On May 26, 2026, Micron Technology’s stock climbed 19% and crossed the $1 trillion market cap threshold for the first time.CNBC Worth noting: the move came on a session when US tech stocks were broadly rallying, so the 19% gain is not entirely Micron’s own story. Regardless, the event completes a picture that has been forming for months: all three core layers of the AI chip chain are now trillion-dollar businesses. The more interesting observation is not that the numbers look similar, but that each layer is priced by a fundamentally different market mechanism.

Three Layers, Three Steps on the Valuation Staircase

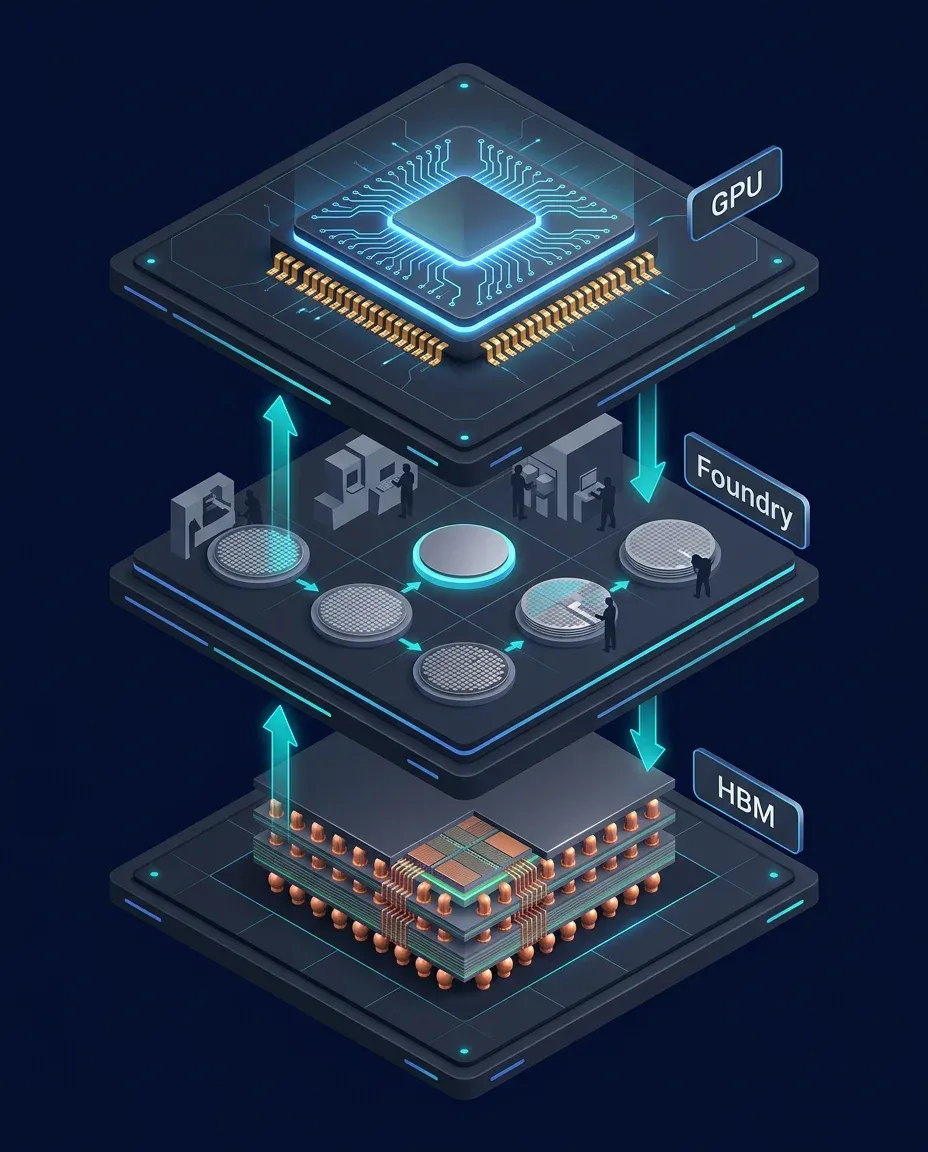

A cluster of AI servers needs three things working in concert. At the top sits the graphics processing unit (GPU), the computational brain dominated by Nvidia. In the middle is the semiconductor foundry, which physically manufactures the chips from design blueprints, a role TSMC owns. At the base is high-bandwidth memory (HBM), the high-speed data store that feeds GPUs, where Micron, SK Hynix, and Samsung compete.

