On the morning of 21 April 2026, during the National Assembly’s economic debate session, Deputy Prime Minister Nguyen Van Thang announced a target for stock-market capitalization to reach 120% of GDP by 2028.VnExpress The number itself is not new — it already appears in Decision 1726/QD-TTg, dated 29 December 2023.Bao Chinh phu What has changed is the timing: the 120% milestone has been pulled from 2030 to 2028, two years ahead of schedule.

The reason for the acceleration does not lie in the stock market itself but in the funding balance of the broader economy. The next three years will be the window in which retail investors need to decide which instrument they will use to participate in this expansion.

Starting point: 77.9% of GDP, not a peak

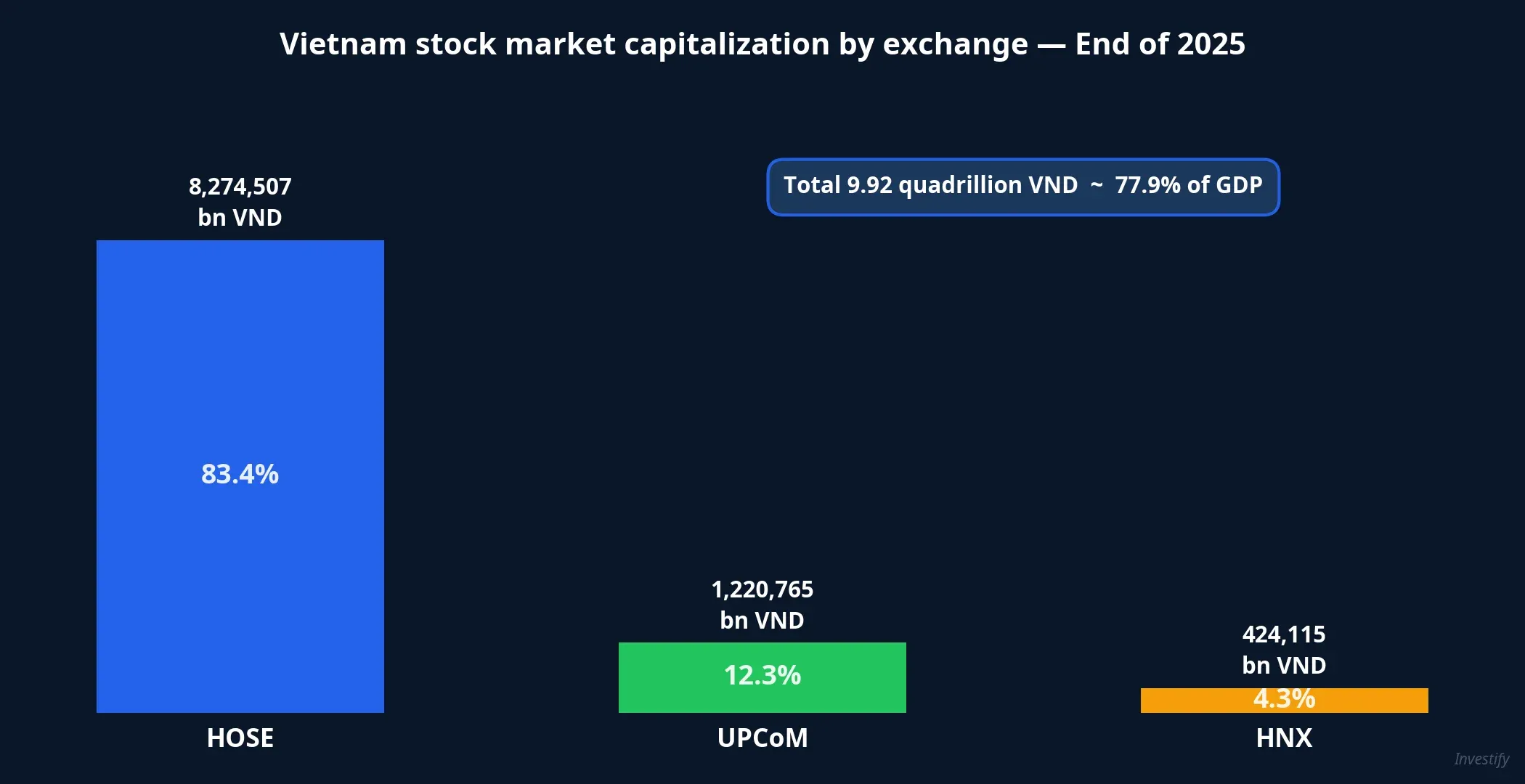

At the end of 2025, total market capitalization reached nearly 10 quadrillion VND — roughly 77.9% of GDP.VnExpress HOSE accounted for 8,274,507 billion VND, UPCoM 1,220,765 billion, and HNX 424,115 billion — HOSE alone dominates with more than 83% of the total, concentrated in VIC, VHM, VCB, CTG, and BID.

