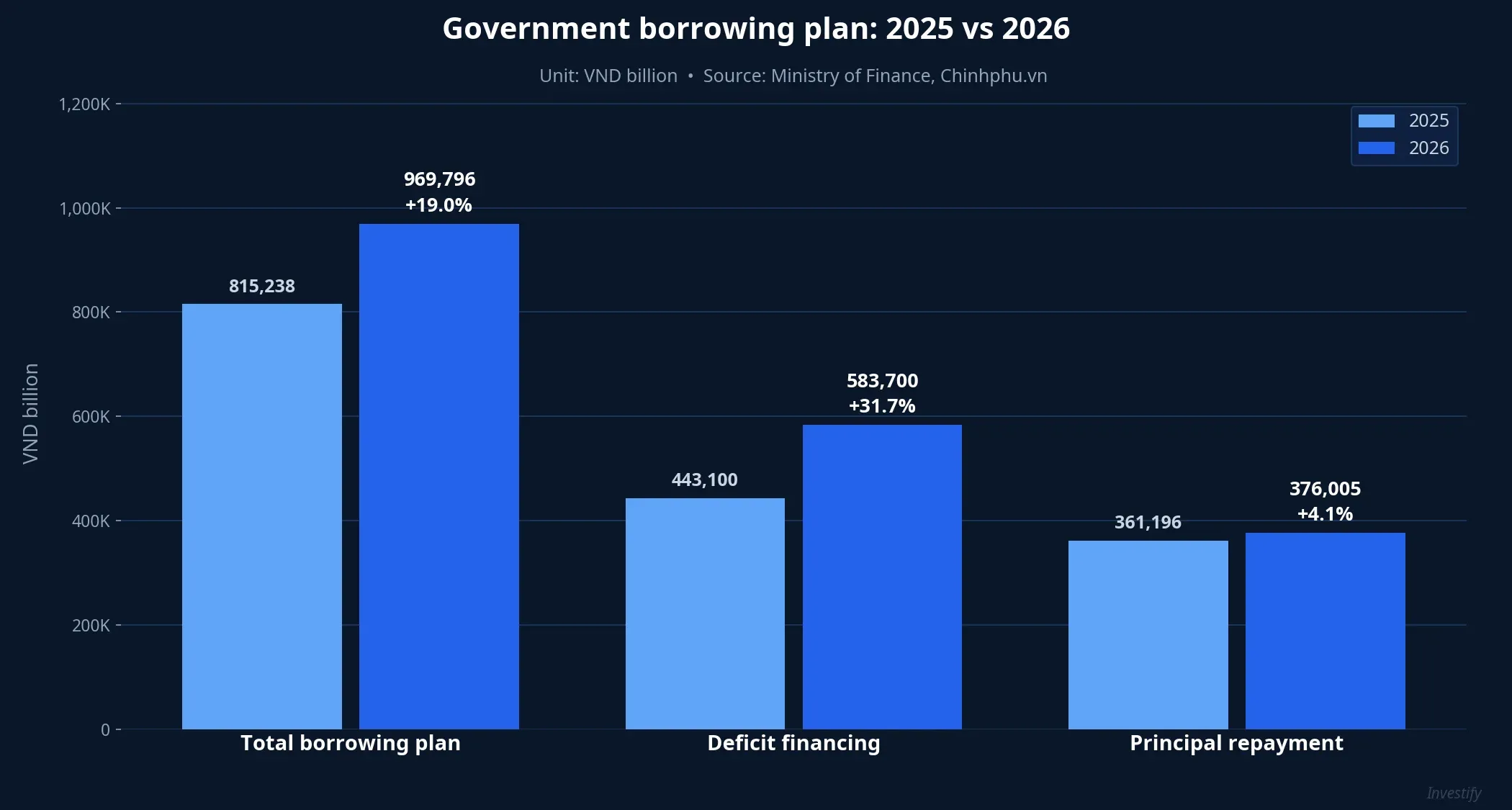

Vietnam’s government has just finalized a 2026 borrowing plan of up to VND 969,796 billion, VND 154,558 billion more than the VND 815,238 billion approved for 2025.Thoi bao Tai chinh The total is up roughly 19%, but the more telling figure sits deeper in the structure. Borrowing to cover the central budget deficit jumps to VND 583,700 billion, up 31.7% from VND 443,100 billion a year earlier, while borrowing to roll over principal rises only 4.1% to VND 376,005 billion. On-lending adds another VND 10,092 billion.

The gap between those two components says a lot about the nature of this year’s funding need: the incremental borrowing is pouring into development investment, not into servicing old debt. Refinancing pressure isn’t much heavier than last year. What’s actually expanding is fresh demand for capital for the economy. And the three mechanisms that follow are pulling VND rates to a new baseline, different from the expectations of the previous cycle.

