At a $1.75 trillion target valuation, SpaceX would sit in the same league as some of the world’s largest listed companies even before its shares start trading publicly. But the market is not being asked to buy a finished profit machine. It is being asked to buy a two-layer story: Starlink as the proven cash engine underneath, and Starship, AI infrastructure, and orbital ambitions as the longer-duration layer on top.

For newer investors, this is exactly the kind of deal that can distort the frame. A famous brand, a founder with enormous market pull, and a trillion-dollar headline can make people skip the most basic valuation question: where does the real money come from. The most important thing in SpaceX’s numbers is not that every division has already proven itself. It is that one division has generated enough real cash to support belief in the rest of the story.

What Starlink is actually selling to the market

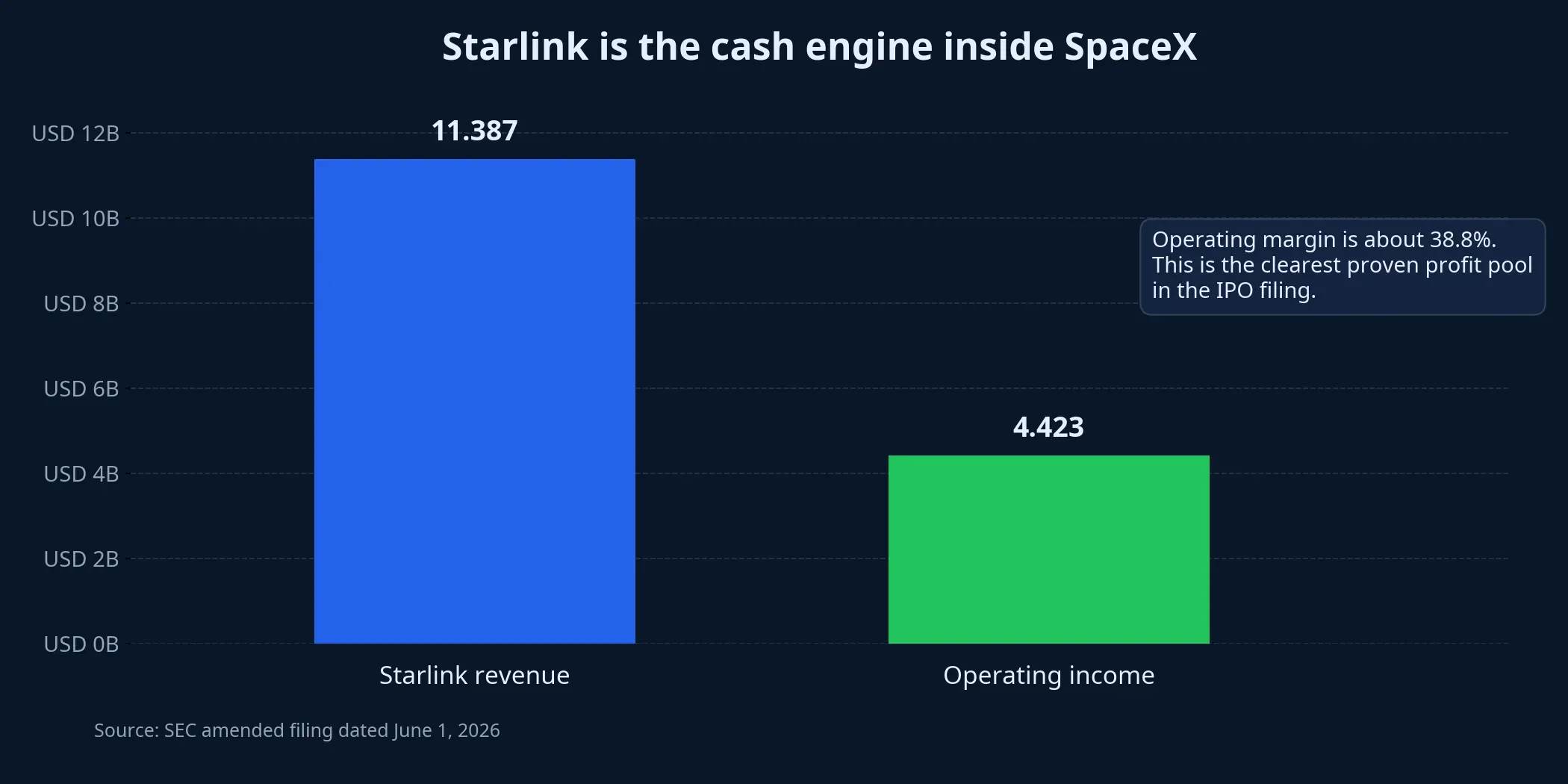

The most important takeaway from SpaceX’s amended SEC filing dated June 1 is that the connectivity segment led by Starlink generated $11.387 billion in revenue and $4.423 billion in operating income in the latest fiscal year. This is no longer a speculative side project or a pure cash-burn growth story. Starlink already looks like a scaled infrastructure business with recurring revenue, meaningful operating leverage, and a moat that is difficult to replicate quickly.

The same filing says Starlink had about 10.3 million subscribers at the end of the latest quarter, while one disclosed subscriber cohort grew 105% from a year earlier. For retail readers, that matters because it separates two ideas that often get blurred together: user growth and narrative growth. In Starlink’s case, the narrative is being supported by a real paying customer base rather than a promise that demand might show up later.

The numbers make it clear why institutional investors are willing to entertain such a high valuation for SpaceX in the first place. A company that can launch its own satellites, own the network in orbit, and sell service directly to end users has a vertically integrated structure that most traditional telecom operators do not. When revenue is generated on infrastructure the company controls end to end, the margin story is fundamentally different from a model built on leased layers of assets.

