On the morning of May 29, 2026, dozens of newspapers and TV broadcasts ran the same headline: “E10 gasoline mandatory nationwide from June 1.” The framing spooked millions of motorcycle and car owners, prompting questions about whether gas stations would stop selling anything else and whether older vehicles might break down. Social media quickly circulated lists of “incompatible” motorcycles, and some people began stockpiling conventional RON95 before the deadline.

What most headlines left out: the obligation in Circular 50/2025/TT-BCT falls on gas stations, not on consumers. Those are two entirely different parties, with very different legal and financial consequences. And the genuine risk worth watching sits in a corner that the “engine damage” story has almost entirely crowded out.

Who Does Circular 50 Actually Bind?

The Ministry of Industry and Trade issued Circular 50/2025/TT-BCT on November 7, 2025, effective January 1, 2026, with mandatory enforcement beginning June 1, 2026.Báo Chính phủ The parties bound by the circular are fuel traders, blending operators, and distributors. Drivers are not covered. Not a single clause in the regulation requires drivers to use E10.

More specifically: E5 RON92 will remain legally available for sale until December 31, 2030.Báo Thanh Hoá Consumers have nearly 4.5 more years to choose whatever fuel suits their vehicle, without compulsion. Aviation, defense, and all diesel fuels also fall outside the mandatory ethanol blending scope.

The distinction between “stations must sell E10” and “drivers must use E10” is not a semantic quibble. It determines who must invest in blending infrastructure, who absorbs conversion costs, and who retains the right to choose the fuel that fits their engine.

Which Vehicles Actually Need Attention

Bad news amplified on social media tends to lump “old vehicles” into a single undifferentiated block, making the hazard seem broader than it is. Technical data from automotive and motorcycle associations tells a narrower story.

For motorcycles, the genuine risk is concentrated in models produced before roughly 1998–2000. Specifically: Honda Dream, Super Cub, and older Wave S variants; Yamaha Sirius and Jupiter from around 2005–2009; Suzuki Viva, FX, and Best; older SYM Elegant and Attila models. These use carburetors with rubber hoses and plastic gaskets that can degrade under regular ethanol exposure. For cars, some pre-2006 models with higher octane requirements may be incompatible with E10.Hyundai Gò Vấp

Vehicles made after 2010 overwhelmingly meet Euro 3 standards or higher, with rubber and metal components in the fuel system engineered to tolerate a 10% ethanol blend. For this group, E10 poses no technical concern.

The corrosion mechanism also has specific conditions: ethanol absorbs moisture and dislodges sediment inside older fuel tanks, eventually clogging injectors or carburetors. This primarily affects infrequently used vehicles where fuel sits in the tank for extended periods. Owners in the at-risk group can simply continue using E5 RON92, which stays on the forecourt until 2030.

