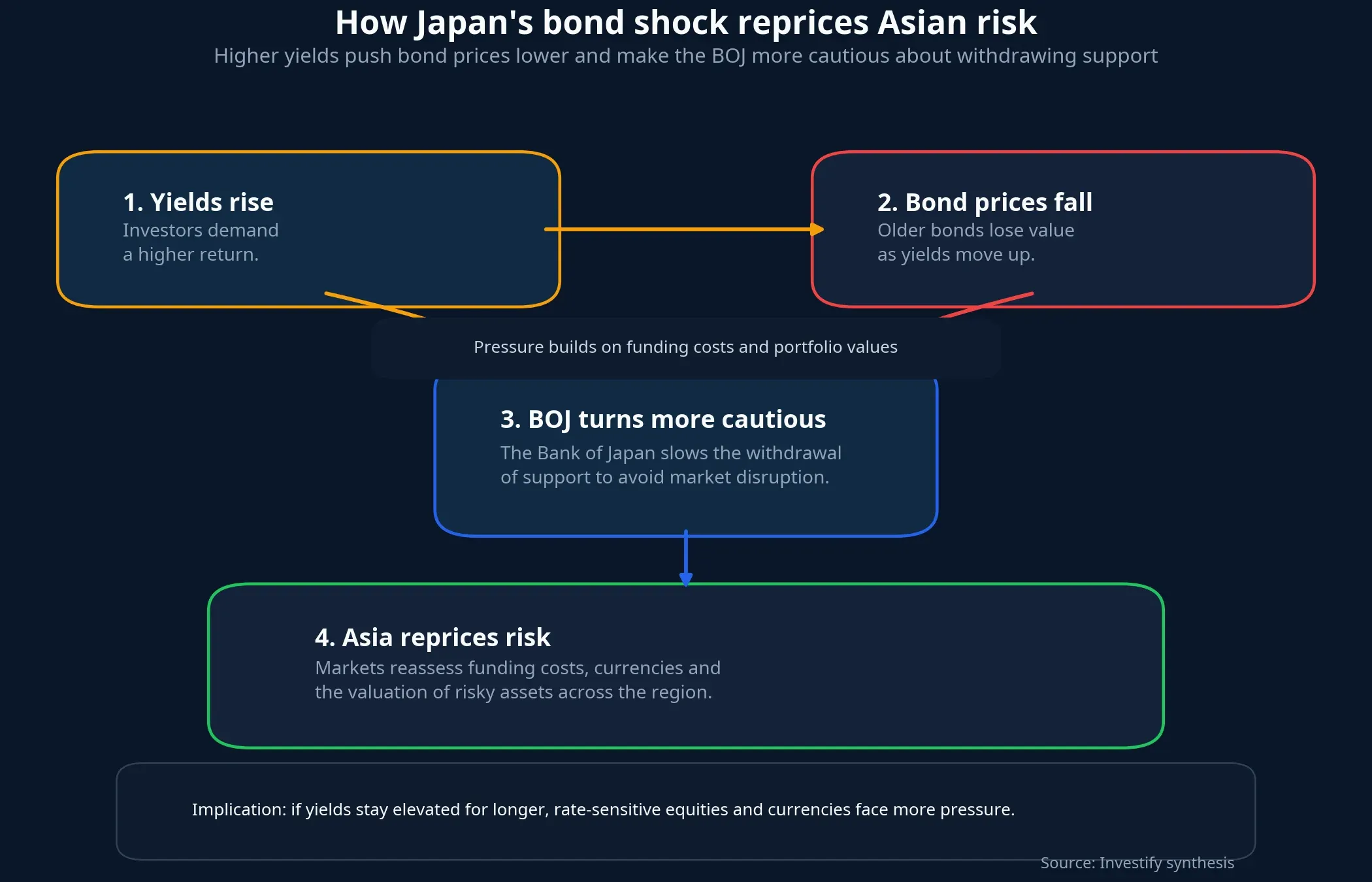

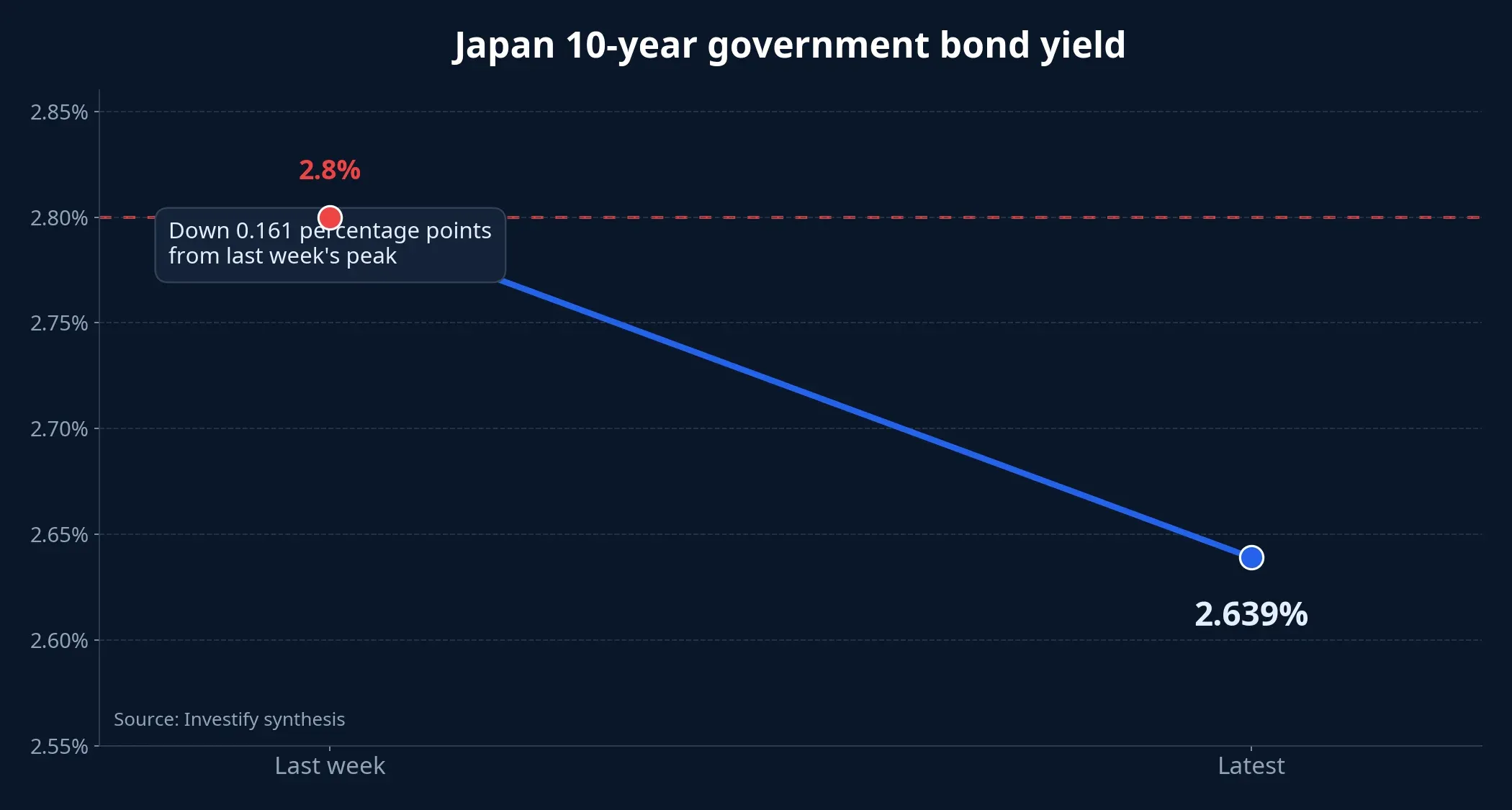

Japan’s government bond market is sending a message that matters well beyond Tokyo. The 10-year yield eased back to 2.639% at the end of last week after touching 2.8% earlier in the week, but the bigger story is not the pullback itself. It is the repricing of capital in one of Asia’s key funding centers, and the growing chance that the Bank of Japan, or BOJ, may need to slow the pace of its exit from market support.Reuters

That signal arrives at a delicate moment for the region. The BOJ will review its bond-buying reduction plan at its June 15-16, 2026 meeting, and Reuters reported on May 29 that bond-market volatility is increasing the odds of a pause or a slower pace of balance-sheet reduction in the next fiscal year.Reuters For newer investors, this is not about comparing Japanese yields directly with a bank deposit or a Vietnamese stock. The larger point is that when a market that spent years exporting cheap money becomes more expensive, risky assets across the region have to justify their valuations again.

