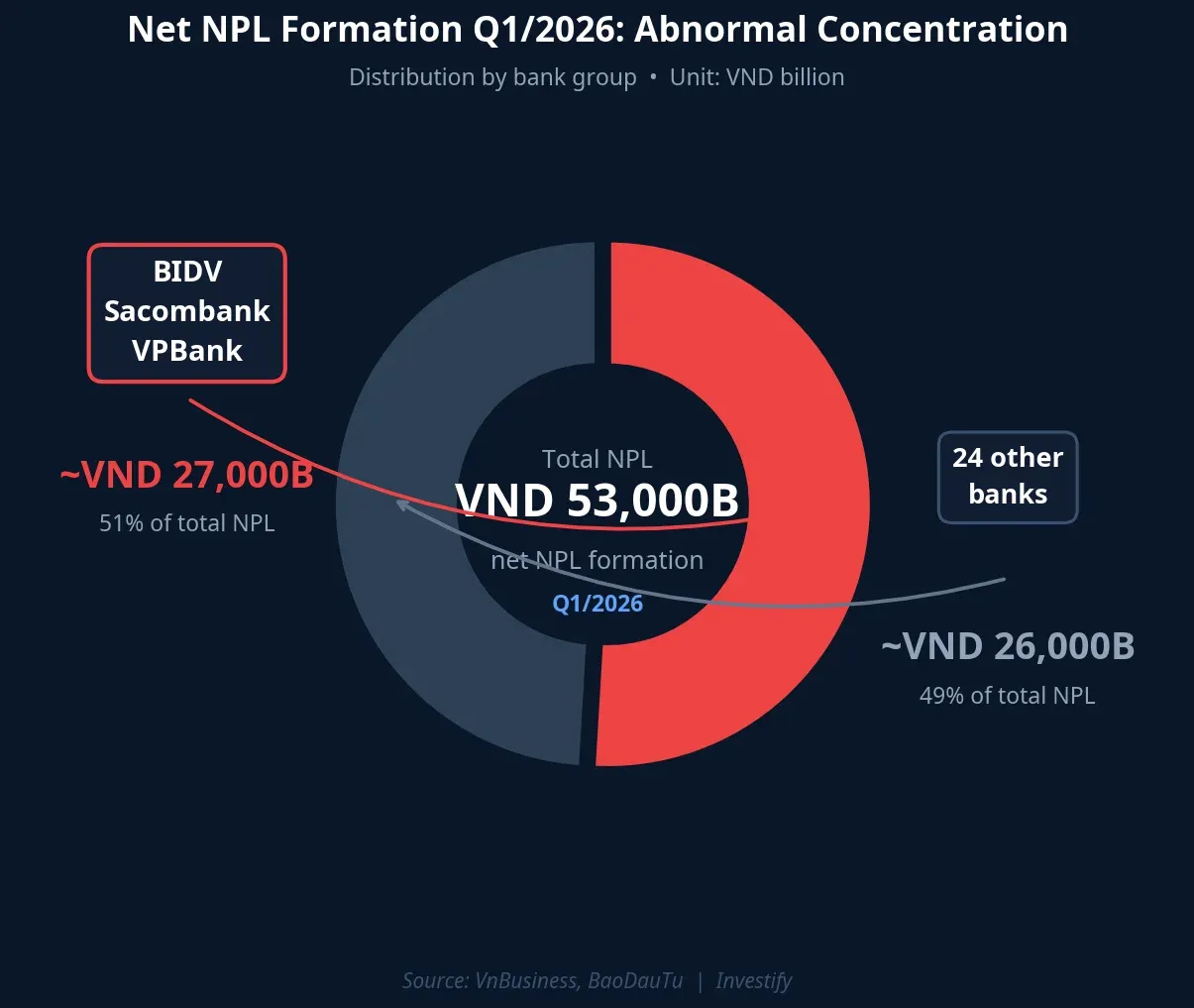

On May 28, the banking sector was among the top four worst-performing industries on the exchange, with 22 of 27 listed bank stocks closing in the red. The VN-Index finished the session at 1,863.67 points, down 10.76 points. The immediate trigger was the release of Q1/2026 system-wide NPL data, which showed net new NPL formation of VND 53,000 billion.BaoMoi

But the headline aggregate is hiding something more important. More than 50% of that net NPL formation landed in just three banks: BIDV, Sacombank, and VPBank. The real question for investors holding bank stocks is not “is the whole system in trouble?” but rather “have those three banks provisioned enough, and which scenario will play out in the second half of 2026?”

