The first plenary session of the 16th National Assembly on 21 April 2026 placed two numbers side by side. Real estate credit outstanding rose from VND 1,955 trillion in 2021 to VND 4,541 trillion in 2025 — a 132% increase over four years.VOV That pace was 2.4 times the rate at which credit flowed into industry over the same period.Vietstock

Those figures frame the proposal that followed from MP Le Hoang Anh (Gia Lai delegation): a progressive tax on second and subsequent homes or plots of land that are neither used nor rented out; escalating fees on projects stalled for more than 24 months; a Hanoi pilot via the amended Capital Law in the current session, then TP.HCM expansion via the Special Urban Law expected to be tabled in the second session in late 2026.Tuoi Tre Revenue would flow into social housing funds, old apartment refurbishment, and urban infrastructure.

This is a proposal, not yet law. But along the legislative path the National Assembly is pursuing — Hanoi pilot, then expansion via the Special Urban Law — real estate stocks had enough information to start repricing policy risk on the same day.

One number on the Assembly floor

Looking at the five-year credit series, the acceleration was uneven: growth picked up sharply from 2023 onwards, when the low-rate cycle and the Land Law 2024 framework reopened credit channels to real estate.

Alongside the credit series, the delegate presented a second figure: the price-to-income ratio for housing in major cities now ranges from 25 to 30 times — the highest in Southeast Asia.Dan Tri Put together, the two numbers build the policy frame: credit is flowing into real estate faster than into industry, while housing affordability for urban residents is shrinking. That is the backdrop in which any property tax proposal finds enough political room to be seriously debated.

