Two days before Sacombank’s shareholders gathered in Việt Trì on the morning of April 22, the board unexpectedly withdrew Proposal No. 25/2026/TT-HĐQT, the same proposal to extend the post-merger restructuring program through 2030 that the board itself had issued five weeks earlier on March 18, 2026.CafeF The bank has not disclosed a reason, but this is not a procedural adjustment. It is a signal about when Sacombank intends to close the 10-year journey it has walked since the SouthernBank merger in 2015.

The market voted twice

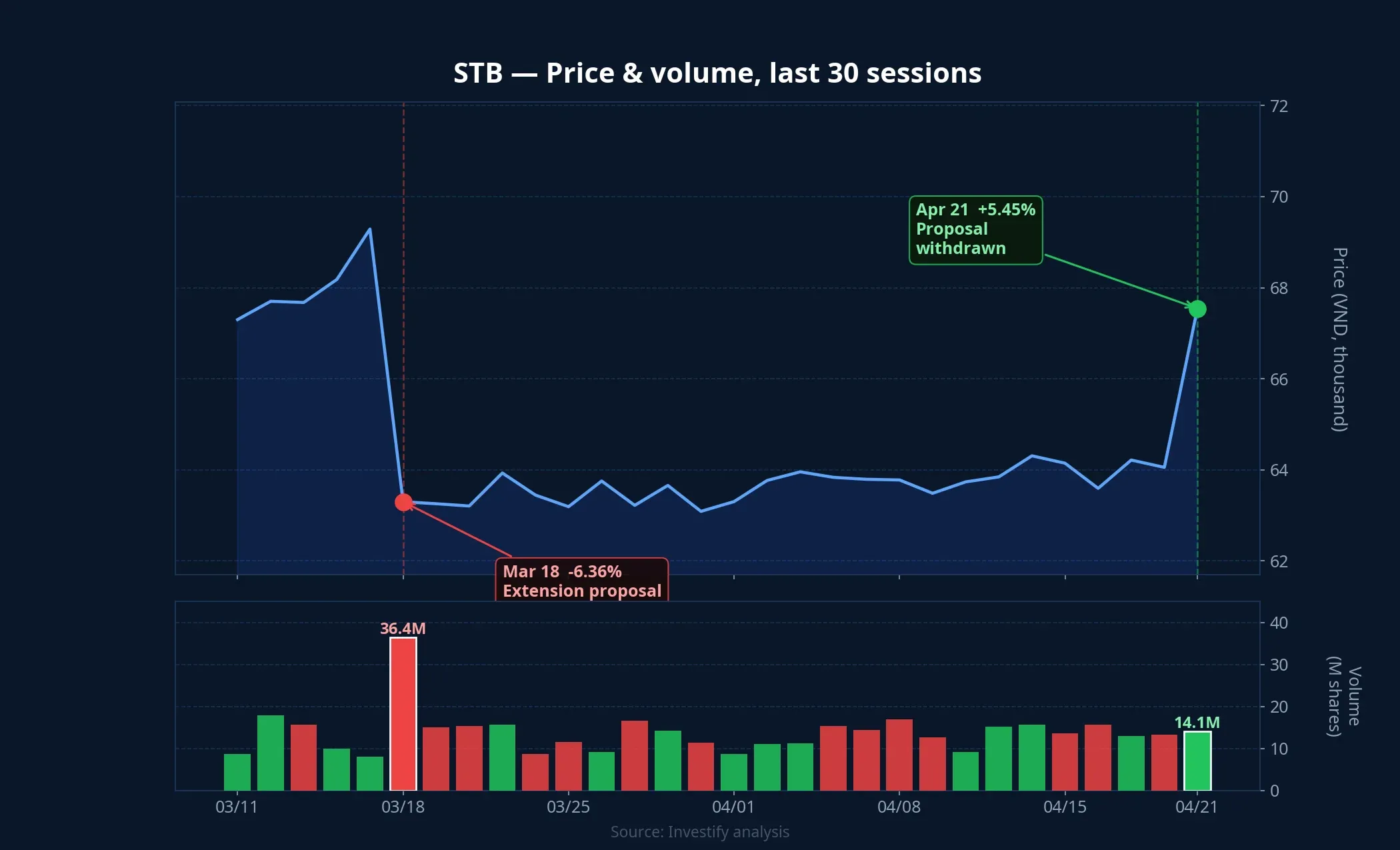

When the extension proposal was announced on March 18, STB fell 6.36% to VND 63,300 on unusually heavy turnover of 36.4 million shares, three to four times the typical session.Vietstock Shareholders were not enthusiastic about the prospect of another four years under the restructuring regime.