The Aggregate Is Masking Real Differentiation

As of end-Q1/2026, total NPLs across 27 listed banks reached VND 292,160 billion, up VND 28,065 billion from end-2025.VnBusiness An 11% increase in a single quarter is notable, but the aggregate figure alone does not tell the full story. Group 5 NPLs (loans with high loss probability) across the system approached VND 168,543 billion, with just five banks — Sacombank, BIDV, VietinBank, VPBank, and Vietcombank — accounting for roughly VND 89,000 billion of that total.Thời Báo Tài Chính VN In other words, more than half of the system’s most dangerous NPL stock sits on the balance sheets of a small group of banks.

This is why sector-level analysis produces blurry answers. Bank-by-bank analysis is the only way to reach conclusions that are actually useful for portfolio decisions.

The Top 3 Banks: Balances and Growth Rates

Looking at individual numbers, the degree of differentiation becomes clear.

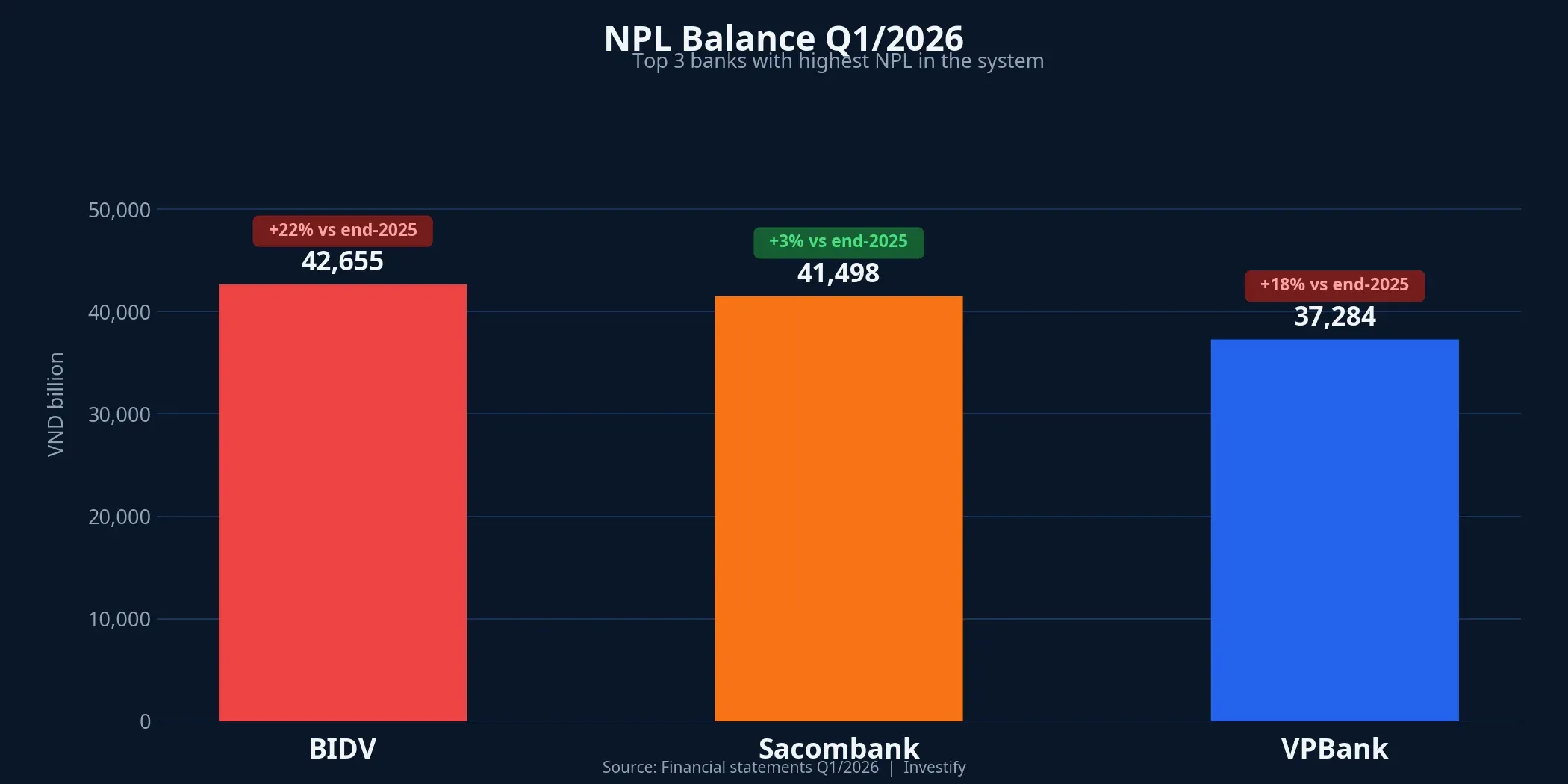

BIDV leads the system with VND 42,655 billion in NPL balance, up VND 7,678 billion — equivalent to 22% — in just three months.VnBusiness The NPL ratio remains a controlled 1.76% because BIDV’s loan book is very large.NguoiQuanSat What warrants watching is the pace of new NPL formation, not the absolute ratio.

