On May 28, the U.S. Bureau of Economic Analysis (BEA) reported that the Personal Consumption Expenditures (PCE) price index rose 3.8% year-on-year in April 2026, the highest reading since 2023.BEA Core PCE, the Fed’s preferred inflation gauge for monetary policy decisions, came in at 3.3%.Wichita Liberty Both figures remain nearly two percentage points above the Fed’s 2% target. From Hanoi, this looks like a distant data point. But it is a key link in the chain of constraints keeping the real return on Vietnamese savings accounts near zero or negative in 2026. To trace that chain, we need to put both central banks side by side and ask the same question: who is stuck, and by what mechanism?

The Fed: Inflation Above Target, Rates Going Nowhere

The Fed’s macro picture is fairly straightforward. April marks roughly the fourteenth consecutive month that headline PCE has stayed above 2%. There is one nuance worth noting: the monthly pace is decelerating. Month-on-month, PCE rose just 0.4% in April, down from 0.7% in March.Wichita Liberty The trend is cooling, but the level remains too far from the target for the Fed to act.

As a result, the Fed has held its policy rate unchanged at 3.50–3.75% for several months running.CNBC The bind comes from two opposing forces acting on the institution simultaneously. President Donald Trump has publicly pushed for lower rates, and Kevin Warsh, the newly installed Fed Chair, took office with the implicit expectation that he would ease policy. But cutting rates while PCE sits at 3.8% sends the wrong signal: markets would interpret it as the Fed prioritizing growth over price stability, anchoring inflation expectations higher rather than lower. The result: markets have all but abandoned expectations for any rate cut in 2026.Chase

The last time the Fed was in a similar standstill was 2022–2023, when sustained rate holds were needed to cool post-pandemic inflation. That cycle also tightened the foreign exchange constraint on Vietnam’s central bank. History suggests these cycles do not resolve quickly.

The Transmission Channel: A Strong Dollar, a Narrower Window

Holding rates high for an extended period creates an indirect effect on Vietnam through the exchange rate channel. Elevated U.S. interest rates sustain the dollar’s attractiveness, keeping the USD/VND rate at major commercial banks around VND 26,300–26,350 per dollar, up approximately 3% over the past twelve months.GiaVang.net Market analysts project the rate could move to VND 26,350–26,700 in Q2, with some forecasts flagging the VND 27,000 level as a tail risk.Dân Việt

An important clarification: the interest rate differential is not the sole driver of the exchange rate, nor even the dominant one. The VND depreciation is largely driven by broader macro forces: U.S. policy expectations, Treasury yield volatility, and risk-averse sentiment ahead of inflation data. But with the State Bank of Vietnam’s (SBV) policy rate at 4.50% per annum versus the Fed’s 3.50–3.75%, the carry spread has narrowed to just 0.75–1 percentage point. With that cushion thin, any significant rate cut by the SBV risks compressing the carry further and rekindling downward pressure on the dong.

The SBV: Wanting to Cut, Unable to Follow Through

This is the core difference between the two central banks. The Fed wants rates high and is holding them there. The SBV wants to cut to support economic growth, but the market is not fully cooperating.

At a meeting hosted by the SBV on April 9, the central bank asked commercial banks to stabilize and reduce both deposit and lending rates to support growth.Thời báo Tài chính Several banks responded promptly: PVcomBank, Agribank, VPBank, and Sacombank each trimmed rates by 0.2–0.5 percentage points at longer tenors. But looking at the industry-wide picture, the guidance did not win out. The industry average 12-month deposit rate actually edged higher, moving from 5.77% on March 18 to 5.96% on May 11. Banks including VietinBank, MB, and Techcombank raised rates to defend their liquidity positions and compete for funding, offsetting the group that complied with the SBV’s request.

The macro picture here is telling: the SBV is caught from both sides. Externally, the exchange rate constraint limits how far it can cut. Internally, interbank market dynamics and commercial banks’ own funding costs resist the downward push. These two forces largely cancel each other out, keeping deposit rates from falling as far as the central bank would like.

