On the morning of April 22, 2026, Vingroup’s annual shareholder meeting approved the year’s plan: revenue of VND 485 trillion (up 46% versus 2025) and net profit of VND 35 trillion — approximately three times the 2025 result.CafeF The entire profit will be retained, with no dividend, to fund ongoing business activity.Vietstock

The VND 35 trillion figure is easy to read. Placed next to the 2025 consolidated base of roughly VND 11,065 billion, next to the VND 60 trillion target at the Vinhomes subsidiary level, and next to the fact that Vingroup just lifted the plan by an additional VND 10 trillion only two days before the meeting, three mechanisms behind the “3x” number stand out fairly clearly. This post unpacks each mechanism, flags the assumption worth testing in each, and answers the question of why a P/B near 10x is not simply inflated expectation.

Mechanism 1: Vinhomes remains the anchor, but VND 60 trillion does not flow entirely into VND 35 trillion

One day before the Vingroup meeting, Vinhomes shareholders approved the 2026 target: revenue of VND 285 trillion and net profit of VND 60 trillion.VietnamNet This is an upward revision from the previously disclosed VND 50 trillion plan. The 2025 baseline at Vinhomes was revenue of VND 153,271 billion (up 49.8% year-on-year) and net profit of VND 43,335 billion (up 23.6%).

At first glance, Vinhomes’ VND 60 trillion net profit already exceeds the VND 35 trillion consolidated target of the parent. The natural question: how can the subsidiary earn more than the parent? This is where consolidation accounting tends to trip up retail investors. Vingroup’s consolidated statements include 100% of Vinhomes’ revenue and profit, but then subtract the minority interest share — the portion attributable to minority shareholders of Vinhomes — from the net profit attributable to the parent. Vingroup retains controlling influence over Vinhomes but does not own 100%.

The consequence: VND 60 trillion in Vinhomes net profit flows into Vingroup’s consolidated statements, then a meaningful slice flows out as minority interest. The remainder, combined with the results of VinFast, Vinpearl and group-level costs, arrives at the VND 35 trillion consolidated target. A parent target below a subsidiary target is not a paradox — it is standard consolidation arithmetic.

The assumption to test. Vinhomes earned VND 43,335 billion in 2025. Reaching VND 60 trillion in 2026 implies a 38% increase. The harder part sits on the revenue line: Vinhomes is targeting VND 285 trillion, up 86% on the 2025 base.Nguoi Dua Tin That jump depends directly on mega-project launches and handovers landing on schedule in 2026. Slippage at a single flagship project can skew the entire segment, so investors watching VIC or VHM should track quarterly handover progress rather than just unit sales at launch.