Mechanism one: a VND 534,739bn repayment schedule competing directly with new bond supply

Alongside the new borrowing, the government also has to repay roughly VND 534,739 billion in 2026, split between VND 493,405 billion in direct debt service and VND 41,334 billion in on-lent project repayments.Chinhphu Placed next to a VND 970tn new-issuance plan, the treasury’s cash-flow picture this year is tight: a heavy maturity schedule forces the State Treasury to maintain a steady auction cadence both to refinance maturing debt and to raise the new capital needed to finance the deficit.

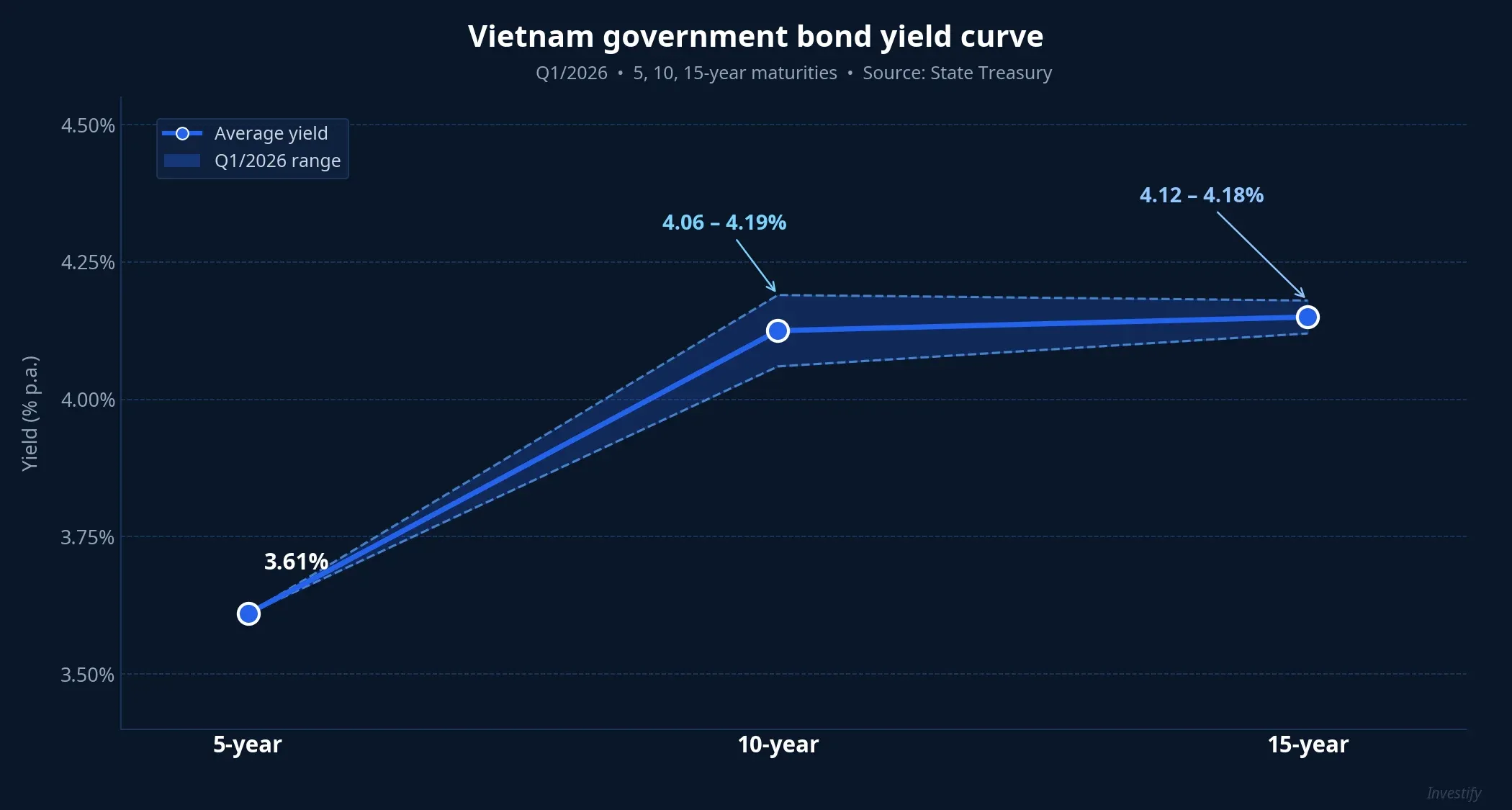

The funding mix blends domestic government bonds (VGBs), ODA, concessional foreign loans, and possible international bond issuance. Domestic VGBs remain the dominant channel. Q1/2026 raised VND 80,101 billion at an average yield of 4.06% per annum, about 0.8 percentage points higher than the same period in 2025.VnEconomy Ten-year paper cleared at 4.09–4.19% depending on the session, 15-year around 4.12–4.18%, and 5-year traded on the secondary market near 3.61%.