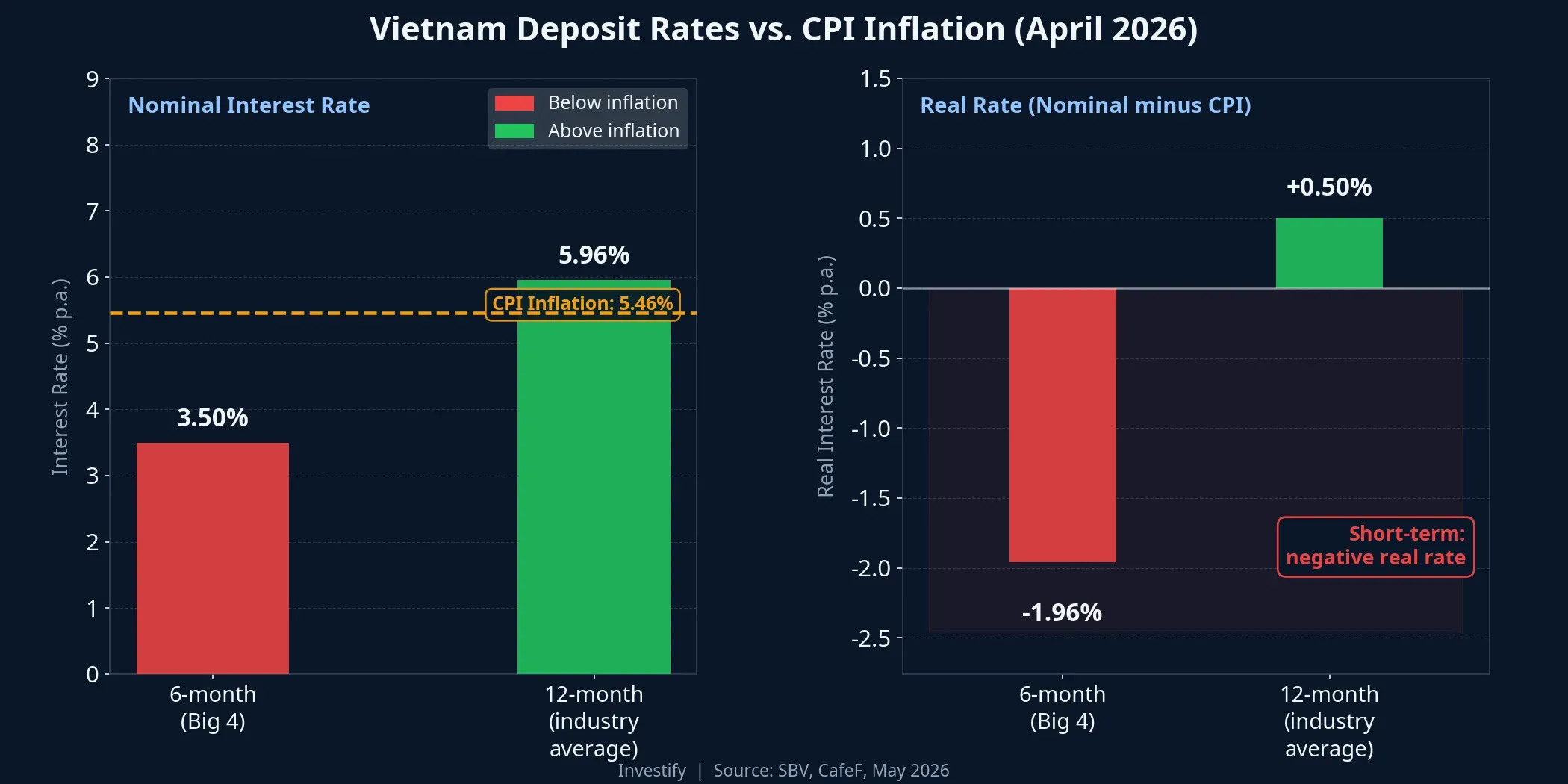

Real Rates Below Zero: What the Numbers Show

Put both constraints side by side and the picture comes into focus. Vietnam’s CPI rose 5.46% year-on-year in April 2026, with the four-month average up 3.99%.CafeFTTTCTT Against that backdrop, the six-month deposit rate at Big 4 banks is around 3.50% per year at the counter. The real return for short-term depositors is approximately negative 1.96 percentage points.

The 12-month tenor looks better. At the industry average of 5.96%, the real rate is a small positive 0.50 percentage points above April CPI. That is technically positive, but the margin is razor thin. If CPI picks up by half a point in coming months, real rates slip negative again.

The key point for understanding this correctly: the situation persists not because the SBV lacks the will to cut rates. The constraint is structural and external. As long as U.S. inflation keeps the Fed’s hands tied, the SBV’s policy room remains narrow.