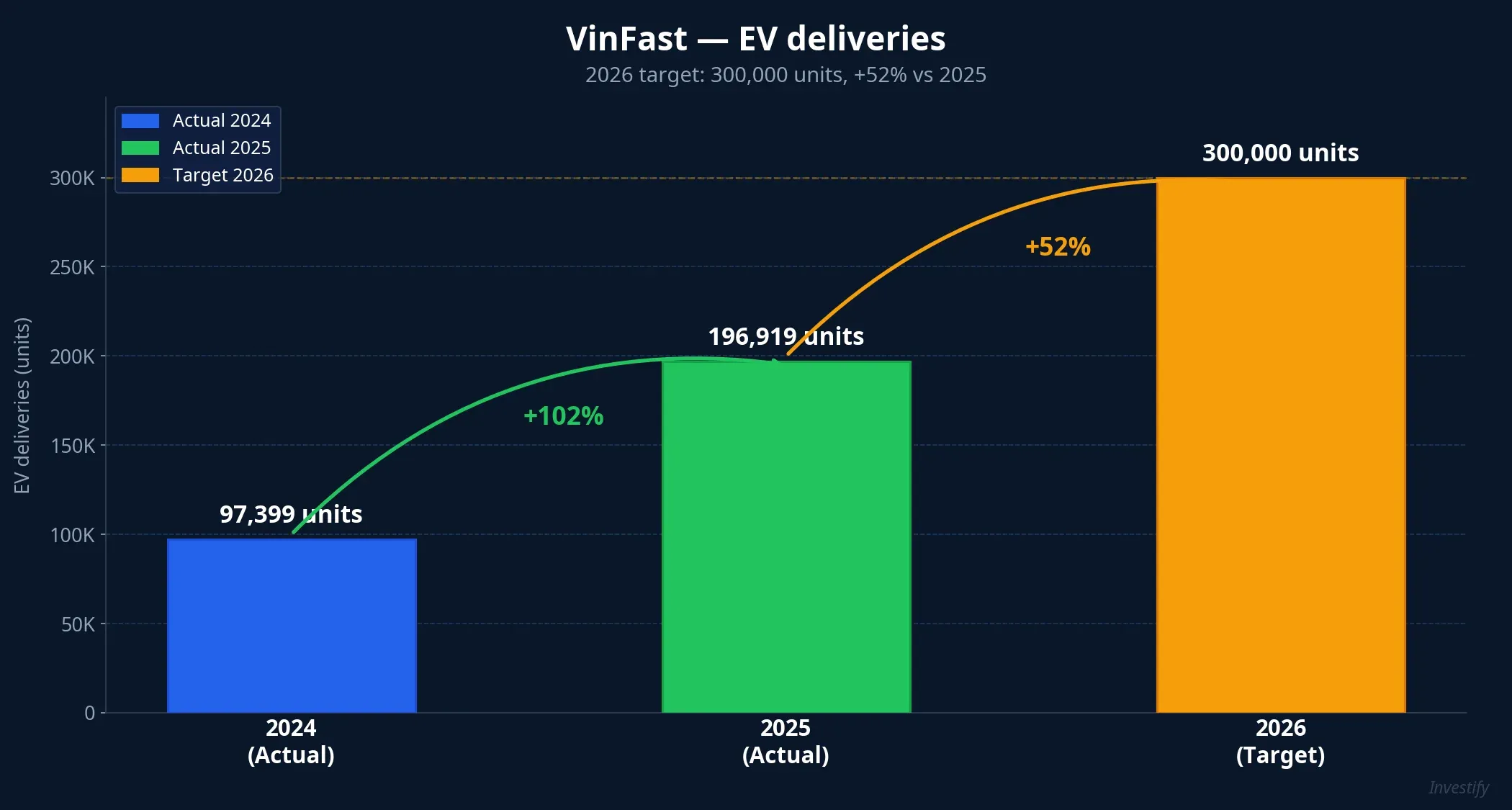

Mechanism 2: VinFast pivots from drag to growth driver

This is the mechanism with the widest swing — and the riskiest leg of the plan. VinFast delivered 196,919 electric vehicles globally in 2025 (up 102% year-on-year), plus 406,498 electric motorcycles (up 473%), with full-year revenue of VND 90,427.6 billion.AutoPro The 2026 plan targets 300,000 EVs (roughly 52% above 2025) and close to 1 million electric motorcycles (at least 2.5x higher).

What matters is that VinFast’s role in the consolidated picture has flipped. From 2022 to 2024, VinFast was the “loss-making segment” weighing on consolidated results: manufacturing losses, large capex, direct deduction from group profit. The 2026 plan implicitly assumes VinFast either contributes positively to net profit or, at minimum, narrows the loss meaningfully so group-level costs do not swallow the Vinhomes contribution. Moving from “deep loss” to “breakeven or profit” within one year requires VinFast to capture both manufacturing scale and unit-cost efficiency.

The assumption to test. A 52% rise in EV output within a single year is achievable if the Hai Phong plant, along with the India and Indonesia projects, run smoothly, and if domestic and export markets absorb the new output. The risk sits on the demand side, not just capacity: delivering 300,000 cars requires selling 300,000 cars. The 2025 base reached close to 197,000 units with the help of support policies and home-market advantage; adding another 100,000+ units in 2026 requires international distribution channels to scale in step with production. Monthly delivery figures — especially outside Vietnam — are the most direct signal for this scenario.

Mechanism 3: The VND 10 trillion upward revision on April 20

On April 20, exactly two days before the shareholder meeting, Vingroup revised the plan upward: an additional VND 35 trillion in revenue and VND 10 trillion in net profit versus the earlier disclosure.CafeF The net profit target moved from VND 25 trillion to VND 35 trillion — a 40% jump from a single document.

There are two ways to read this revision. The first: the pipeline for subsequent quarters became clearer than the late-Q1 projection, and management wanted shareholders to see the updated number rather than the older one. The second: this is expectation management ahead of the meeting — publishing an ambitious bar to discipline the internal plan. The two readings are not mutually exclusive and likely coexist.

A notable data point: on the same April 20, Vinhomes lifted its 2026 net profit target from VND 50 trillion to VND 60 trillion, and Vinpearl doubled its profit target from VND 1.5 trillion to VND 3 trillion. Three companies raising targets on the same day points to a coordinated move at the group level, not piecewise technical adjustments.

The assumption to test. Vingroup’s plan-completion rate from 2022 to 2025 shows a company setting relatively cautious targets after a volatile stretch. The 2025 result of VND 11,065 billion sat very close to the VND 10 trillion plan. Jumping directly to VND 35 trillion in 2026 means Vingroup is breaking the cautious target-setting frame it has held for years. Investors holding VIC should read completion rate after each quarterly report rather than wait for year-end.

