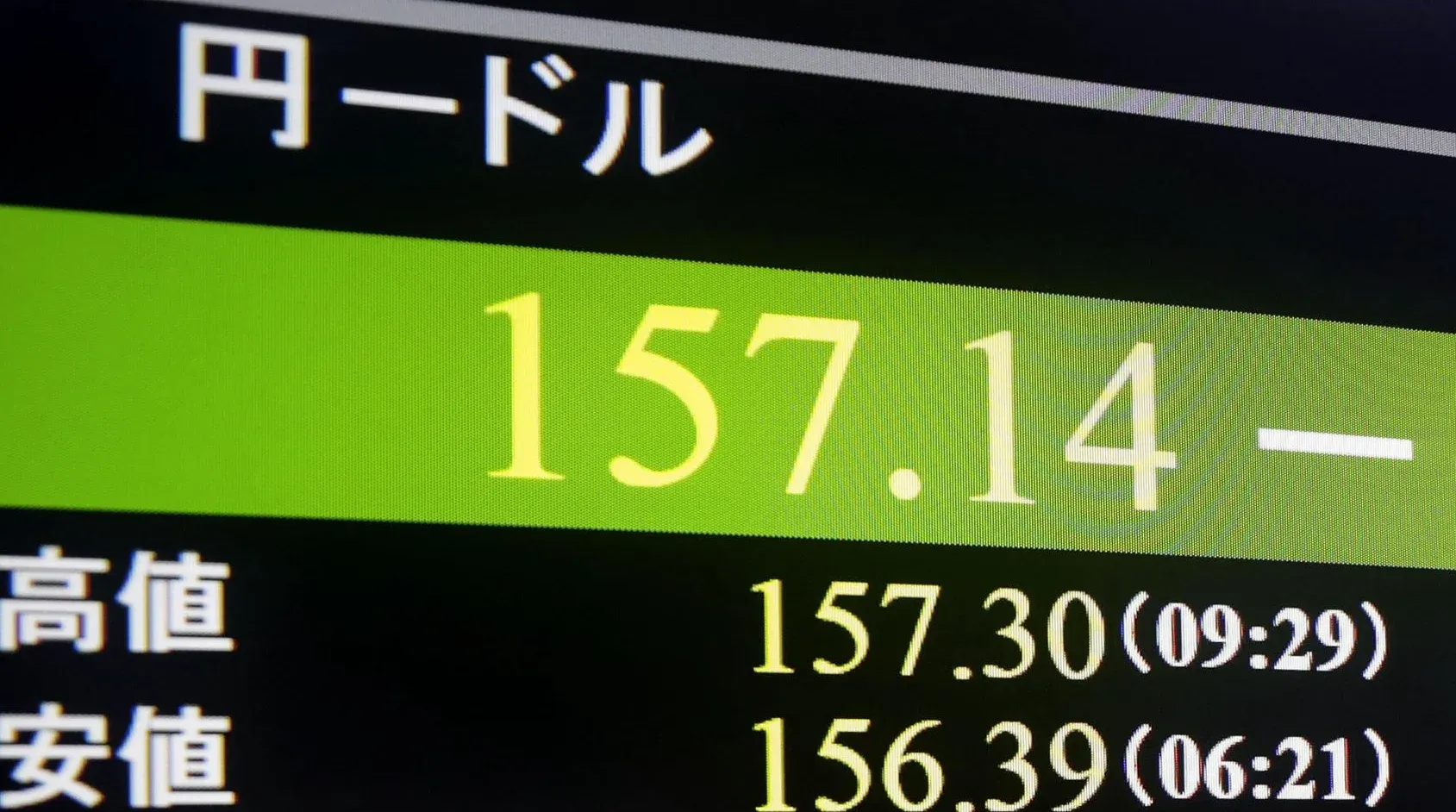

USD/JPY is moving back toward the very zone that previously forced Tokyo to act. That turns 160 into a clear market test: did the latest intervention create a more durable shift for the yen, or did it merely buy Japan a little more time before the old pressures returned.

For Vietnamese readers, this is not a distant foreign-exchange story with no local relevance. The yen acts as an early signal for Asian risk appetite because it sits at the intersection of three large forces: broad dollar strength, imported energy costs and expectations for the Bank of Japan. As long as those three forces have not cooled, 160 matters more than a headline about whether the Nikkei opens up or down.

