On 20-21 April 2026, the Vietnam Gold Traders Association (VGTA) sent the Prime Minister a letter with two headline proposals: allow jewellery manufacturers to import raw gold on an annual plan of roughly 50 tonnes (around 5 billion USD), and let companies borrow gold directly from households at negotiated interest rates to ease import pressure.Dân Trí In parallel, the State Bank of Vietnam is finalising a draft amendment to Decree 24/2012/ND-CP that would end the SJC production monopoly and open licensing to qualified credit institutions and companies.

The prevailing narrative on Vietnamese financial social media is simple: supply liberalisation plus domestic gold mobilisation will compress the SJC premium toward zero, bar-gold holders win, and the market reaches “international standard”. The logic sounds clean — but three pieces of data don’t fit, and all three are precisely why Decree 24 was written in the first place.

The 2008-2012 lesson isn’t history trivia, it’s the reason Decree 24 exists

From 2008 to 2012, Vietnamese commercial banks were allowed to mobilise gold from depositors and lend it to businesses. When the global financial shock sent gold prices swinging, several banks fell into a short-gold position: they had sold mobilised gold for VND, then faced the obligation to repurchase gold at higher prices to repay depositors. Losses compounded, liquidity tightened. In 2009, domestic gold in Vietnam briefly spiked above 29 million VND per tael because of import restrictions — a live demonstration of how fragile the system was under supply shocks.

That episode is the reason Decree 24/2012 was drafted: ban gold mobilisation, ban gold lending, remove gold from bank balance sheets, nationalise the SJC brand. It was a situational fix. It solved the systemic risk at the cost of a persistent price premium.

The current proposal puts gold back on a balance sheet — this time of jewellery firms rather than banks — using the same type of operation that caused the earlier instability. The nominal difference (jewellery firms aren’t payment intermediaries like banks) doesn’t eliminate short-gold risk. It just shifts who carries it.

The three risks experts are flagging are all mechanism risks, not market risks

Compiling commentary from Dân Trí, Người Quan Sát and a Sài Gòn Times analysis, the concerns resolve into three mechanism gaps that need a legal framework before rollout — not three vague worries.