Why Japanese bonds suddenly matter more

Japan is a special case in global finance. For years, the BOJ kept financial conditions loose by buying huge quantities of government bonds and holding yields down. Reuters said the BOJ still holds roughly JPY 500 trillion of Japanese government bonds, which means it remains the dominant force in that domestic debt market.Reuters

When a buyer that large starts stepping back, the market has to find a yield level that attracts other pools of capital. That is why a rise in yields is not just a story about falling bond prices. It is the market’s way of saying that the old price of safety no longer clears, and investors now want a higher premium for holding duration.

In that sense, 2.639% is not the most important number. The more important fact is that Japan’s 10-year yield briefly reached 2.8%, pushing into a zone not seen in decades before easing slightly.Reuters A large sovereign bond market does not move like that if investors still believe cheap money is the default setting. When long-end yields jump, the market is testing more than inflation. It is also testing fiscal credibility and the BOJ’s tolerance for instability.

For retail investors, the simplest way to read this is to treat government bonds as the base price of safe money. When that base price rises, equities, property, gold, and currencies all need to adjust, because expected returns on riskier assets have to rise as well.

The BOJ is being pushed toward a slower exit

The BOJ’s problem is the pace of withdrawal. If it cuts bond purchases too quickly, yields could rise further, the Japanese government’s borrowing cost would climb, and the yield curve could become more volatile than policymakers want. If it moves too slowly, the market may conclude that the BOJ is still not ready to leave the era of ultra-cheap money even as inflation pressure remains alive.

That is why the phrase “pause in tapering” matters more than any single daily move. Reuters did not suggest that the BOJ is about to return to the old flood-the-market playbook. What the reporting does suggest is that policymakers may accept a slower path if that is the price of keeping the bond market orderly.Reuters Put differently, the market is forcing the BOJ to acknowledge that policy normalization will not be a straight line.

Why does that matter for the rest of Asia? When a major central bank is pushed into a slower exit because safe yields have risen too far, the signal to the rest of the region is clear: capital is becoming less forgiving. Equities can still rally in the short run if investors think the BOJ will stay soft-handed. Over a longer horizon, though, higher safe yields become a real headwind for valuations, especially in markets that rely heavily on risk appetite.

Three channels Vietnamese investors should watch before the open

The first is the yen. At the end of May 29, USD/JPY stood at 159.31 yen per dollar. If Japanese yields rise while the yen remains weak, the market is telling you this is not yet a clean BOJ regime shift. The policy gap with the United States and the broader appeal of the dollar are still dominating the tape.

The second is dollar strength. At the same time, the DXY index was at 99.02 and USD/VND was at VND 26,332 per dollar. A yield spike in Japan does not automatically move the Vietnamese dong, but it does make the whole region more sensitive to the same question: if the dollar stays firm, are risky assets still attractive enough to hold capital in place?

The third is regional equity performance. On June 1, the Nikkei 225 rose 0.8% while the KOSPI gained 2.8%. That tells you Asian stocks are not in panic mode over Japanese bond volatility. It is also where investors can misread the setup. A green session does not cancel out funding pressure. It simply means the market still believes the BOJ can move slowly enough to avoid a liquidity shock in the near term.

Taken together, those three channels tell a consistent story. The yen is still weak, DXY has not broken down, and Asian equities are still rising. That means the market has not fully shifted into risk-off behavior. But the foundation has changed: safe yields in Japan are higher, and every BOJ decision from here will be scrutinized much more closely.

How to read the signal without overreacting

The common mistake is to see higher yields and conclude that everything has turned negative. In reality, yields can rise for two very different reasons. One is better growth and firmer inflation, which lead markets to price higher rates. The other is a demand for more compensation against fiscal risk and future bond supply. In Japan right now, the evidence suggests both layers are present, but the second one is the reason the BOJ is being pushed toward a slower path.Reuters

That leads to a fairly clear thesis: Japan’s bond market is becoming an early signal for how Asia reprices risk before the trading day begins, even if equity markets are still absorbing the move calmly. Vietnamese investors do not need to trade Japanese government bonds. They do, however, need to respect what this market is saying about capital costs, foreign exchange, and the durability of regional risk appetite.

The key watch list for the first half of June is not one number but three. Does the 10-year yield move back toward 2.8%? Does the BOJ confirm a slower pace of bond-purchase reduction at its June 15-16, 2026 meeting? And does the yen finally strengthen in line with higher yields, or does it stay weak? If those signals start moving together, Vietnam’s market will also have to reassess its own risk baseline.