The P/B 9.88x signal: expectations priced in early

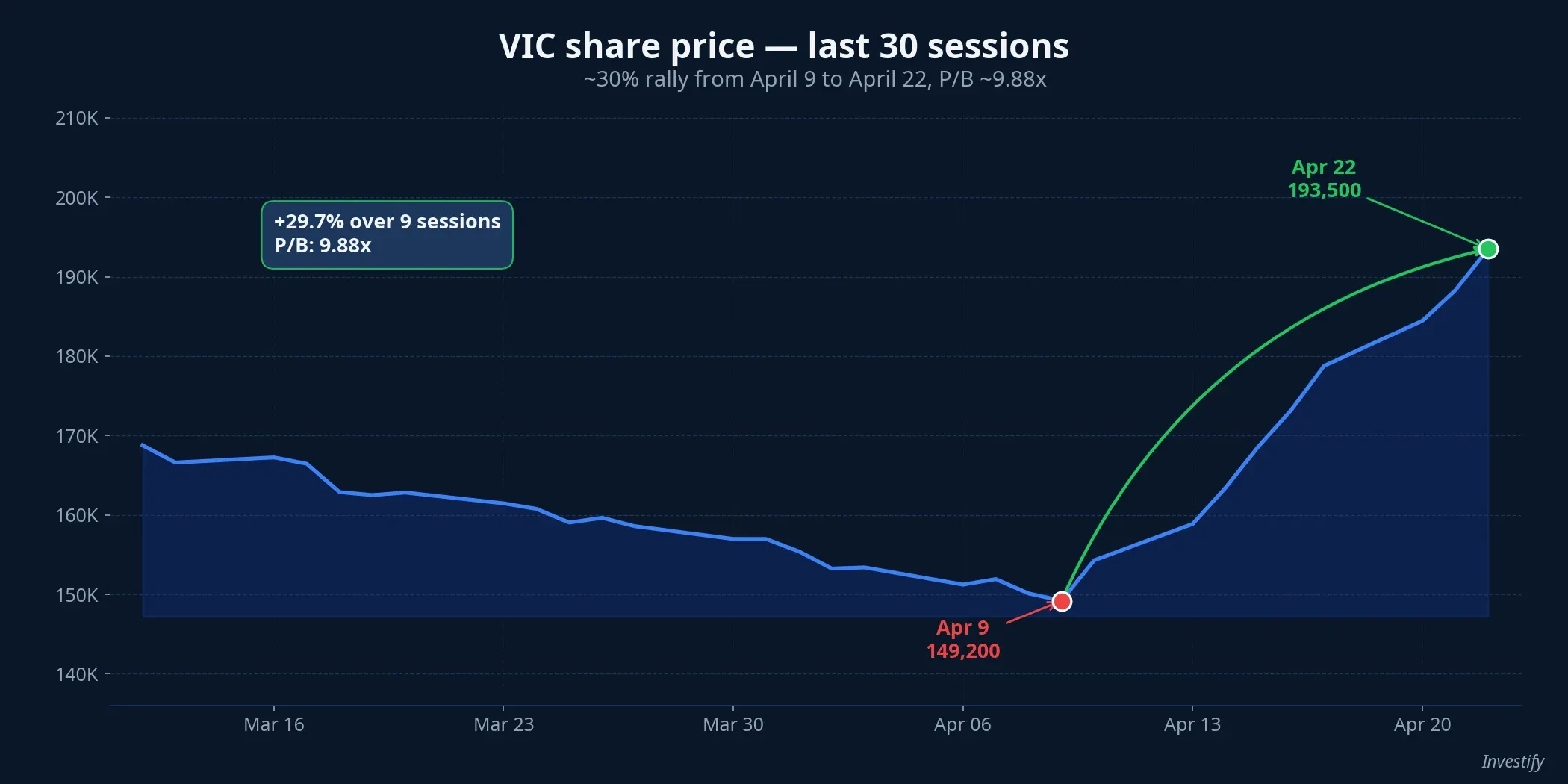

VIC ended the April 22 morning session at VND 193,500, down a marginal 0.10% versus the prior session.Dan Viet Over roughly two weeks, VIC moved from the VND 149,200 area (April 9) to VND 193,500 — a rise of nearly 30%. P/B is currently around 9.88x, well above the multi-year average.

What does this P/B imply for the VND 35 trillion scenario? The market has priced in most of the expectation associated with the new plan early. If Q1 or Q2 reports confirm the pipeline is on track, P/B can compress naturally as the denominator (book value) grows along with retained earnings — the share price does not need to fall. On the other hand, if the first quarter misses, current valuation becomes fragile: the downside on a price revision exceeds the remaining upside.

Three checkpoints over the next 12 months

For shareholders holding VIC, VHM, or VN30 index funds with heavy Vin exposure, what matters is not tomorrow’s price but the checkpoints that validate or invalidate the assumptions. The “3x” figure is not a completed fact — it is a promise to be verified across four upcoming reporting periods:

- VIC Q1 2026 consolidated report: the completion rate for the VND 35 trillion plan after Q1 is the first signal on whether the actual pipeline is tracking.

- Monthly VinFast EV deliveries (especially India and Indonesia): the most direct signal for the 300,000-unit scenario.

- Vinhomes mega-project handover progress: determines whether VND 60 trillion at the subsidiary materializes.

The thesis of this post: the VND 35 trillion target is not a random number. It rests on three specific mechanisms, and all three carry assumptions that can be tested against quarterly data. The risk is not whether the target is reasonable — it is whether investors have the patience to read each quarterly report rather than read the daily price. At a P/B near 10x, the standard defensive frame for a large-cap stock that has already run hard is to track quarter by quarter whether the assumptions are being confirmed or slipping, and only then to consider adjusting position size.