The VN-Index closed the 21 April session at 1,833.48 points, down 0.20% from the previous day. The starting point for the expansion is therefore not a peak but an accumulation zone. Moving from 77.9% to 120% of GDP in three years is a gap of 42.1 percentage points, equivalent to roughly 7 quadrillion VND of additional absolute capitalization.

Why accelerate by two years: the pressure comes from banks

The real reason behind pulling the deadline forward is not in the stock market. It is in the banking system.

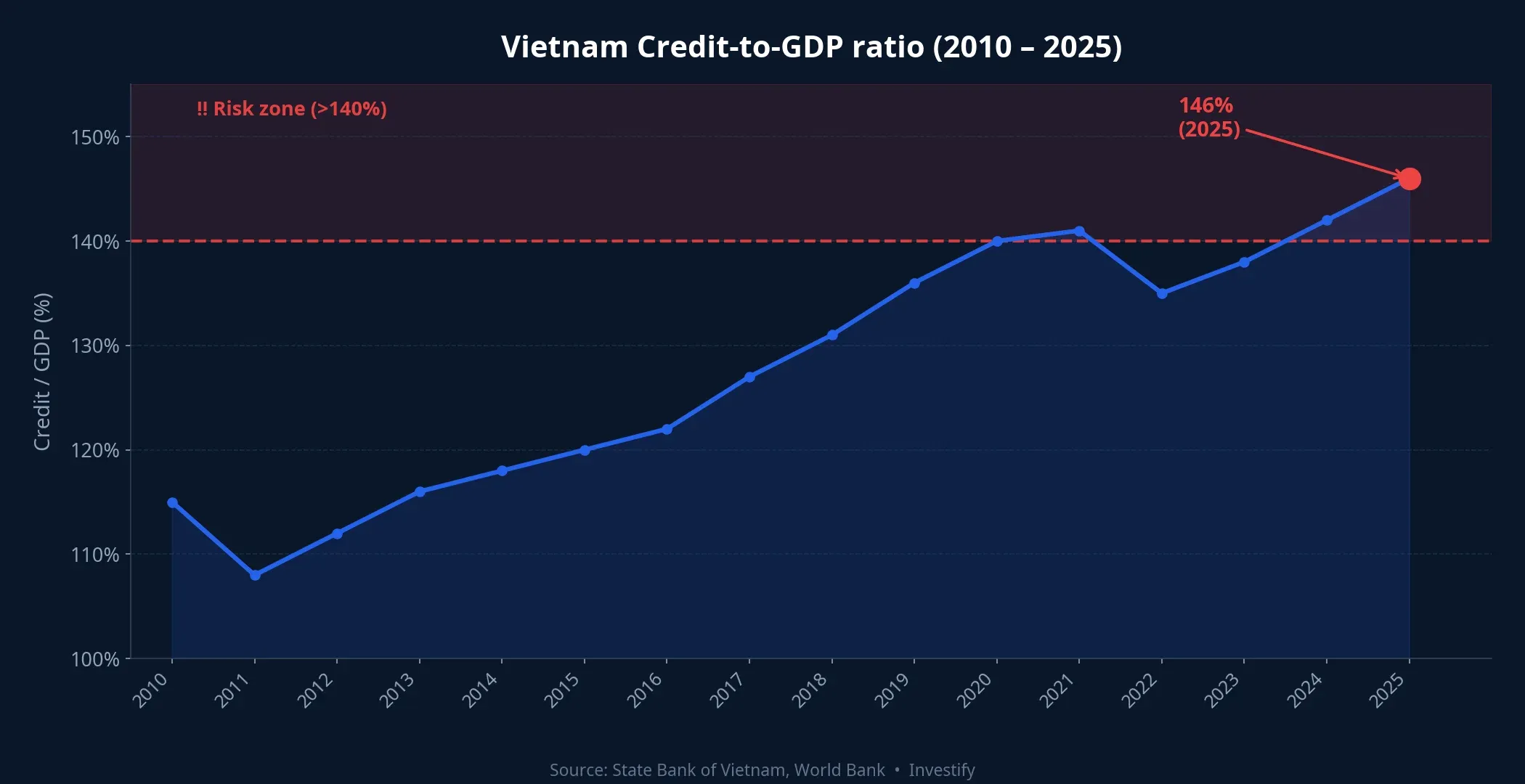

At the end of 2025, total outstanding credit in the economy exceeded 18.40 quadrillion VND, up 17.87% year-on-year. The credit-to-GDP ratio reached 146%, among the highest in the lower-middle-income country group.CafeF State Bank of Vietnam leadership has also acknowledged a maturity-mismatch risk: roughly 80% of funding is short-term, yet about 50% of loans are medium- and long-term.

Put plainly, banks are carrying a role of medium- and long-term capital provision that should have belonged to the capital market. The Deputy Prime Minister was explicit: the stock market needs to become the medium- and long-term funding channel of the economy, relieving pressure on the banking system.Thanh Nien With credit room stretched thin, the capital market has to fill the gap — and it has to do so in three years rather than five.