The yield curve is steepening clearly in the belly and the long end, a market acknowledgment that 2026 funding demand isn’t easing. With VND 534,739 billion in repayments this same year, any softening in bond demand forces the Treasury to lift auction yields to pull in enough volume. A drop back to 3.2–3.5% yields, the norm before 2025, looks unlikely in the near term.

Mechanism two: USD 5.5bn in foreign borrowing meets a weak DXY, but the rate gap hasn’t closed

The foreign-currency portion of government borrowing in 2026 is projected at roughly USD 5.5 billion, which works out to about 15% of the total plan at current exchange rates.Tien Phong This is the second layer of pressure retail investors need to track, because it flows straight into USD/VND, which in turn sets the real purchasing power of the VND portion of a portfolio.

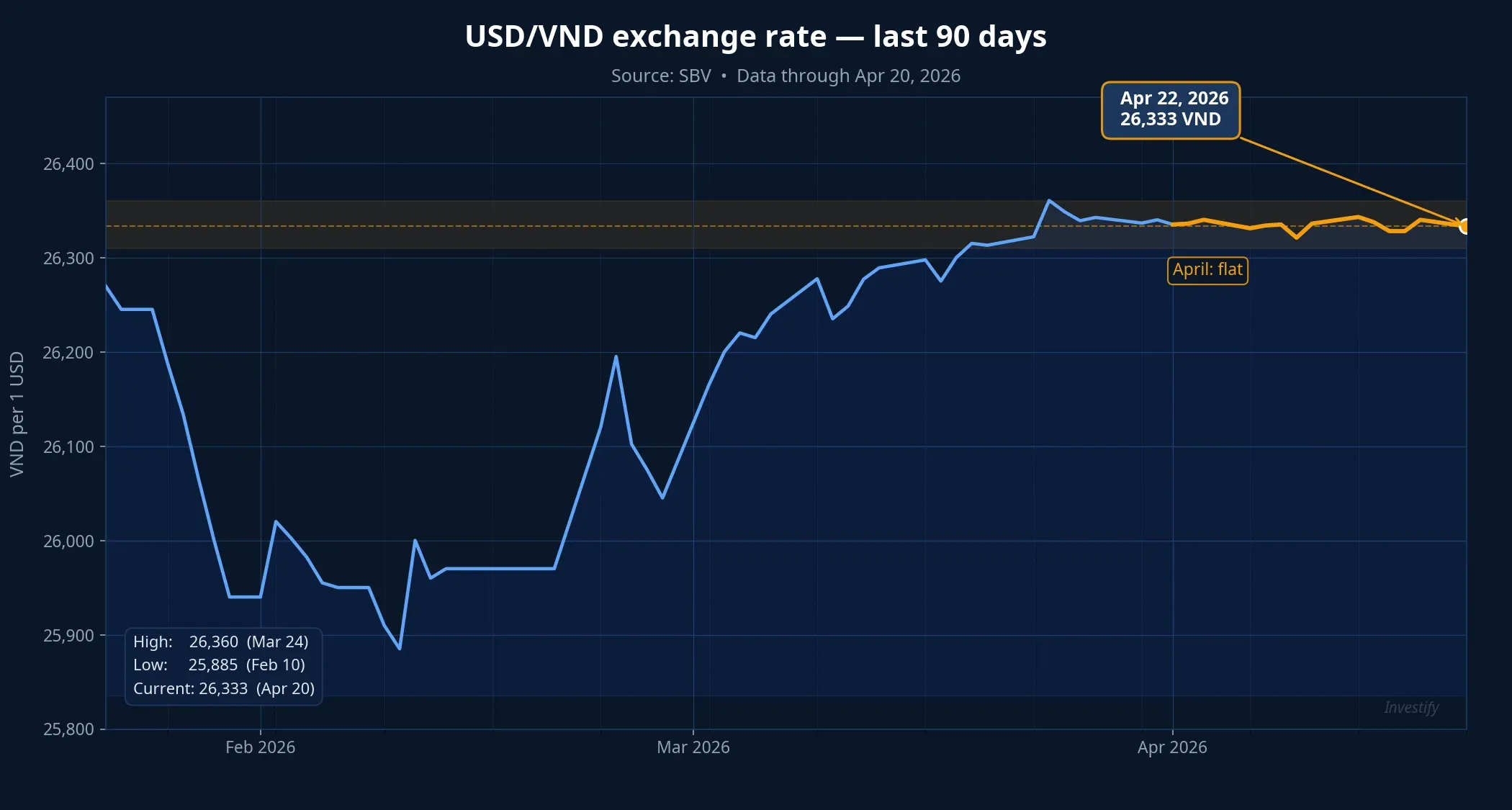

USD/VND sat around 26,333 on April 22, 2026, essentially flat over the past 30 days, even though the DXY, measuring USD strength against major currencies, has slipped about 1.6% over the month to 98.10. The “USD weaker globally, VND not stronger locally” pattern reflects a USD–VND rate differential that hasn’t meaningfully narrowed: the State Bank of Vietnam’s policy rate has held at 4.5% since March 1, 2026, while the Fed has yet to pivot decisively into easing.