Sacombank recorded VND 41,498 billion, up a more modest 3%, but its NPL ratio has climbed to 6.62%, well above the State Bank of Vietnam’s recommended 3% ceiling.NguoiQuanSat This is the legacy of a prolonged restructuring process the bank has not fully exited.

VPBank reported VND 37,284 billion, up 18% from end-2025, with an NPL ratio of 3.58%, just crossing the 3% threshold.NguoiQuanSat The 18% rise reflects retail and consumer lending converting to NPLs faster than the market had expected.

Provisioning Buffers Are Thinning

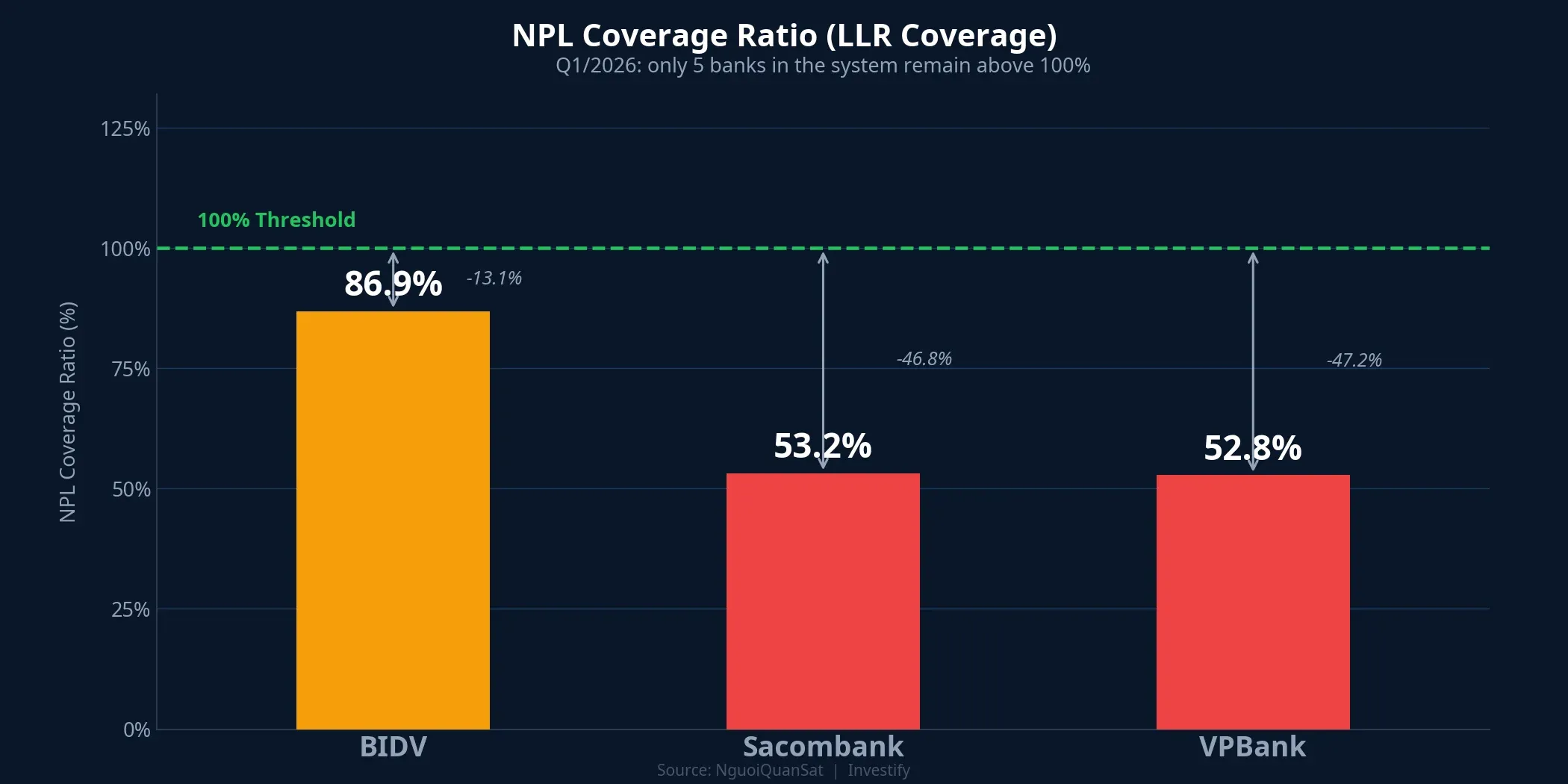

The more important issue is not just the scale of NPLs but each bank’s capacity to absorb further stress. The average system-wide NPL coverage ratio fell from 83.3% at end-2025 to 74.9% at end-Q1/2026.NguoiQuanSat Only 5 banks in the entire system now maintain coverage above 100%, the fewest in many years.

