On the morning of April 22, 2026, at Vinamilk’s Annual General Meeting, a retail shareholder stood up to complain: he had held VNM for ten years and still had nothing to show for it. Mai Kiều Liên — Vinamilk’s long-serving CEO — answered bluntly: “Honestly, I never pay attention to the share price”, adding that the price is set by supply and demand, by earnings, and by growth prospects, and the company cannot direct it.Tuổi Trẻ

That complaint was not just one person’s. Behind it sits an expectation that has simmered for years across thousands of retail accounts that once treated VNM as a “national blue-chip”: hold a defensive sector leader, and profit will come. That belief may have been wrong from the outset — not because VNM has deteriorated, but because the stock has quietly changed roles.

Flat on price, not flat on return

VNM closed on April 22 at VND 61,800 per share. Compared with the VND 140,000–150,000 range in early 2016, before the subsequent stock splits and bonus issues, the position has indeed gone nowhere on price once adjustments are applied. But across those same ten years, Vinamilk has paid out roughly VND 44,500 in cash dividends per share. A long-term holder has already received back nearly two-thirds of today’s share price in cash — not break-even in the strict sense, only no capital gain on top of that.

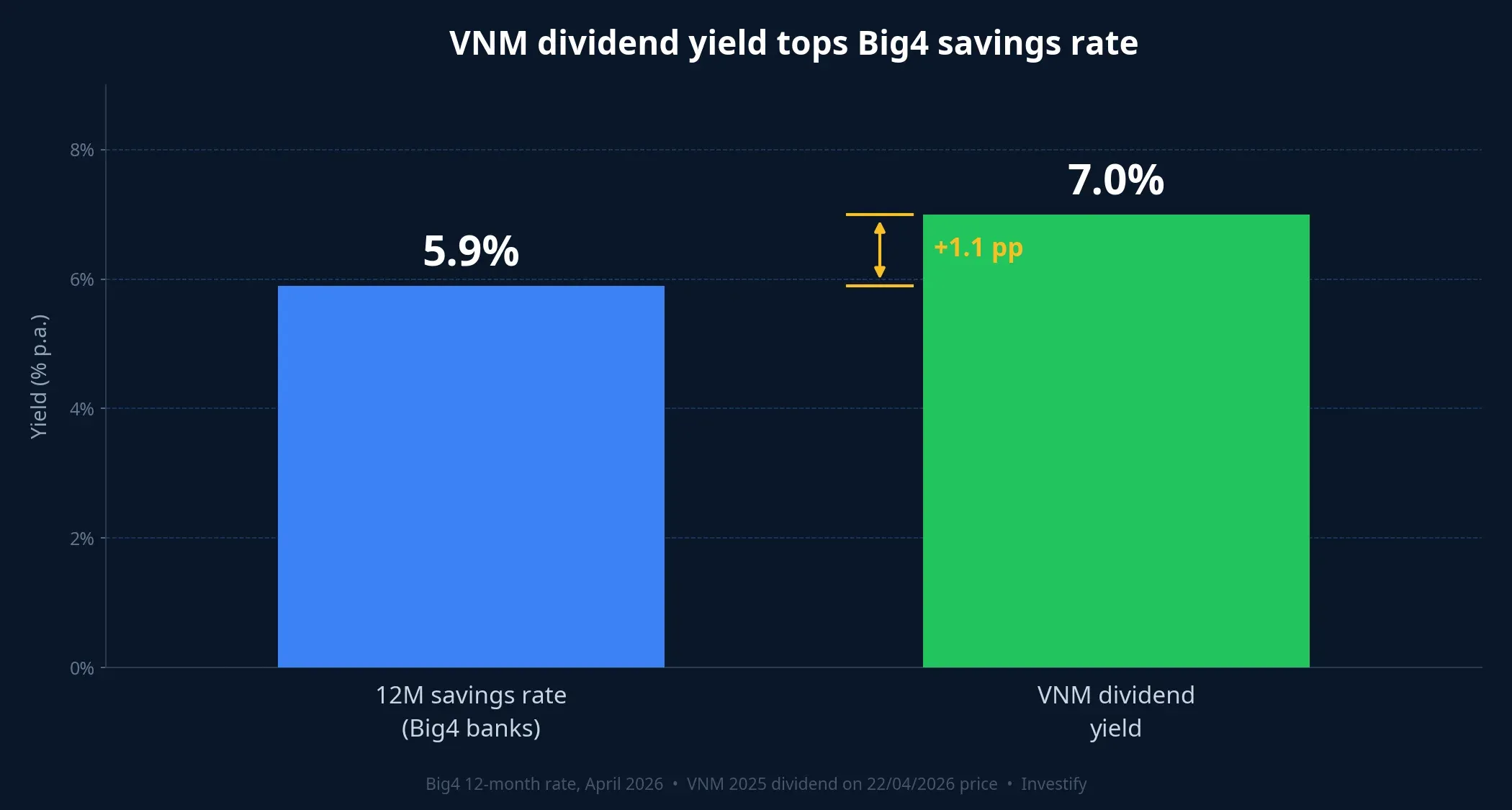

This is the first distinction worth naming: the shareholder said “flat” because he measured in price, while Vinamilk has been returning most of its profit as cash dividends. The 12-month Big4 savings rate in April 2026 is 5.9% per year.VietnamBiz If the annual dividend cash flow is compared with a rolling 12-month deposit over the same decade, VNM does not clearly beat savings — that is the real issue. But “flat at zero” is the wrong ruler.

Why VNM is flat: a saturated domestic category

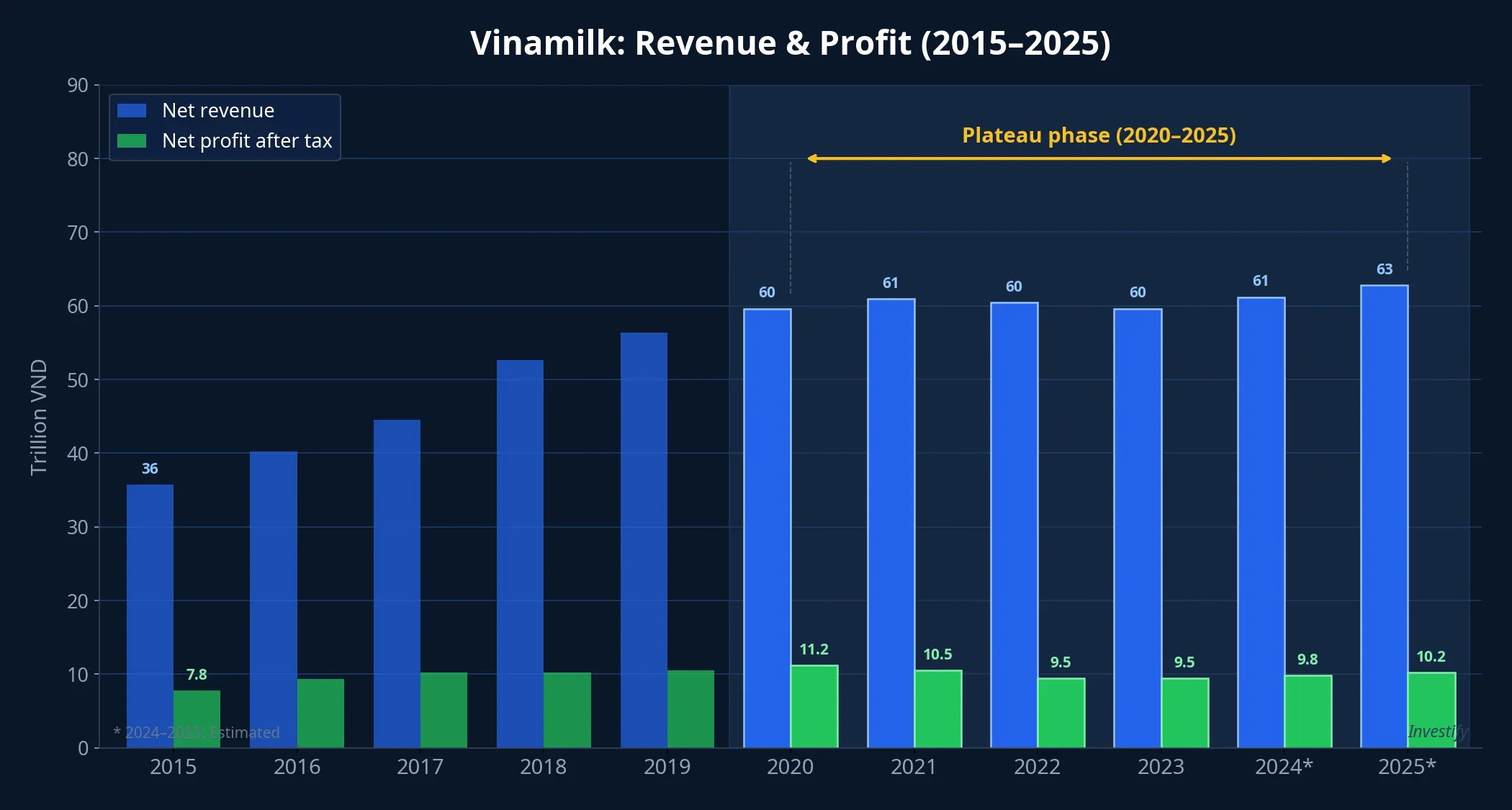

The next question is why the price has not risen. Ten years of financials give a compact answer: revenue and profit have been broadly flat since 2020. Consolidated revenue moved from VND 59,636 billion in 2020 to VND 63,646 billion in 2025 — only 6.7% over five years. Net profit in the same window has hovered around VND 9,400–11,200 billion, closing 2025 at VND 9,414 billion, below the 2020 peak. A sector leader holding roughly 43% of the domestic dairy market in 2024 per FPTS estimates still runs well and earns a lot, but it no longer grows at the 2015–2018 pace.