What 160 really means

The bigger picture is that 160 is not a magical line that automatically changes everything once it is touched. It matters because the level is both psychological and political. This is the zone where traders stop looking only at the chart and start asking how far Japan is willing to go if yen weakness persists.

This time the backdrop is also harder than a simple technical story. If the yen is weakening because US rates are still relatively high, that is already one layer of pressure. If Brent stays elevated at the same time, Japan faces a second squeeze through imported energy costs and inflation. When both forces are present, intervention can trigger a sharp pullback in USD/JPY, but it cannot easily reverse the broader trend on its own.

That is why 160 should be read as a test of policy credibility. If the market believes Tokyo still has both the tools and the resolve to push back, the pair may remain just below that level for a while longer. If speculators conclude that intervention has only short-lived effects, each move back toward 160 becomes another attempt to probe the authorities.

Why a huge intervention was still not enough

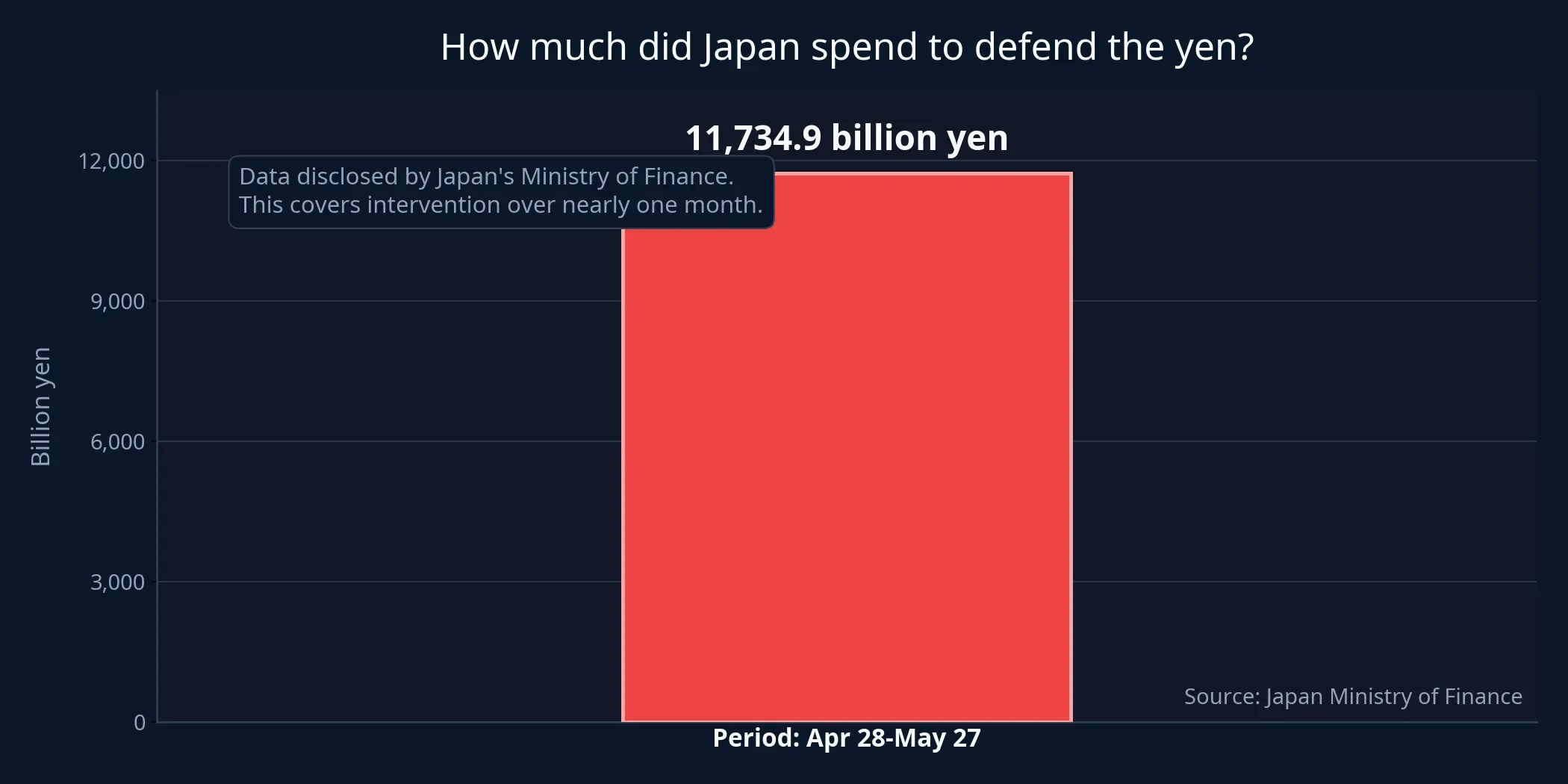

Japan’s Ministry of Finance said total foreign-exchange intervention between April 28 and May 27, 2026 reached JPY 11,734.9 billion.MoF Japan That is large enough to send an unmistakable signal: Tokyo is not prepared to watch the yen slide deeply without responding.

But intervention is fundamentally a braking tool, not an engine of reversal. When the state sells dollars to buy yen, the first impact usually falls on speed and speculative positioning. It can force crowded trades to unwind quickly, yet the deeper story still sits in the US-Japan rate gap and in the energy bill Japan has to import.

That is why the market does not look only at how much money was spent. It also asks what changed afterward in the underlying variables. If US yields do not fall meaningfully, the dollar remains firm and oil does not retreat, pressure on the yen has been delayed rather than removed. That is the point new investors most often miss when they see a headline-sized intervention number and assume the trend must immediately turn.

None of this means intervention is useless. It still matters because it reduces the market’s confidence in one-way speculative bets and gives the BOJ more room to observe conditions before considering a harder move on rates. But if the underlying forces do not shift, intervention will remain tactical rather than strategic.

The three underlying pressures are still there

As of June 2, USD/JPY stood at 159.71, DXY at 99.20 and Brent at USD 94.68 per barrel. Put together, those three numbers describe an environment in which the yen is unlikely to strengthen in a durable way on official buying alone.