When the government steps into the FX loan market at USD 5.5 billion scale, domestic USD demand rises at the absorption window. Combined with rising domestic inflation (March CPI reached 4.65%), the room for the VND to appreciate alongside a weaker USD is materially compressed.VnEconomy

The highest-probability scenario for the next few months: USD/VND stays in a narrow 26,200–26,500 band, rather than a sharp decline, until either the rate gap narrows or the Fed cuts another 50 basis points. That has direct implications for holding VND versus allocating into USD: expecting a deeper move back toward 25,500–25,800 requires a catalyst that hasn’t yet materialized.

Mechanism three: 15% credit growth meets slow deposits, leaving deposit rates sticky

The State Bank of Vietnam is targeting credit growth of about 15% in 2026, built on top of last year’s strong expansion. Deposit growth, however, is running noticeably slower this year: Q1/2026 credit grew 3.3% while deposits rose only 0.73%. The widening gap between the two ends (loans expanding faster than deposits can come in) will, if sustained, create persistent liquidity pressure across commercial banks.

When the Treasury is issuing bonds at 4.06% or higher, banks competing for the same long-duration funding pool are forced to hold, or raise, savings rates to attract 12-month deposits. Current 12-month savings rates sit around 5–5.5% per annum at the Big 4, 6.5–7% at mid-sized private banks, and 7–8% at smaller lenders.

FiinRatings expects deposit rates to rise another 0.5–1 percentage point over the remainder of 2026.Thoi bao Tai chinh In other words, the expectation of “savings rates drifting back to 4–4.5%”, common during the 2023–2024 easing cycle, no longer fits this year’s funding-demand structure.

Three mechanisms act together, not in isolation

The broader picture shows these three mechanisms are not moving in isolation. The VND 534,739bn repayment schedule keeps the Treasury issuing at a steady cadence, the USD 5.5bn foreign loan compresses VND appreciation headroom, and 15% credit demand keeps deposit rates sticky. Stacked together, VND rates across both deposit and sovereign-bond channels trend sideways or drift higher through the remaining nine months of 2026, not lower.

Retail investors can read these signals across three allocation frames. Note that this is an analytical framework, not specific buy/sell advice.

On bank savings, the current rate structure (Big 4 at 5–5.5% and small banks up to 8%) remains the standard fixed-rate channel for the cash sleeve of a portfolio. If the SBV is not expected to cut its policy rate in 2026, locking in a long tenor at current levels isn’t urgent, but waiting for a “peak” also doesn’t make sense if the spread between 12-month and 24-month rates is small enough (typically under 0.3 percentage points).

On government bonds, the 4.06% Q1 average and 4.1–4.2% at the 10-year are converging on the 12-month deposit rates offered by mid-tier private banks. With the spread between the two channels largely closed, VGBs lose their relative advantage for short-horizon fixed income. For 15–30-year tenors, however, they remain one of the few true long-duration anchors for the stable portion of a portfolio, particularly with inflation expectations already at 4.65%.

On holding VND versus USD exposure, a USD/VND that’s expected to hold within 26,200–26,500 in the short term argues that foreign-currency holdings should play a balancing hedge role, not a yield role. A 5–10% portfolio allocation is the common hedge benchmark for retail investors without USD liabilities. Rushing into USD after the DXY has already fallen 1.6% in a month while the VND hasn’t shown a convincing drop runs against current pricing.

Signals to watch over the next two months

The core message of the VND 970tn borrowing plan isn’t some abstract fiscal number. It sets the frame for bond supply, deposit-rate pressure, and the FX band that retail investors will face every month for the rest of the year. Three indicators belong on the monitoring desk:

- 10-year VGB auction yield: currently 4.09–4.19%. A clean break above 4.3% would signal bond demand is falling short and system-wide rates will follow higher.

- USD/VND: the hinge level is 26,500. A break above suggests domestic USD liquidity is being absorbed faster than expected.

- Credit–deposit gap: if Q2 deposit growth stays below 1.5% while credit climbs past 5%, long-tenor savings rates will have to move up to close the gap.

Reading these three mechanisms correctly means personal allocation will track the real pricing of capital in 2026, rather than expectations anchored to an easing cycle that has already passed.