collapses execution and strategy into one node, reducing internal friction. This is the explanation most consistent with a 5.45% single-session move on a 127.6 trillion VND market cap bank.

- Pricing the end of an old chapter. Withdrawing the extension request for the restructuring plan is a quiet signal that the asset base is close to normalized. The restructuring has been largely complete since end-2024, with only one secured loan still being worked out — if that chapter fully closes, STB regains the room to pay cash dividends.BaoMoi

- Pricing the rename expectation. The weakest leg to explain a single-session move. A rename doesn’t change the bank’s future cash flows; it only signals direction. The belief that “Saigon Treasure” will outsell “Saigon Thương Tín” in retail is just that — a belief, not a fact.Vietstock

(1) and (2) most likely carry the heavier weight in the 5.45% April 21 print; (3) contributes but isn’t the primary driver. Worth noting: on April 8, 2026, STB also jumped 6.97% to 66,000 — meaning the market was already paying for restructuring expectations before the supplementary AGM agenda was even filed. April 21 is the confirmation trade, not the triggering trade.

Three questions retail should watch on April 22

Before deciding how to position around STB, three items worth watching at the meeting are the ownership structure, the forward business roadmap, and the chairman’s view on the new positioning.

Ownership structure after the AGM. After the supplementary board election, how many seats will be controlled directly or indirectly by shareholders aligned with Bầu Thụy? How is that bloc’s relationship with Chairman Dương Công Minh (in seat since 2017) structured? This is the core question that decides who actually runs layer 3.

A concrete business roadmap. Renaming and relocating are layer 2. Will the bank simultaneously announce layer 3 — which segments it wants to grow, which it plans to trim, what the 2025-2026 dividend plan looks like? The dividend resolution and updated profit plan are the metrics that can actually be priced. Without them, 67,700 VND is carrying a premium for conviction, not for expected earnings.

The chairman’s view on the new positioning. “Saigon Treasure” is a significant departure from the “Saigon Thương Tín” ethos, both in name and in market positioning. Dương Công Minh’s remarks at the meeting will reveal whether the rename reflects long-standing internal consensus, or a decision being finalized in the AGM season itself.

Compared against peers on P/E and P/B, STB sits in a balanced spot: P/E notably above VCB, MBB and CTG; P/B below VCB but above the two mid-tier banks. That spread reflects repositioning expectations — but also reminds us that the current price already runs ahead of a story that has not fully happened yet.

Bottom line: layer 2 is in, layer 3 is still outstanding

The thesis of this post fits in one sentence: April 21 is the confirmation trade for layers 1 and 2 of a familiar playbook (operational control centralized, brand rebuilt), while layer 3 (strategic repositioning) is still absent — and layer 3 is the variable that decides the post-AGM price path. The LPB analogue matters here: layer 2 can lift the stock quickly in the first six months, but the 12-month outcome depends entirely on whether layer 3 delivers real earnings.

Three specific signals to watch immediately after the April 22 AGM: (i) the new board composition and how roles are split with Chairman Dương Công Minh, (ii) the dividend resolution and 2026 profit plan, (iii) the timeline for resolving the remaining secured loan that would formally close the restructuring program. If the meeting only confirms layer 2 without revealing layer 3, the gap between “nominal restructuring” and “substantive restructuring” will be the dominant factor in STB’s price over the next 3-6 months.