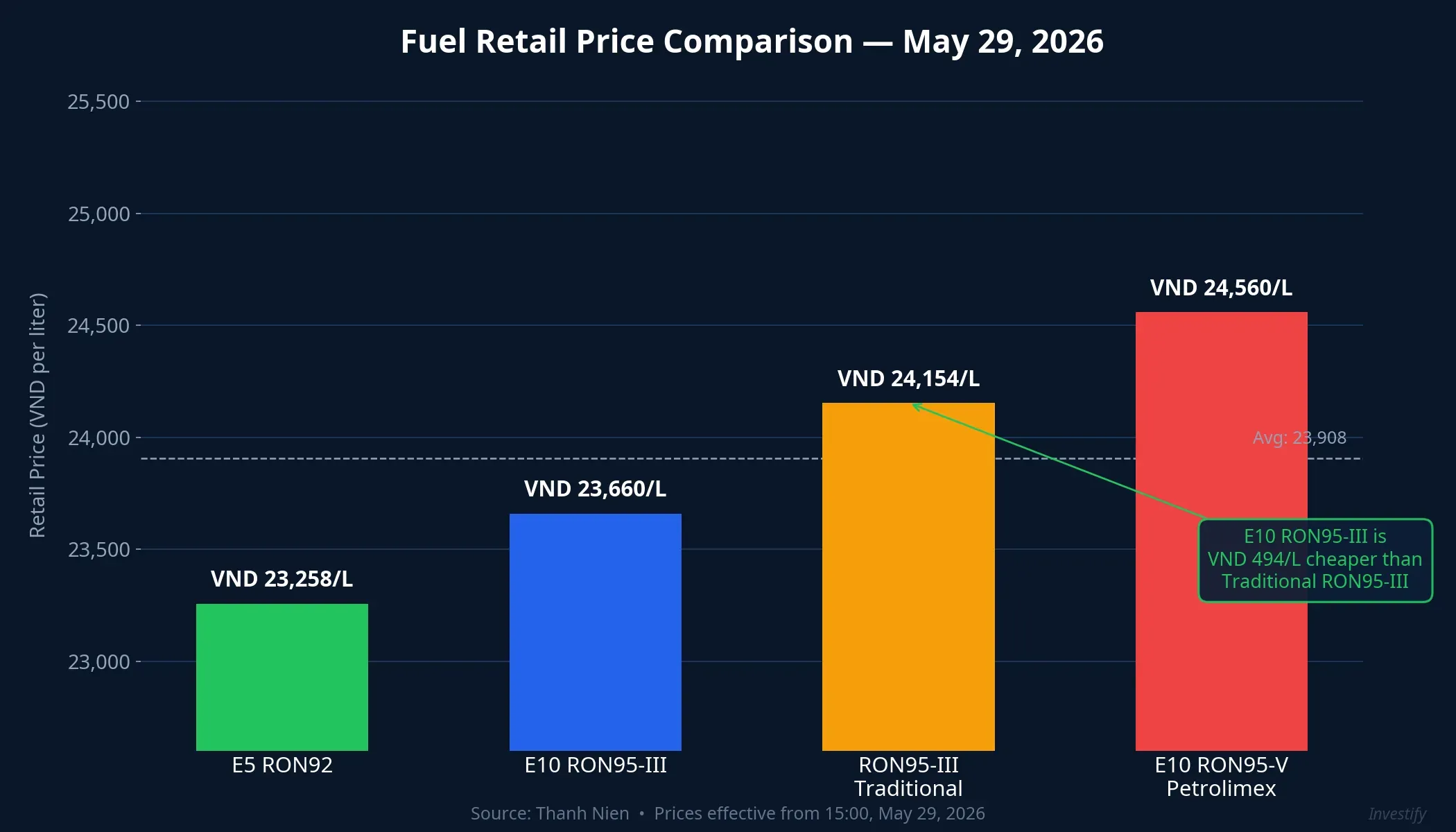

The Price Reality: E10 Is Cheaper, Not More Expensive

Another fear circulating online is that E10 will push pump prices higher. The May 29, 2026 pricing board says the opposite.Thanh Niên

E10 RON95-III currently sits at VND 23,660 per liter, VND 494 cheaper than traditional RON95-III at VND 24,154. E5 RON92 is the cheapest option at VND 23,258 per liter. Petrolimex’s E10 RON95-V is higher at VND 24,560 per liter, reflecting its higher octane segment.Thanh Niên

The VND 494 per liter difference has real-world weight. Filling a 4-liter motorcycle tank saves roughly VND 2,000 per stop; filling a 50-liter car tank saves around VND 24,500. Modern engines do consume roughly 1–2% more E10 than conventional RON95 due to the lower energy density of ethanol, so the nominal saving narrows somewhat at the pump, but it does not reverse direction.