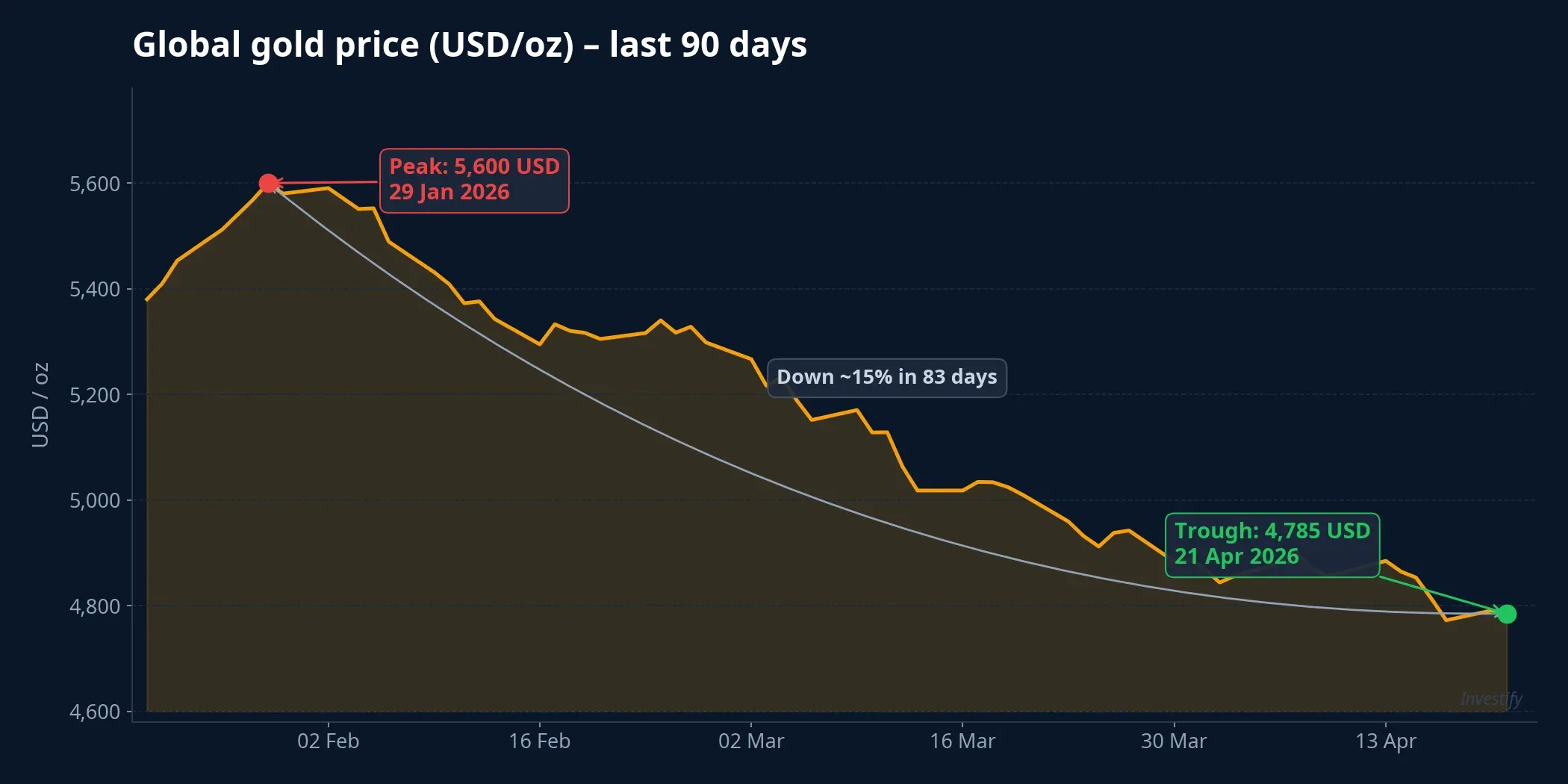

Mechanism 1 — price volatility plus leverage. If a company borrows gold at a negotiated rate, sells it for VND and uses the proceeds as working capital, it is taking on exactly the exposure banks carried in 2008-2012. Global gold has moved from a peak of 5,600 USD/oz on 29 January 2026 to 4,785 USD/oz on 21 April — a roughly 15% swing in 83 days.VietnamPlus A 10-20% reversal isn’t rare for gold, and it is more than enough to blow up the borrower’s position without a hard leverage cap written into the contract.

Mechanism 2 — settlement and accounting framework. There is currently no standard guidance for how to book, tax, or invoice gold-denominated transactions instead of VND ones. How should a borrower account for price movements between reporting periods? How are VAT and corporate income tax applied to the price differential between borrowed and returned gold? Without this framework in place first, the accounting and tax risk gets pushed down the contract chain onto depositors — the weakest party in the stack.

Mechanism 3 — who issues gold certificates. If the scheme expands into gold certificates — an idea Vietnam is drawing from India, Thailand, and Turkey — the decisive question is who issues and who absorbs price differentials on reversals. In India, Sovereign Gold Bonds (SGB) are backed by the central bank and the finance ministry; price risk is absorbed by the budget. If Vietnam lets commercial banks or jewellery firms issue certificates without risk caps and governance standards, the 2008-2012 scenario can repeat with a new issuer — same structure, different nameplate.

