VSIP’s latest approvals are not just another land-bank headline. The more important signal is that Vietnam’s industrial property story is being re-rated around infrastructure quality, logistics depth and tenant fit rather than raw hectares alone.VietnamBiz

For investors, that changes the framework. In the previous cycle, industrial parks were often discussed in terms of land supply and rental price. In the next one, the sharper question is whether a park can host higher-value tenants that need stable utilities, cleaner operations and faster links to suppliers and export routes.

The expansion says more about network design than land supply

On May 29, 2026, the Vietnam-Singapore Industrial Park joint venture received investment registration certificates for new projects in Hai Phong, Nghe An, Hue, Ha Nam and Ho Chi Minh City. The new approvals lift VSIP’s footprint in Vietnam to 26 projects.Nhan Dan

Read narrowly, that looks like a story about more industrial land. Read geographically, it looks more strategic. Hai Phong sits on the northern port axis, Ha Nam plugs into the Red River Delta supply chain, Nghe An extends room in the north-central corridor, Hue adds a central Vietnam node and Ho Chi Minh City anchors the country’s deepest manufacturing base.

That matters because Vietnam’s FDI push is no longer centered on low-cost capacity alone. The policy direction increasingly favors higher-value manufacturing, cleaner production and supply-chain depth. In that setting, industrial park locations are judged not only by distance to a city center, but by their ability to connect production, labor pools and logistics infrastructure in a way global manufacturers can actually use.