By April 21, after news of the withdrawal broke on the afternoon of April 20, STB closed at VND 67,700. That price recovered the entire earlier decline on volume of 14.1 million shares, and market capitalization returned to VND 127.6 trillion. Two opposing decisions from the board, two opposing market reactions, and only five weeks between them.

The important point: withdrawing the proposal does not automatically mean the program will close in 2026. It opens three possibilities, each with a different exit path for STB. The numbers can frame each scenario, but most of the answer will only become clear in the next six months.

Scenario A: Completion on schedule in 2026

This is the scenario the market priced in during the April 21 rally.

The foundation for this scenario is what Sacombank has already done: full provisioning of VAMC bonds, broad cleanup of legacy items in 2023–2025, and the successful auction of the Phong Phú Industrial Park. Based on market analysis, an estimated VND 12,000 billion in collateral recovery is expected to be recognized in 2026, enough to close most of the remaining provisions.

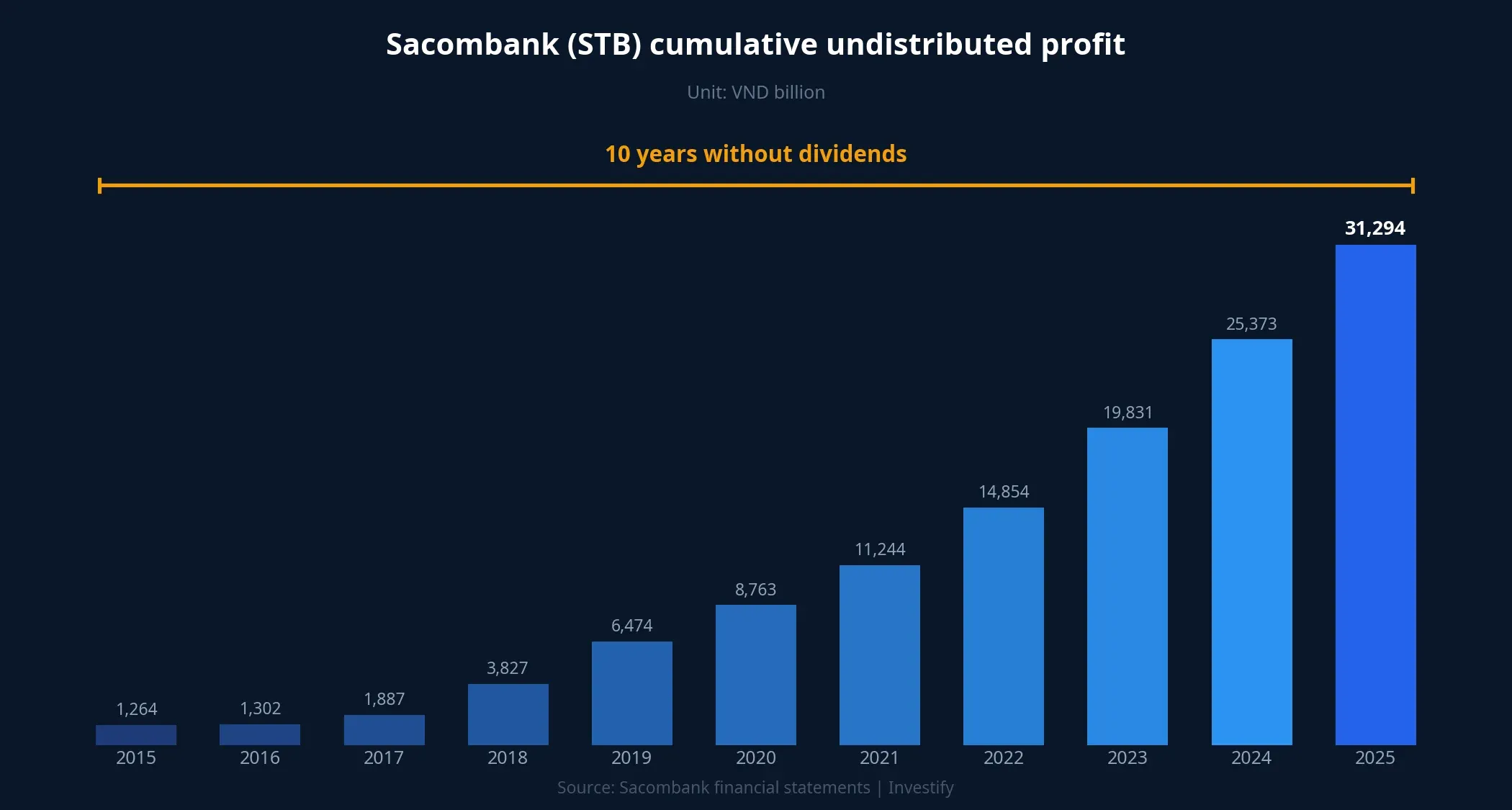

If the State Bank of Vietnam permits Sacombank to end the program, the undistributed earnings accumulated over 10 years without dividends will enter a workable zone. That figure had reached approximately VND 31,294 billion at the end of 2025 according to financial statements, close to the bank’s current charter capital.

Three patterns are common at banks emerging from supervision: cash dividends, stock dividends to raise charter capital, or allocation to share premium and reserves to strengthen capital adequacy. ACB, after exiting its own restructuring, chose the third option first, then returned to a regular dividend policy. Its P/B then drifted from a discount to a higher band as the market confirmed that legacy issues had been resolved.