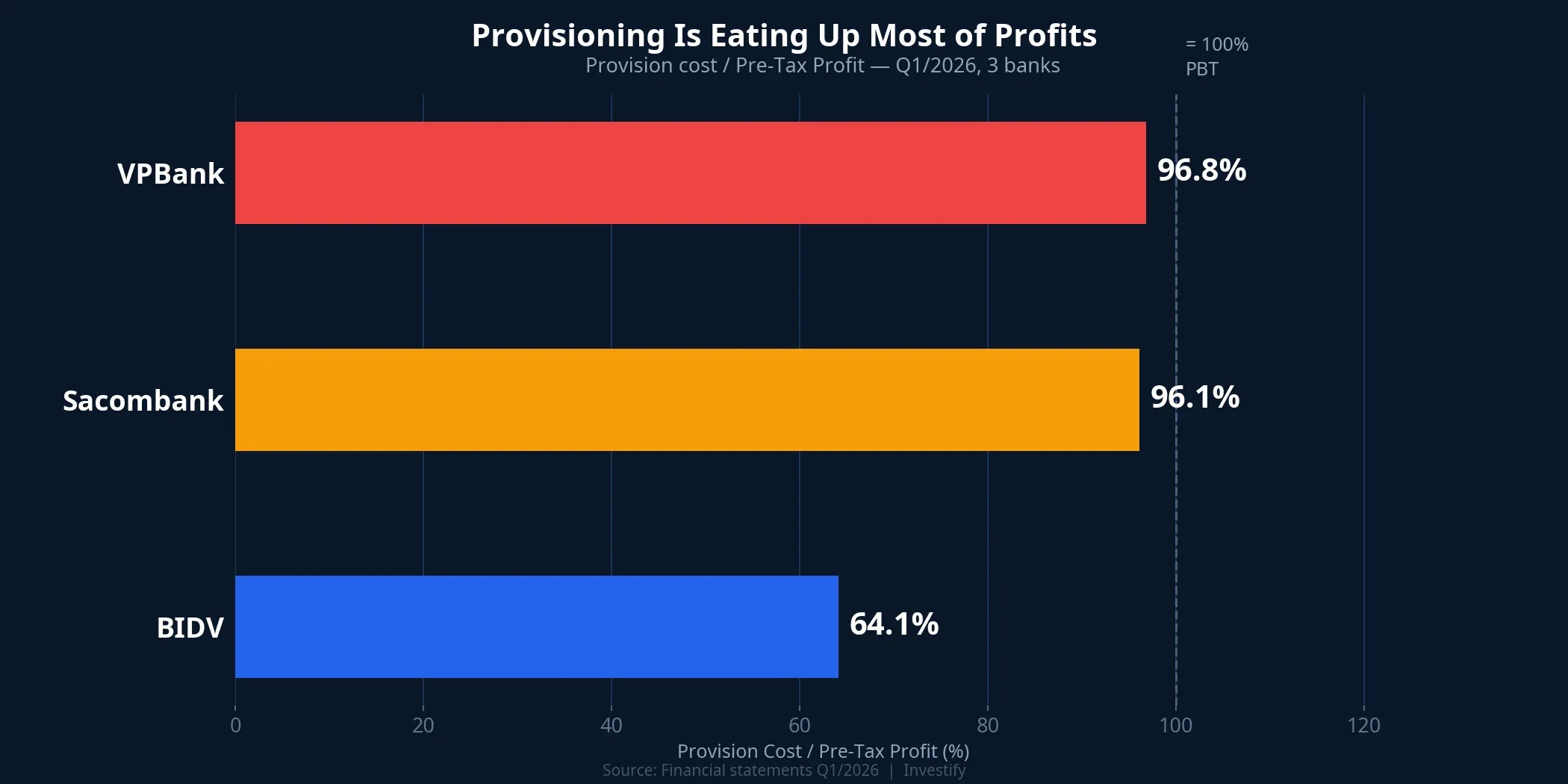

For the three focal banks, the buffer picture is starkly different. BIDV holds a coverage ratio of 86.9%, but provisioning has already consumed 64.1% of pre-tax profit (PBT) in Q1. Sacombank’s coverage ratio stands at just 53.2%, meaning there is roughly VND 0.53 in provisions for every VND 1.00 in NPLs. Provisioning expense consumed 96.1% of PBT, with Q1 provisioning up 109% year-on-year and profit down 42.7%.BaoDauTu VPBank’s coverage is a near-identical 52.8%, with provisioning consuming 96.8% of PBT.

Two of the three banks are in a position where almost every dong of profit they generate is absorbed by provisioning charges. The remaining buffer to absorb one more difficult quarter is razor thin. BIDV still has room, but meaningfully less than a year or two ago.

Two Scenarios for H2 2026

The Q1 data supports two interpretations that are both internally coherent.

Scenario A: Front-loaded provisioning is complete. Under this reading, Sacombank’s record provisioning and VPBank’s near-97% PBT absorption in Q1 are positive signals, not negative ones. Management spotted NPL formation early and front-loaded the expense recognition. In Q2 and Q3, provisioning pressure eases and profits recover. If this holds, current valuations are pricing in excess fear relative to fundamentals. Confirming signals: absolute provisioning cost in Q2 is lower than Q1, Group 2 loans (special mention) stop growing or decline, and system-wide net NPL formation in Q2 comes in below VND 40,000 billion.

Scenario B: Group 2 loans continue migrating to bad debt. Under this reading, Q1’s elevated provisioning is just the beginning. Group 2 loans across the system have exceeded VND 181,000 billion, and a meaningful portion will continue rolling into Groups 3-5 in Q2 and Q3. MBS has flagged Group 2 loans and real-estate-backed collateral as ongoing sources of provisioning pressure.BaoMoi Mirae Asset has already cut its 2026 profit forecast for Vietcombank — the bank with the strongest buffer in the system — citing provisioning pressure from corporate bonds and new NPLs.BaoMoi If Scenario B plays out, Sacombank and VPBank — which have exhausted most of their buffer in Q1 — could report near-zero or deeply negative earnings in one or two upcoming quarters.

Even in the more optimistic Scenario A, real-estate-linked Group 2 loans remain a source of latent credit risk that has not fully materialized.