The underlying reason: Vietnam’s dairy category has hit a domestic ceiling. Per-capita dairy consumption is about 27 liters per year — below regional peers, with long-run headroom, but the growth rate has slowed as the demographic profile matures, as TH True Milk and Nutifood compete, and as consumers shift to other nutritional beverages. Vinamilk has not lost share — it even recovered slightly in 2024 — but the pie simply is not expanding fast enough to lift earnings.

When earnings plateau, there is no reason for the P/E multiple to expand, and the share price naturally flattens with it. This is not a broken company, it is the profile of a mature sector leader. Holding VNM today is closer to holding a bond with a high coupon than holding a growth lottery ticket.

The role has changed: from capital gains to dividend income

For a business in this state, the return mechanism for shareholders is no longer price appreciation — it is the cash dividend. The April 22 AGM approved the 2026 plan: consolidated revenue of VND 66,477 billion and net profit of VND 9,828 billion (both up roughly 4% year on year), with a dividend policy committing to at least 50% of 2026 profit paid in cash.DNSE The 2025 dividend was fixed at 43.5% of par, or VND 4,350 per share.

Applied to today’s price of VND 61,800, that dividend translates to a yield of about 7.0% on the current cost. That is about 1.1 percentage points above the 12-month Big4 deposit rate of 5.9%. This is the return a VNM shareholder today can reasonably expect — not a doubling of the share price over three years like the 2016 era.

The correct frame for VNM today is a dividend channel: buy for the steady cash flow, and accept that the share price may continue to drift sideways for years. The wrong frame is the capital-gains channel: buy and wait for the price to double in three to five years. The shareholder who complained on April 22 measured VNM by the second frame, in a company that switched to the first frame long ago. One caveat is worth stating plainly: a 1.1 percentage-point premium over a state-backed bank deposit is not a lavish risk reward — it supports holding VNM in the defensive sleeve of a portfolio, not overweighting it.

A self-check for defensive sector leaders

The VNM story is not unique. HOSE lists several other sector leaders once treated as “national” names by retail investors. FPT closed April 22 at VND 74,600, about 43% below its peak of VND 131,668 on January 23, 2025; earnings are still rising, but the P/E multiple has compressed sharply after an expensive run. SAB sits at VND 45,050 on a P/E of about 13.2 and ROE close to 20% — a dominant domestic brewer with healthy returns, but revenue has been nearly flat for years. MWG at VND 86,200 with a P/E near 18.4 has moved past its store-rollout boom and into a maturity narrative. VJC at VND 176,200 trades on a P/E close to 58 with ROE of only 8.6% — still priced for a growth story its returns do not support.

A simple self-check for anyone holding a defensive sector leader today:

- Look at revenue and profit growth over the past three to five years. Two consecutive flat years is a signal the domestic category may have hit its ceiling.

- Look at market share. A stable position near the top means little domestic headroom; further growth will depend on exports or new product lines.

- Look at the dividend yield on today’s price. If it already sits meaningfully above the 12-month Big4 deposit rate, the market is pricing the stock on a dividend frame, not a growth frame.

With the VN-Index closing April 22 at 1,857.30 and breadth negative (113 advancers versus 205 decliners), the reasonable default for a saturated sector leader is to treat it as a steady dividend stream, not a bet on capital appreciation. Whether to hold or trim depends on position size and cash-flow needs, but the expectation has to be reset before any decision means anything.

A complaint is really a call to reread the frame

The thesis, stated cleanly: VNM today is no longer a capital-gains stock, it is a dividend stock. At VND 61,800, the dividend yield of about 7.0% beats the 12-month Big4 deposit rate by 1.1 percentage points — enough to justify a slot in the defensive sleeve, not enough to justify expecting capital gains. Three factors could reverse this picture and deserve monitoring: the new Mộc Châu Creamery project that management expects to contribute about half of revenue over the medium term, the pace of export expansion into the Middle East and ASEAN, and competitive intensity at home from TH True Milk and Nutifood. If all three improve and revenue breaks out of the plateau, the growth frame could return. Until that evidence arrives, the dividend frame is the reasonable default.

The complaint “ten years, flat” sounds like an investment failure. In practice, it is a call to reread the frame. For many retail investors still holding “national” blue-chips in their portfolios, that call is worth answering before the complaint.