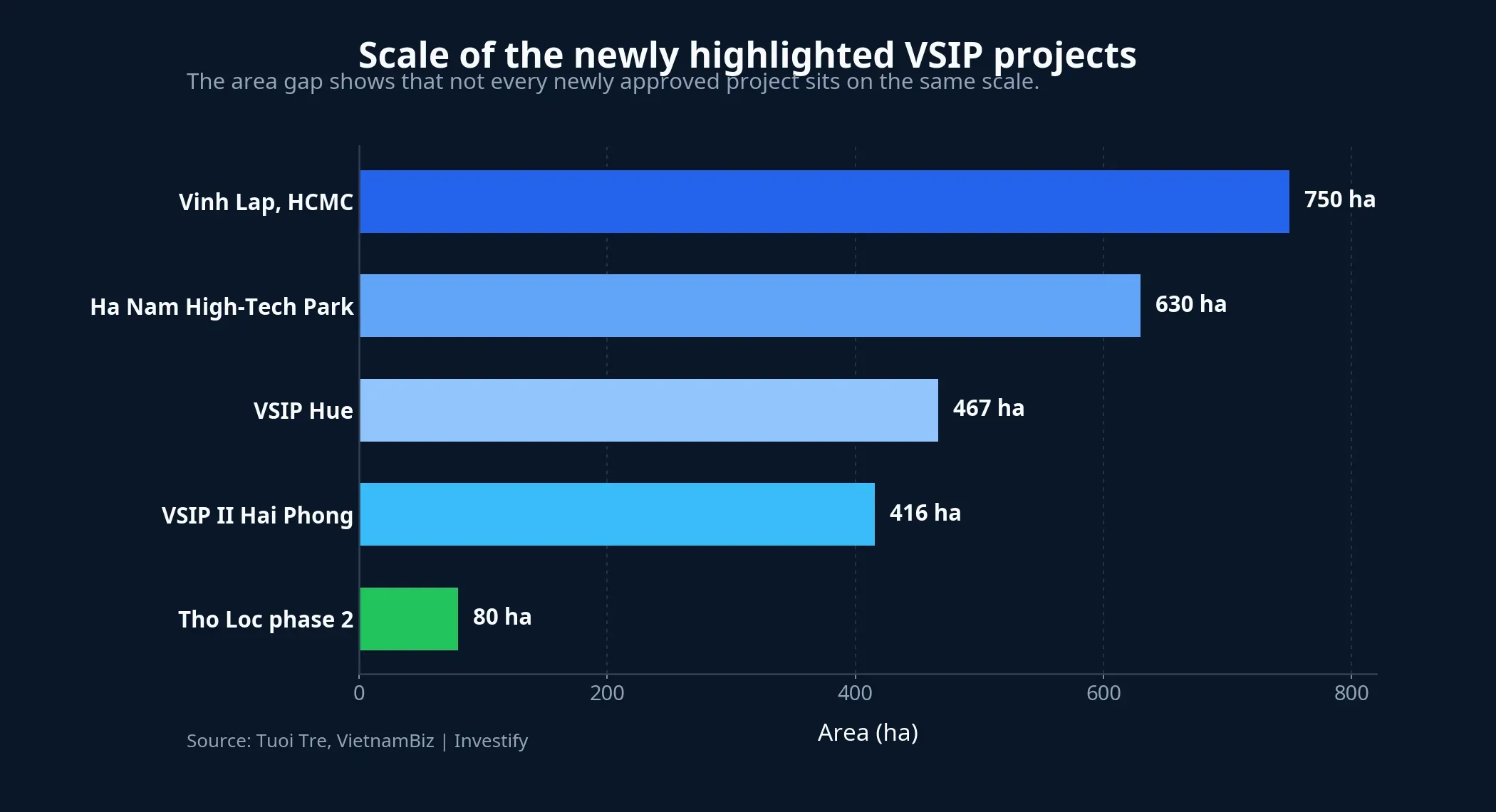

The numbers are large, but hectares are not the full story

Among the projects with disclosed details, Vinh Lap Industrial Park in Ho Chi Minh City spans more than 750 hectares, with phase one alone covering more than 497 hectares. Total investment is set at more than VND 9,700 billion, and the rollout is planned for 2026-2031.Tuoi Tre In Ha Nam, the high-tech park is close to 630 hectares, with investment of nearly USD 230 million and a target tenant mix spanning AI, electronics, semiconductors, biotechnology and new materials.VietnamBiz

Hai Phong was highlighted at roughly 416 hectares under an eco-industrial model, Nghe An’s Tho Loc phase two at nearly 80 hectares, and Hue at around 467 hectares with a greener, smarter positioning.VietnamBiz The spread in project size suggests that each province is being assigned a different role in the next phase of investment attraction.

Markets often flatten all industrial parks into one metric: total area. That works if the only question is how much leasable land may come to market. It breaks down once a project is aimed at semiconductors, electronics or cleaner manufacturing, where the real economic value depends on whether the site is technically ready for capital-intensive tenants to commit.

In practical terms, 100 hectares with stable power, compliant wastewater treatment, strong port access and clean legal status can be worth far more than several hundred hectares still trapped in preparatory work. For newer investors, this is the key distinction between a large land bank and an asset that is actually close to monetization.

A different FDI standard is reshaping the industrial park model

The new projects are not being described like traditional parks that offer only basic land, roads and utilities. The language attached to them leans toward eco-industrial, high-tech, green, smart and research-linked development.Nhan DanVietnamBiz

That is more than branding. Electronics manufacturers, semiconductor firms, precision-equipment makers and data-center operators do not stop at rental price per square meter. They need reliable power, clean water, dependable environmental treatment, resilient logistics and labor markets that can retain engineers, technicians and second-tier suppliers.

Tuoi Tre also reported that Becamex and A*STAR’s Advanced Remanufacturing and Technology Centre signed an MoU to build an advanced manufacturing research center in Vietnam. That detail matters because it points to a newer industrial park model: one that links factories with testing, process improvement and applied research rather than simply clustering plants behind a fence.Tuoi Tre

For experienced investors, this shift has been building for a while, but it is becoming easier to see. The old edge could come from cheaper land or faster absorption. The new edge is increasingly about serving more demanding tenants with larger capital commitments and longer infrastructure requirements.

The upside is real, but it will not be evenly distributed

The most direct beneficiaries remain industrial park developers that can actually execute. Execution here means more than appearing in a plan. It means land clearance, legal completion, infrastructure rollout and tenant acquisition in the right segment. VSIP’s latest batch of projects highlights that standard because the attached tenant profile is materially tougher than the low-cost assembly model of the past.

The secondary beneficiaries are broader: infrastructure contractors, materials suppliers, power, water, environmental treatment, warehousing, ports and transport. Even there, though, the gains will not spread evenly. Companies tied to real transport corridors, signed contracts or visible order flows will look very different from names trading mostly on planning speculation.

The risk sits in the implementation gap. A new approval is only the start of a long chain that includes compensation, site preparation, utility connections, environmental work and tenant onboarding. For higher-tech projects, the bar is even higher, which means larger capital outlays and longer preparation periods.

If the global economy weakens, FDI tenants can still defer leasing decisions or slow expansion plans. In that scenario, the long-term industrial park thesis may remain intact without translating into near-term revenue for every listed company exposed to the theme. That is the difference between a durable investment direction and an earnings result that is about to land.

A better filter for investors

Instead of asking which industrial developer holds the most land, the better question is whether that land is cleared, how far the legal process has advanced, whether power and water capacity can support higher-value tenants, whether the park is connected to ports or expressways, and what tenant mix management is actually targeting. As FDI requirements shift, the investment filter has to shift with them.

The most defensible thesis from VSIP’s latest expansion is that Vietnam’s industrial real estate opportunity remains broad over the next several years, but the gains are likely to favor companies and provinces that can offer integrated infrastructure rather than land alone. Area still matters, just not enough to identify the biggest winners by itself.

The most useful signals to monitor over the next few quarters are infrastructure completion speed, success in attracting higher-value tenants and the depth of supporting industries around each site. If those pieces start to line up, the May 29 approvals will look less like a land headline and more like an early marker of Vietnam’s higher-quality FDI network.