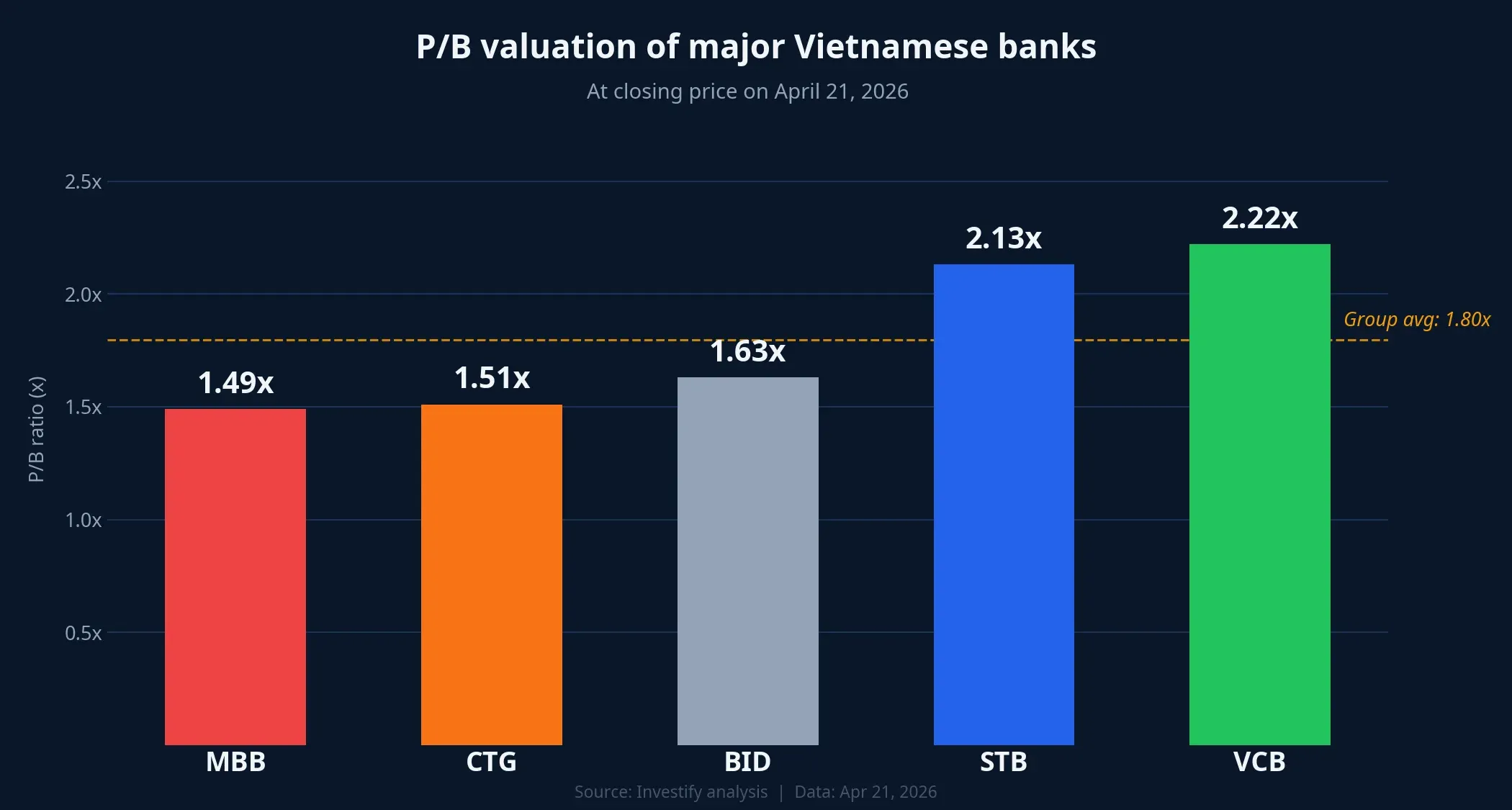

At the price of VND 67,700, STB’s P/B sits at roughly 2.13x (BVPS VND 31,756), above the state-owned group ex-VCB and slightly below VCB.

In this scenario, the re-rating headroom is not about STB overtaking VCB. It is about the market reclassifying STB from a bank “still restructuring” to a bank “having completed restructuring.” A small P/B premium, but a fundamentally different risk profile.

Triggers for Scenario A: an official SBV decision to close the program, a concrete board proposal on profit distribution within the next six months, and clear recognition of the VND 12,000 billion recovery in the H1 2026 report.

Scenario B: De facto extension into 2027–2028

The extension proposal that Chairman Dương Công Minh submitted on March 18 was not random. The legacy items linked to the Trầm Bê group, including the 32.5% stake originating from that group, are the slowest part of the program and depend on legal proceedings rather than the bank’s internal cleanup pace.

Withdrawing the proposal does not necessarily mean the cleanup is finished. The bank may simply choose not to formally extend the program and let the cleanup run into 2027–2028 in practice, avoiding the media weight of a “four more years” message. This pattern has occurred in other restructuring programs: the date of paperwork closure and the date when legacy items truly clear can be a couple of years apart.

In this case, Sacombank’s NIM will face prolonged pressure from cleanup costs and additional provisions tied to the pace of litigation. The 2026 pre-tax profit target of VND 8,100 billion (+6.2% year-on-year), 45% below the previous year’s VND 14,650 billion plan, partly implies that management is already cautious about this possibility.

Triggers for Scenario B: the quarterly pace of collateral recovery in 2026, developments in legal cases related to the Trầm Bê stake, and the gap between provisioning plans and what is actually booked.

Scenario C: Reinvention, not just restructuring