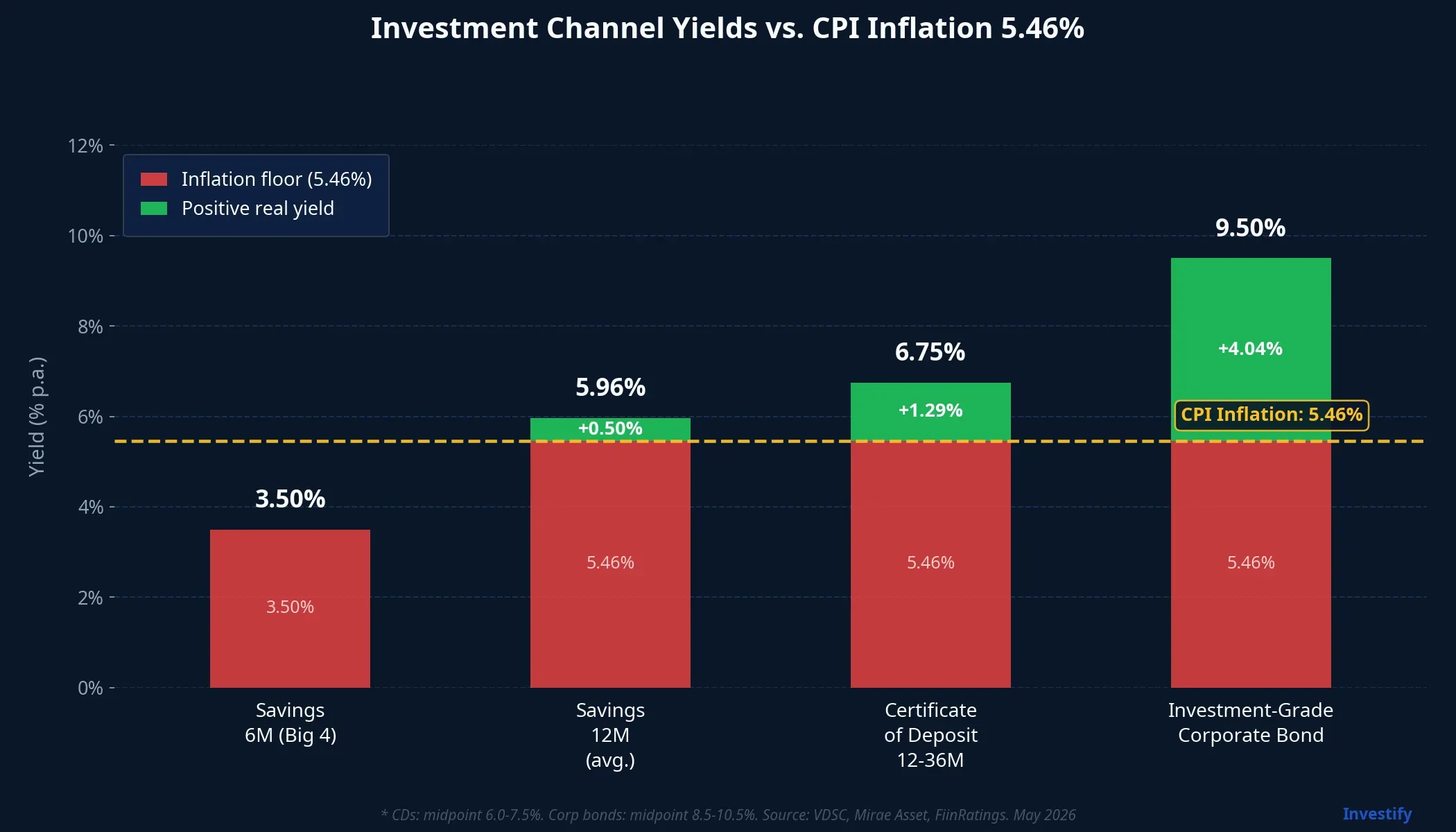

What Channels Still Offer Positive Real Returns?

For individual investors holding cash in an environment where real rates hover around zero, the practical question is: are there alternatives that deliver a positive real return without crossing into high-risk assets like equities?

Fixed-income products sit somewhere in the middle. According to a composite of Q2 money market and bond market reports from VDSC, Mirae Asset, and FiinRatings, certificates of deposit (CDs) at tenors of 12–36 months are widely available at 6.0–7.5% per annum, roughly 0.5–1.5 percentage points above equivalent deposit rates. Investment-grade corporate bonds in sectors like infrastructure, industrial real estate, and major consumer companies are yielding 8.5–10.5% per annum. Against the six-month bank deposit rate, that yield gap is 3–5 percentage points, enough to push real returns into clearly positive territory.

The trade-offs deserve a clear-eyed assessment. Higher yields come with higher credit risk and lower liquidity: CDs and bonds cannot be redeemed on demand the way a savings account can, and corporate bonds are tied directly to the issuing entity’s financial health. A sensible framework in the current environment is to prioritize credit quality and match tenor to actual capital needs — not simply to chase the highest headline yield.

Signals Worth Watching

The core thesis here is clear: real rates in Vietnam are unlikely to recover sustainably as long as U.S. inflation keeps the Fed anchored. The scenario on either side is worth mapping out. If U.S. CPI continues to run hot, a Fed hold through early 2027 is not an implausible outcome; if inflation cools faster than expected, markets will reprice rate-cut expectations and pressure on the USD/VND rate should ease, opening more room for the SBV to act.

Two data points to track in the coming weeks: the next U.S. PCE and core CPI release, and USD/VND rate dynamics as June tends to carry heightened import-demand pressure on the dong. Those numbers will reveal whether the transmission chain running from Washington to Hanoi is tightening further or beginning to loosen.