Why Starlink’s profit does not solve the whole-company equation

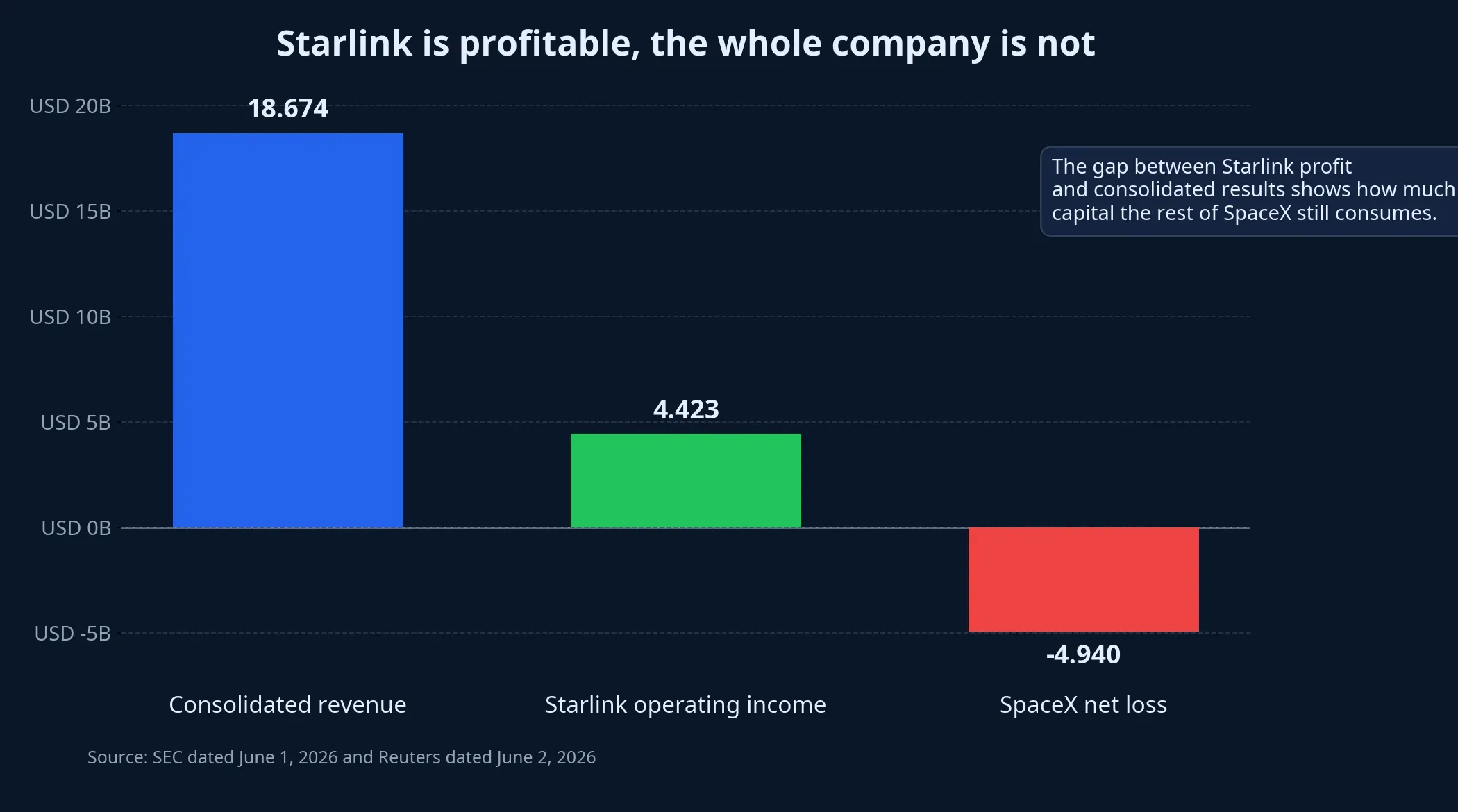

The easy point to miss is that SpaceX’s clearest profit pool does not represent the company as a whole. The same SEC filing shows consolidated revenue of $18.674 billion in the latest fiscal year, while Reuters reported a net loss of $4.94 billion. In plain terms, the profitable part of the business exists alongside a set of projects that still need enormous capital before they can prove their return profile.

That is where first-time investors should slow down. A company with one exceptional segment is not the same thing as a company whose entire valuation is already validated by present-day cash flow. In SpaceX’s case, Starlink may be the profit core, but Starship, launch operations, AI infrastructure, and orbital compute plans are still long-cycle investments that investors are being asked to prepay for.

From a valuation perspective, that makes hypothetical SpaceX stock a hybrid asset. One part looks like a scaled connectivity infrastructure company that has already cleared the product-proof stage. The other part behaves like a long-duration growth option whose value depends on execution speed, cost discipline, and whether the market keeps believing in a far-out future.

Is the $75 billion raise for today’s business or tomorrow’s ambition

Reuters reported that SpaceX is targeting at least $75 billion in IPO proceeds at a $1.75 trillion valuation. Even that single ratio, capital raised versus current revenue, says a lot about the nature of this deal. This is not a routine listing meant to add growth capital around the edges. It looks more like a request to fund the next expansion phase of a company that wants to move far ahead of the point where every business line is already producing mature returns.