The SJC premium isn’t only about monopoly

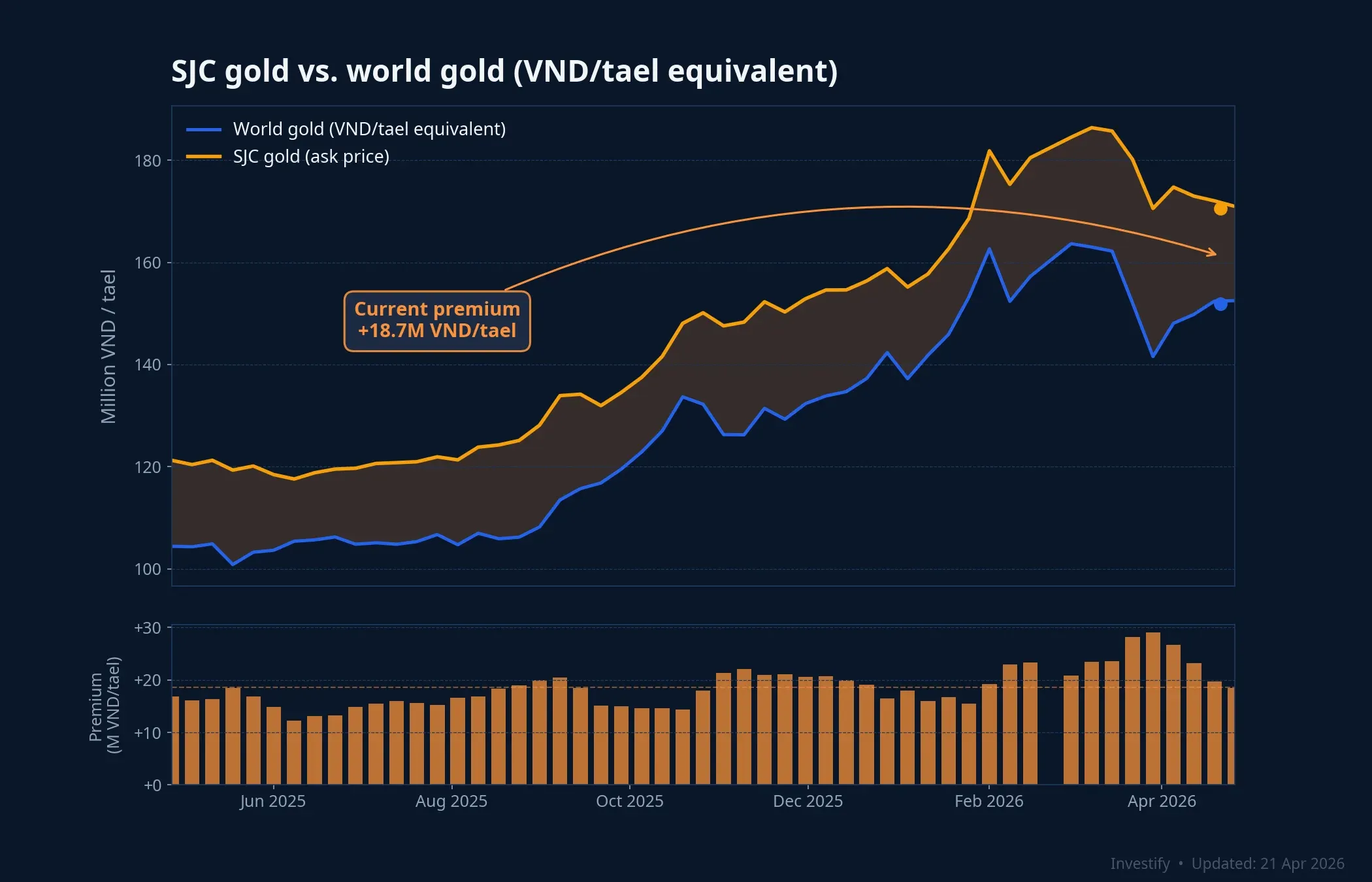

Global gold printed 4,785.63 USD/oz on 21 April. At a USD/VND rate of 26,333 and one tael equal to 37.5 grams (approximately 1.2057 troy oz), world gold translates to roughly 151.9 million VND per tael. SJC sells at 171.3 million VND — an actual premium of about 19.4 million VND per tael, close to 13%. SJC 99.99% ring gold bids at 165.8 million VND, a premium of around 13.9 million VND — lower but still substantial.