21 April session: realty stocks split within the day the proposal was tabled

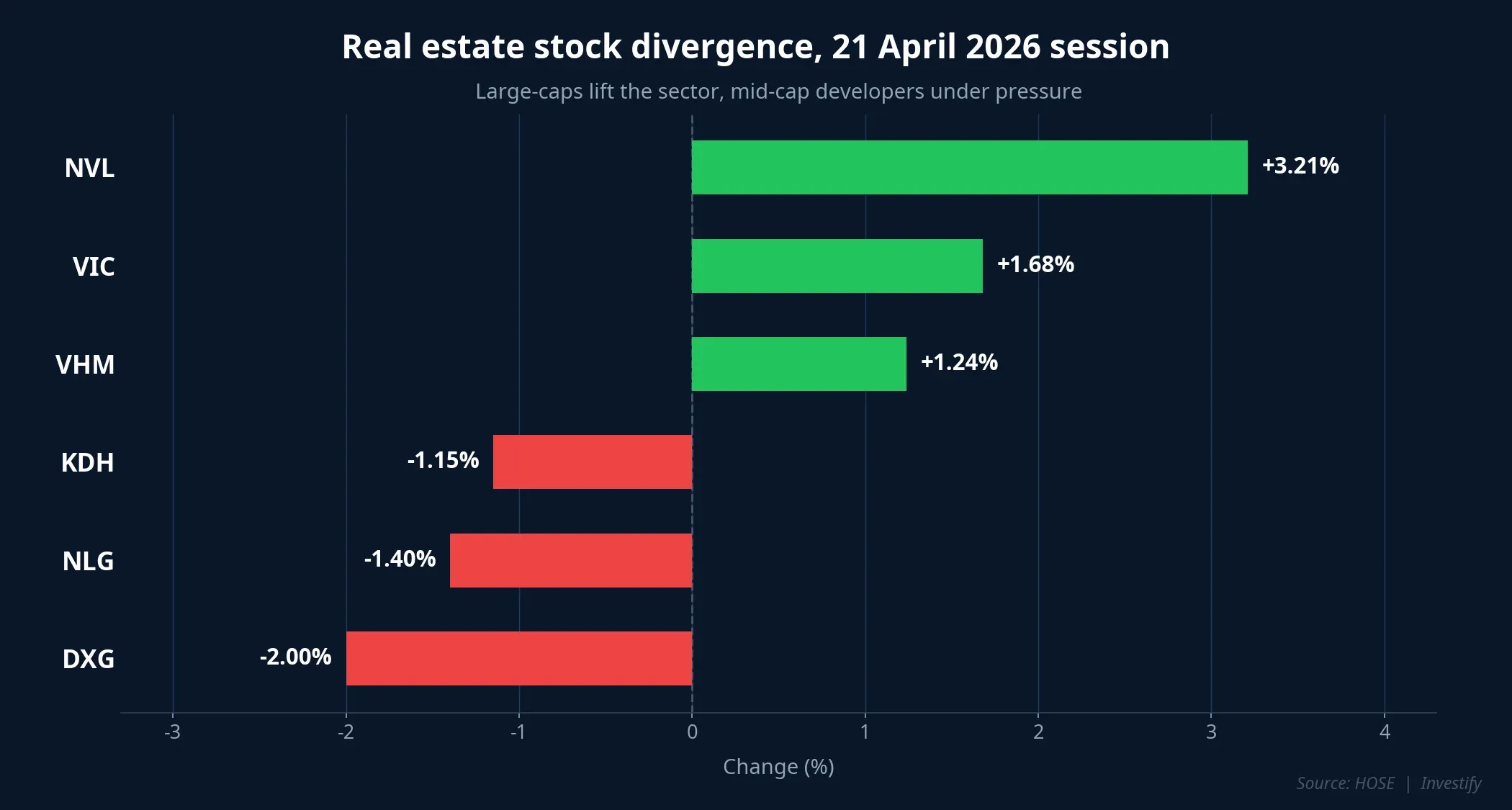

The real estate sector was among the strongest performers on the VN-Index on 21 April, rising 1.86% as a group,FireAnt even as the broader index slipped 0.20% to close at 1,833.48 points. But the internal breadth was nearly balanced: 35 advancers, 35 decliners, and 52 unchanged out of 122 listed names. Divergence began on the same day the policy news appeared.

Six representative tickers show two clear tiers. VIC (+1.68%), VHM (+1.24%), and NVL (+3.21%) — large caps tied to restructuring ecosystems and visible pipelines — pulled the sector up. In contrast, KDH (−1.15%), NLG (−1.40%), and DXG (−2.00%) — mid-cap developers with a heavier weighting in mid-to-high-end commercial housing and as-yet-undelivered projects — came under pressure within the session.

This was not a sentiment reaction. The market began sorting companies by exposure to two policy variables: (1) the share of undeveloped land bank, and (2) the weighting of second-home and speculative segments against genuine housing.

Three policy paths, three pricing responses

Along the current legislative process, the proposal faces three likely paths, each producing a different valuation frame for listed real estate stocks.

Scenario A — The Capital Law passes the tax clause in the current session. Hanoi gains authority to levy a progressive tax on unused second homes and fees for stalled projects. The transmission works in three layers: investors holding a second apartment must rent it out or sell it, pushing secondary supply into the market over the first 6–12 months of the pilot; developers with Hanoi land banks but projects frozen over 24 months face a choice between rapid build-out or paying the fee; speculative capital rotates into satellite provinces or exits real estate temporarily. Subjective probability is low-to-moderate — passing a second-home tax clause within a single session is an aggressive track for a newly introduced proposal.

Scenario B — The proposal is logged and sent to the drafting committee for study. The Assembly refers it to the Ministry of Finance and the State Bank for impact assessment, with no final decision in 2026. The market continues pricing in partial policy risk on real estate names, especially those with a high speculative weighting or large undeveloped land banks. Sector-internal volatility stretches over 3–6 months, tracking every statement from SBV or the Ministry of Construction leadership. This is the natural track for a systemic proposal that lacks a standardized land-ownership database — subjective probability moderate-to-high.

Scenario C — The proposal is upgraded into nationwide policy via the Special Urban Law. The Capital Law passes in pilot form, and the Special Urban Law for TP.HCM is tabled in the second session of late 2026 with an expanded tax clause. Early signal: the Ministry of Finance adds a Property Tax Law revision to the 2027 legislative agenda. Both Hanoi and TP.HCM then apply a common progressive tax frame, urban real estate reprices as the speculative segment cools, and the genuine rental segment expands. Low probability within 2026, moderate when extended to 2027–2028.

Two groups of companies, two degrees of impact

The key feature of the proposal is a clear scope: only second homes that are neither used nor rented out are taxed. Assets with a transparent rental cash flow are, in principle, outside the progressive tax. That scope creates two groups of companies with different valuation trajectories.

Under pressure are developers heavy in second-home, resort, and eco-city segments, and those with large-scale projects still undelivered. These are businesses whose undeveloped land bank accounts for the bulk of valuation — if the stalled-project fee is applied, land-holding cost rises directly, dragging down NAV and forcing either pipeline acceleration or partial divestment.

Indirectly benefiting are developers focused on mid-priced genuine housing, social housing, industrial parks, and urban infrastructure. The proposed tax revenue is earmarked for social housing funds and old-apartment refurbishment. Over the next 3–5 years, if this path is implemented, developers in affordable segments may see more stable order flow from public housing programs.

A clarification: this is a classification by pipeline composition, not by specific tickers. A single company can develop both high-end housing and affordable land banks — net impact depends on the weighting of each segment in the 2026 financial report and the disclosure cadence at upcoming AGMs.

Signals to watch

These three scenarios are not mutually exclusive in time. Scenario B may play out first, then shift into A or C depending on the Capital Law and the Special Urban Law timelines. Current evidence points to Scenario B as the base case for the next six months — but two specific events can reframe this quickly.

First, the vote on the amended Capital Law in the ongoing session. If the second-home tax clause is inserted into the draft at the final round of debate, Scenario A shifts from low to moderate probability within weeks. If the proposal is merely logged as a policy suggestion, Scenario B becomes the dominant track.

Second, the Ministry of Finance’s 2027 legislative agenda. If a Property Tax Law revision is added to that agenda, it signals that the proposal has been upgraded to long-term policy status, paving the way for Scenario C.

The VND 4,541-trillion figure is now on the Assembly floor. The policy clock has started — and the market, through the 21 April divergence, has already begun pricing the sector differently before and after that day.