The third scenario reads the Sacombank story at a different scale. The withdrawal of the extension proposal, the arrival of Mr. Nguyễn Đức Thụy as CEO since March 2026 with an expected board appointment at today’s AGM, and the upcoming shareholder vote on a brand identity change: this sequence is unlikely to be a string of unrelated adjustments.

They may signal that Sacombank is preparing to shift from a bank “closing out a merger legacy” to a bank “opening a new ecosystem.” The decision to hold the AGM in Phú Thọ rather than the Ho Chi Minh City headquarters for the first time in two decades is not symbolically neutral either.

In this scenario, the planned milestone of crossing VND 1,000 trillion in total assets in 2026 is not just a size marker but a gateway into the “trillion-dong bank” group. Valuation then depends not only on asset quality but also on strategic partnerships, M&A announcements, or product expansions that the new board may unveil after the AGM.

To be clear: this is also the scenario with the highest governance risk. Allocating retained earnings toward expansion rather than distribution to shareholders is a choice that retail investors must monitor closely, particularly when the major-shareholder structure is not yet fully settled.

Triggers for Scenario C: the AGM vote on the brand identity change, M&A or strategic partnership announcements within six months, and major-shareholder composition in the next disclosure cycle.

Three documents to scrutinize after the AGM

The 2022–2026 board term has only a few effective months left, a short window for action. Three documents worth watching after the AGM:

- The resolution on accumulated profit distribution: signals which scenario Sacombank is leaning toward.

- Official statements on the Trầm Bê legacy cleanup pace: signals the gap between Scenarios A and B.

- The vote on the brand identity change: signals the level of commitment to Scenario C.

STB has risen roughly 10.6% in just the last two sessions (April 17 close 64,000 → April 21 close 67,700). Part of Scenario A is already in the price, but the spread between the three scenarios remains wide and will only narrow as the specific signals above arrive. Without enough data to commit to a single direction, watching the right signals is a more reasonable choice than guessing the scenario in advance.