The Differentiation Is Already Visible in Q1 Data

The Q1 NPL story is not about the entire banking system sinking. Vietcap has noted that some banks pre-loaded large provisions back in Q4/2025 — ACB being one example — leaving Q1/2026 provisioning relatively light.BaoMoi VietinBank, NamABank, and ABBank were the three lenders that actually saw NPLs fall in Q1, with VietinBank recording a 6% decline.VnBusiness Vietcombank and ACB both maintain provisioning coverage above 100%.

Investors holding shares in well-capitalized state-owned banks, or in private banks that front-loaded provisions earlier, are in a fundamentally different position from those holding Sacombank or VPBank. Reacting to sector-level noise without examining bank-specific data is likely to produce mistakes in both directions: unnecessary selling where it is not warranted, or inaction where genuine portfolio review is needed.

Four Metrics to Watch Before the Q2 Report

The Q2/2026 report, due for release in late July, will provide the evidence needed to determine which scenario is playing out. Four specific indicators to track for each of the three focal banks:

First, system-wide net NPL formation in Q2. Below VND 40,000 billion points toward Scenario A; above VND 50,000 billion tilts the balance toward Scenario B.

Second, movement in Group 2 loans (special mention). If Group 2 balances level off or decline, the forward provisioning burden will ease materially. If they continue rising by more than 5% over Q1, a second provisioning wave is on the way.

Third, average system-wide NPL coverage ratio. Holding above 75% signals manageable stress. A drop below 70% is a warning that realized losses are accelerating.

Fourth, provision cost as a share of PBT at Sacombank and VPBank. Both banks need to bring this ratio below 80% before any recovery in earnings can be called genuine.

The Q2 earnings season will separate banks that have passed the worst of their provisioning cycle from those that are still working through it. In the meantime, banking sector stocks are likely to remain sensitive to every new NPL-related data point as it emerges. For investors already holding positions in the sector, the immediate priority is knowing which group each bank belongs to in this diverging landscape. That understanding is the baseline for any decision to hold, reduce, or wait for further confirmation from Q2 results.