Where those 42 GDP points will come from

For the gap to be more than a paper figure, market size has to grow through three supplementary flows:

- Price appreciation in existing listings: driven by corporate earnings momentum and by a re-rating as Vietnam is upgraded to FTSE Emerging Markets, effective September 2026.

- New listings and state-backed IPOs: ACV is expected to list at the end of 2026; divestment candidates include GAS, PLX, BID, and CTG; larger candidates such as Viettel, VNPT, Long Chau, VNPay, and MoMo are in the pipeline. Mobile World also plans to IPO Dien May Xanh in 2026 and Bach Hoa Xanh in 2028.

- Additional issuance by existing listings: companies raising charter capital to fund medium- and long-term projects.

For retail investors, the second flow matters most. Many large IPOs will cluster in 2026–2028, creating a choice problem across a broadening opportunity set. Reading every prospectus is not practical for anyone with a day job — this is where indirect investment tools become genuinely useful.

Three channels for retail to ride the expansion

Rather than trying to pick every single name in a basket that is about to double, retail investors have three channels to position for the whole leg. The trade-off between them is not “which one gives the highest return” — it is fees, liquidity, and the amount of research time the investor has to put in.

Channel 1: Broad-index ETFs

ETFs listed on HOSE trade like ordinary stocks and track a reference index. Active domestic ETFs include:

- E1VFVN30 tracking the VN30, one of the largest ETFs on the market with average turnover of roughly 578,280 fund units per session.

- FUEVFVND tracking VN Diamond (a basket of foreign-room-capped stocks), with AUM of around 12,000–14,000 billion VND and average turnover of about 1,324,420 units per session.

- FUESSVFL tracking VN Finlead, with markedly lower turnover of around 41,603 units per session.

- FUEVN100 tracking VN100, with average turnover around 104,385 units per session.

The upside is low management fees (typically 0.6–0.8% per year, well below active mutual funds), a minimum of 100 units per lot, and intraday trading — suitable for monthly DCA. The downside: ETFs rebalance only against their index, with no alpha expectation; if the reference index has a skewed weighting (FUEVFVND tilts toward Diamond names), the held basket tilts the same way.

Channel 2: Active equity mutual funds

Mutual funds issue units daily at NAV, charging higher fees than ETFs to pay for active stock selection. A few domestic funds worth noting:

- VCBF-BCF — 1-year return approximately 40.04%, 3-year 81.02%, management fee 1.9%, minimum VND 100,000.

- VESAF — 1-year 28.00%, 3-year 65.49%, fee 1.75%, minimum VND 100,000.

- VFMVF1 (DCDS) — 1-year 39.28%, 3-year 95.81%, 5-year 75.87%, fee 1.95%, minimum VND 100,000.

The upside is the chance for alpha above the VN-Index when the manager picks well; the minimum is very low, making recurring investment accessible. The downside: fees of 1.75–1.95% per year compound meaningfully over time; NAV clears end-of-day with no intraday trading; performance varies with manager skill. Past returns do not guarantee the next leg, especially as market structure changes with the IPO flow.

Channel 3: Direct stock picks

The highest flexibility, the lowest transaction cost (0.15–0.25% per side), and no management fee. But it demands time to read financials, follow AGMs, and understand industries — the real work of a semi-professional analyst. Over a three-year expansion, the dominant risk of this channel is not a loss on names currently held but missing the new listings while focusing on a familiar narrow basket.

Combining the three channels in practice

For monthly savings (DCA), broad-index ETFs and mutual funds are the more natural channels — low minimums and no need to time entries. For a one-off lump sum, a common structure is to blend the three channels by decreasing weight according to the research time available: the less time to monitor, the higher the ETF share; the greater the conviction on specific names, the larger the direct-stock allocation.

The 120% of GDP target is a public policy commitment with a three-year horizon, not an immediate buy signal. What it changes is the time horizon of retail: if you accept that the policy will be pursued seriously, 2026–2028 will feature a dense pipeline of state IPOs and new listings, and the broadest channel is usually the best one for investors who do not want to pick names one by one.

Three signals to watch

A policy commitment is only worth as much as the milestones it is tracked against. Three factors are worth monitoring in the coming months:

- Pace of state divestments at GAS, PLX, BID, and CTG — the most concentrated supply of new stock, and a decisive driver of market-cap growth in 2026–2027.

- Timing of the ACV listing — if the end-2026 schedule holds, it will be an important test of market absorption capacity.

- Foreign flows after the FTSE upgrade takes effect in September 2026 — passive flows from emerging-market index funds are a meaningful component of the 42 GDP-point expansion.

These three signals will reveal whether policy is converting into actual supply and demand flows, or whether it remains a statement. Retail does not need to predict the outcome — only to observe and rebalance the three channels as progress unfolds.