The market caps form a clear staircase. Nvidia leads at approximately $5.23 trillion, making it the world’s most valuable company.CompaniesMarketCap TSMC sits in the middle at approximately $2.14 trillion.CompaniesMarketCap And Micron just joined the trillion-dollar club at $1 trillion. The staircase is not accidental. It reflects three different business models and three different ways the market prices each layer.

Three Pricing Mechanisms, Three Risk Profiles

The standout figure for Nvidia is a gross margin that consistently exceeds 70%. The company controls both the GPU hardware and the accompanying CUDA software ecosystem, leaving customers with virtually no substitute. The market rewards this with the highest price-to-revenue multiple in the sector, essentially betting on multi-year AI growth with margins that cannot be competed down.

TSMC operates on the opposite model: heavy capital investment, a gross margin around 50%, but steady and predictable. Without TSMC, neither Nvidia nor Apple has an advanced chip to sell. The market prices TSMC as the industry’s toll road. The revenue multiple is lower than Nvidia because of the capital intensity and the constant need to reinvest, but cash flows are regular and foreseeable.

Micron is the most compelling case. For decades, memory stocks were priced as a classic commodity cycle: when supply ran ahead of demand, DRAM prices fell sharply and margins nearly evaporated; when supply tightened, profits surged before reversing again. That pattern kept memory’s revenue multiple at the bottom of the three layers. HBM is the story that changes the equation.

Why HBM Is Different from Standard DRAM

HBM is fundamentally still DRAM, but manufactured in vertically stacked layers connected through thousands of through-silicon vias. This architecture delivers enormous bandwidth in a tiny footprint — exactly what AI GPUs require. An H100 carries 80 GB of HBM; the newer B200 goes up to 192 GB.

HBM is harder to produce than standard DRAM, with lower yields, so supply cannot scale quickly when demand spikes. Major customers must sign long-term contracts committing to volumes and partially locking in prices in advance. Switching costs are also high because each HBM variant must pass a rigorous qualification process for each specific GPU generation. The result: instead of fluctuating on spot markets like standard DRAM, HBM trades under long-term supply relationships with higher, more stable margins. Micron’s entire 2026 HBM output, including the new HBM4 generation, is already sold out.ainvest That has never happened with a memory product before. This is the thesis behind UBS raising its Micron price target from $535 to $1,625, a three-fold increase.The Tech Marketer

A Three-Way Race in the Memory Layer

Unlike Nvidia’s near-monopoly on GPUs, the memory layer is a three-way competition. SK Hynix leads with approximately 62% HBM market share in Q2 2025,Astute Group Micron follows at approximately 21% and has overtaken Samsung at approximately 17%. Micron’s advantage does not come from a dominant position the way Nvidia’s does. It comes from successfully qualifying as a supplier for the latest GPU generations. Samsung is forecast to push its share back above 30% in 2026 as its new HBM products gain acceptance. The high margins Micron is currently earning depend on maintaining a qualified-supplier position through the HBM4 cycle, not on a structural moat.

The Oversupply Risk After 2028

The global HBM market is forecast to grow from approximately $35 billion in 2025 to around $100 billion by 2028, a roughly 186% increase over three years. Demand from AI data center buildouts remains strong, but precisely that growth rate is pulling heavy capital investment from all players to expand production capacity. Even the most bullish reports flag oversupply risk after 2028, when multiple new fabs come online simultaneously.

The UBS thesis rests on undersupply persisting through 2026 and into 2027. If new capacity arrives earlier than expected, the memory layer will remind investors that its cyclical nature has never fully disappeared. The signal worth watching is not the $1,625 price target but whether HBM maintains sold-out capacity and supply discipline through the HBM4 generation.

Accessing the AI Chip Chain from Vietnam

The question is not which layer is best, but which layer fits a given risk appetite. Investors willing to pay a premium for durable long-term growth and the strongest competitive barriers will look at the GPU layer. Those who prioritize steady cash flows and an essential, hard-to-replace position will look at the foundry layer. Those comfortable accepting cyclical exposure in exchange for a valuation re-rating opportunity will look at memory, where the revenue multiple remains the lowest of the three despite improving fundamentals.

For Vietnamese investors, three access routes exist. Opening an account at an international brokerage is the most direct way to own Micron, Nvidia, or TSMC, but requires managing currency conversion costs, reporting obligations, and foreign exchange risk. Buying globally diversified technology fund certificates offers a simpler indirect route, though the portfolio will not be concentrated in semiconductors. Domestic stocks benefiting indirectly through the supply chain are the most accessible, but their correlation to the global chip cycle is considerably weaker.

Micron crossing $1 trillion is a milestone. More usefully, it completes the picture needed to analyze the AI chip chain in depth. The question that will matter most in coming quarters: can HBM supply discipline hold through the capacity expansion cycle?