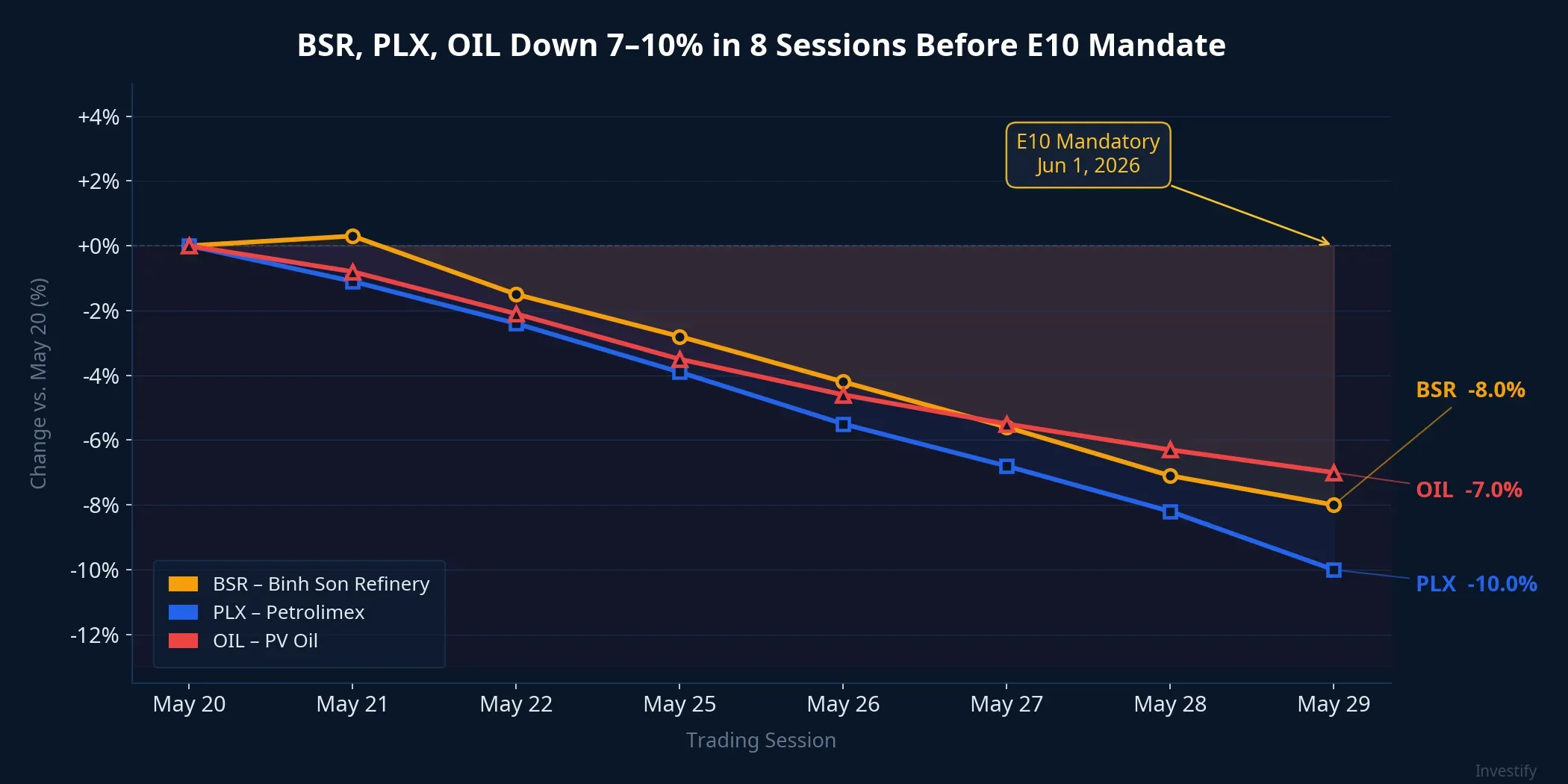

BSR, PLX, OIL: Infrastructure Ready, Market Unimpressed

On the supply side, BSR (Binh Son Refinery, Dung Quat) has completed upgrades to its ethanol blending systems.Người Quan Sát From May 2026, BSR is expected to supply approximately 80,000–100,000 cubic meters of E10 per month by both road and sea. Dung Quat’s biofuel plant is running at 75–80% capacity and is expected to reach 90% in June. PLX (Petrolimex) ran pilot E10 sales in Ho Chi Minh City and Quang Ngai from August 2025 to stress-test its pump and storage systems before national rollout. PV OIL (OIL) has completed upgrades across its 13 regional depots.CafeBiz

The equity market, however, is not celebrating. If E10 represented a clear earnings catalyst for these three stocks, prices would have run ahead of June 1. Instead, all three have declined meaningfully over the eight trading sessions from May 20 to May 29: BSR fell to VND 28,250 per share (down roughly 8% from the prior week); PLX dropped to VND 39,450 (down roughly 10% from May 20); OIL slid to VND 14,600 (down roughly 7% from May 20).

The market appears to be pricing E10 as an infrastructure transition already embedded in valuations, not a new earnings driver. The blending margin on ethanol is thin: at an assumed average margin of around VND 500 per liter on the ethanol component, each cubic meter of E10 adds only a few hundred thousand dong in incremental value: not enough to meaningfully shift EPS at companies with revenues in the tens of trillions. Capital expenditure on storage and pipeline upgrades has already been recognized. The May 21 decision to halt contributions to the petroleum price stabilization fund also compresses retail margins.

Where the Real Risk Actually Sits

The risk that social media is amplifying — older vehicles suffering engine damage from E10 — is real but narrow, and it has a ready solution (E5 remains available until 2030). The risk more worth watching lies in domestic ethanol supply.

BSR estimates it needs approximately 300,000 cubic meters of ethanol per month just for its own feedstock. Current domestic ethanol production capacity falls short of total market demand once E10 becomes the default across the entire distribution network. The gap will need to be covered by procurement contracts and imports during the transition period.

The playbook from early movers is instructive. Brazil has sustained E10 for decades, backed by a strong domestic ethanol industry and flexible tax policy that keeps consumer costs stable. The United States mandated E10 as a standard in the 2010s but ran into bottlenecks at terminal storage and vehicle warranty limits. Thailand built in a long transition window with broad consumer education to clarify the difference between blend levels. The common thread: countries that secured adequate domestic ethanol supply and preserved consumer choice encountered far less friction.

Vietnam’s decision to keep E5 available until 2030 is the right policy step. The remaining question is ethanol plant capacity and import costs over the next 6–12 months. If a domestic shortage materializes and Vietnam imports more than projected, blending margins at the major distributors will face additional downward pressure. That is the variable that deserves more attention than the “engine damage” narrative dominating social media.

Signals to Watch

Second-quarter 2026 earnings for BSR, PLX, and OIL, due in July–August, will be the first reports to reflect the real-world costs of a full national E10 rollout, covering blending margins and ethanol input costs. Two data points are worth tracking in parallel: progress at the Dung Quat biofuel plant toward 90% capacity utilization in June, and the price of imported ethanol if domestic supply falls short of plan.

For consumers, the answer is already clear today: E5 RON92 is still at the pump. No need to stockpile, no reason to panic. It is, however, worth checking what model year your vehicle is before the nearest station is displaying only E10 labels.