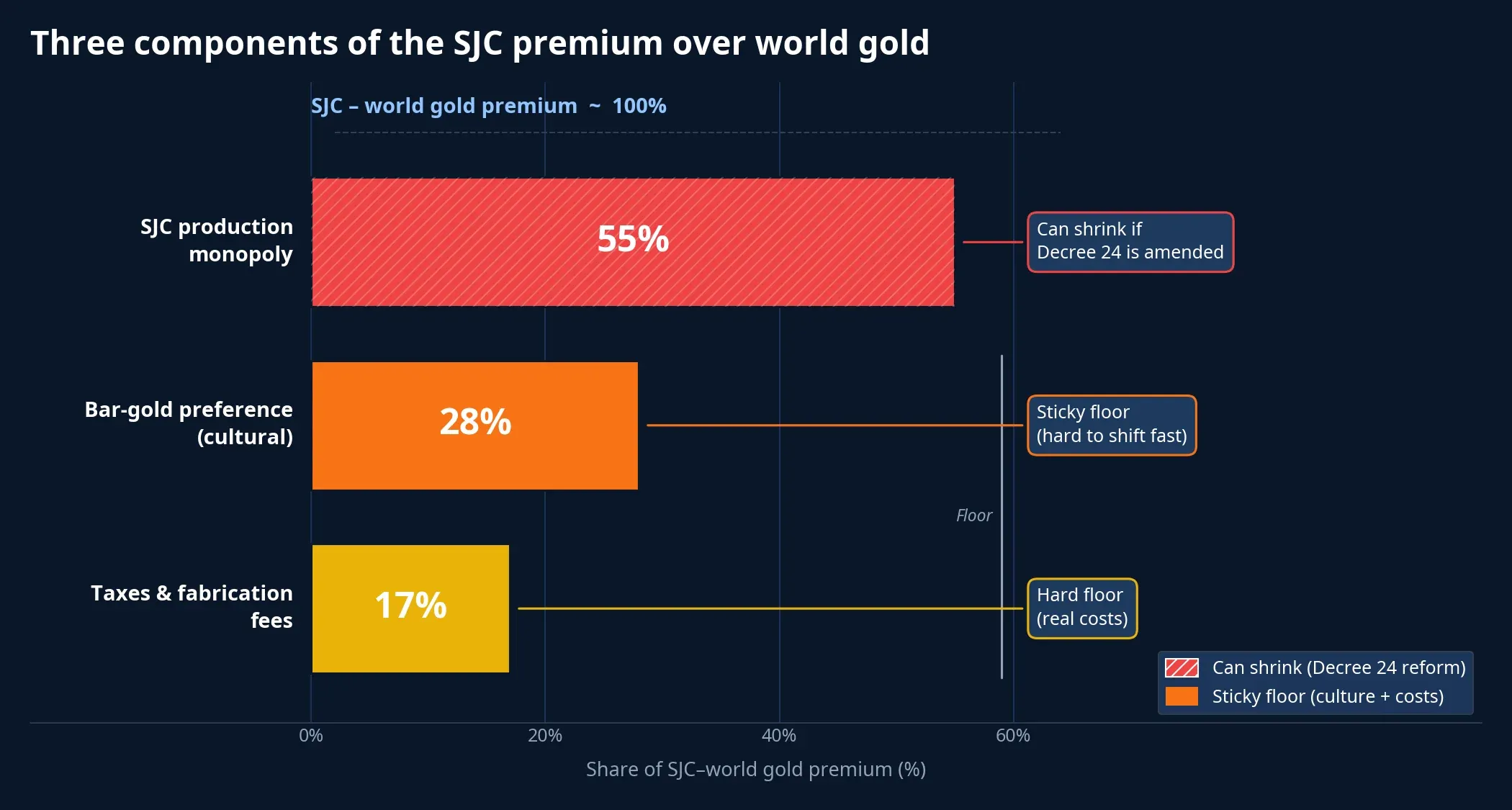

Three components drive the premium, and only one of them compresses when Decree 24 is amended:

- SJC production monopoly — direct pressure on the SJC bar price. Once the amendment takes effect and the 11 filed bar-production licences are approved, this component shrinks meaningfully.

- Cultural preference for bar gold — decades-long domestic demand, especially during macro stress. This doesn’t respond to supply policy; it only shifts if an attractive alternative (for example, state-backed gold certificates) arrives.

- Taxes, fabrication fees, compliance costs — a hard floor that cannot go to zero.

Opening imports fixes component one, does nothing for component two, and only partially addresses component three. The “premium compresses to zero” expectation doesn’t hold given these three mechanisms alone. That is why Turkey had to pair reform with a programme to move household gold into the state-insured financial system, why India paired it with SGBs, and why Thailand pairs it with central-bank-regulated certificates. Ending a monopoly alone isn’t enough — that is the shared lesson, not a Vietnam-specific twist.

Three questions retail needs to answer first, not after

The more likely scenario is that the amended Decree 24 rolls out in phases, with gold-lending and gold-certificate mechanisms following under their own legal frameworks. When the first product appears, these are three filters for separating a protected product from one that puts the risk on the person holding the gold.

1. Who issues? The state (budget absorbs price risk), a well-capitalised commercial bank, or a jewellery firm? Loss-absorption capacity differs drastically across these three. India’s model works because the RBI stands behind SGBs and treats the price differential as a policy cost. Jewellery firms don’t have that cushion.

2. Who bears the price differential on a reversal? The contract needs to spell out: if gold drops 20% mid-term, is the issuer obliged to settle in physical gold or in VND at the settlement-date price? The two options mean very different things for the certificate holder.

3. Does the legal framework set a leverage ceiling? The ratio of mobilised gold to issuer equity, limits on short-gold positions, mandatory hedging tools (such as gold futures on international exchanges). Without those three parameters, a gold certificate is effectively a civil IOU.

In the meantime, for retail investors holding bar or ring gold, the conservative framework is simple: don’t rush to expect the SJC premium to fall to zero over the next 6-12 months. Open imports and the end of the production monopoly may bring the gap down to 8-12 million per tael, but the sentiment and fabrication-cost components hold the floor. For anyone considering a gold certificate when the first product launches, the three questions above are the minimum filter before committing money.

The 2008-2012 lesson doesn’t argue for closing the door again. It argues for this: when gold comes back onto someone’s balance sheet, the risk-management framework has to be in place first, not patched on after. When the first product arrives, the three questions above are the lens — and the decision point for whether to pass.