USD/JPY sitting just below 160 tells you the market does not really believe the pressure is over. DXY near 99 says the dollar has not lost its broader footing. Brent still close to USD 95 per barrel is a reminder that Japan faces a very concrete problem: the economy imports most of its energy, so a weaker yen in a high-oil environment feeds directly back into inflation expectations and production costs.

This is where the yen story connects to the rest of Asia. When a major regional currency remains under pressure because the dollar is strong and oil is expensive, markets do not read it as a Japan-only issue. They read it as a sign that the regional financial backdrop is still difficult, especially for assets that are sensitive to funding costs and commodity prices.

What investors should watch next

In the short term, the key is not whether USD/JPY touches 160 for a few seconds. The more useful question is whether it can stay above that zone. A move through 160 that holds would suggest the market is willing to test Tokyo’s tolerance further. A quick touch followed by a retreat would suggest that policy signaling still carries weight even without a fresh round of direct intervention.

Investors should also watch three screens instead of one. The first is USD/JPY itself. The second is DXY and US yields, because the yen is unlikely to sustain a recovery if the dollar does not weaken more broadly. The third is Brent, because elevated energy prices make every attempt to stabilize the yen more expensive and less effective.

For Asian equities, the yen signal needs to be read through the breadth of risk appetite rather than through a single index print. A green opening in an equity benchmark does not necessarily say much if the rest of the market trades cautiously. By contrast, if USD/JPY cools, the dollar softens and oil stops climbing, the region has a firmer basis for extending risk-on sentiment across asset classes.

New investors often want a level like 160 to function as a clean yes-or-no answer. Markets rarely work that way. An exchange-rate threshold becomes meaningful only when it is confirmed by the underlying variables. Without that confirmation, it is the beginning of a test, not the end of the story.

Conclusion: 160 is a policy stress test

The clearest conclusion is this: 160 matters not because of the number itself, but because it measures whether Japan’s intervention has bought more than time. As long as the dollar stays relatively strong and oil remains elevated, every return toward 160 will bring the market back to the same question about the yen’s durability.

The practical way to read this is not to react emotionally to a single touch of the level. It is to watch what happens around each approach to 160: does DXY ease, does Brent cool and do expectations for the BOJ change. If those three links do not move, Tokyo is probably still pressing the brakes rather than truly changing the direction of the car.