Why might the deal still attract demand? Not just because of Starlink. At least three forces are operating at once. The first is scarcity: a rare opportunity to access a private growth asset at enormous scale. The second is the Elon Musk halo. Musk, Chief Executive Officer, Chief Technology Officer, and Chairman of Space Exploration Technologies Corp. (SpaceX), is still viewed by part of the market as someone who can turn allegedly impossible projects into real businesses. The third is the belief that space, satellite connectivity, and AI infrastructure may eventually converge inside a single corporate platform.

Still, evidence and inference need to stay separate. The strongest evidence today is that Starlink has already produced meaningful revenue and operating profit. How much additional value the market assigns to Starship, AI, or orbital data infrastructure remains an open question. Scarcity, brand power, and Musk’s reputation may all help pull valuation higher, but the current data does not let us cleanly apportion how much each factor contributes.

The risks are embedded in the deal structure itself

The first risk is that investors are buying a company whose storytelling capacity is currently broader than the proven earning power of all its moving pieces combined. That does not mean the valuation is automatically wrong. It means the margin for error is much thinner than the glamour around the deal can make it feel. If Starlink keeps compounding, the current valuation framework may become easier to defend. If the rest of the business remains capital-hungry for too long, a very high price tag will be harder to justify.

The second risk is governance. The SEC filing says Class B shares carry 10 votes per share, while Class A shares carry 1 vote per share. The same filing also says that under this structure Musk is expected to retain the ability to control outcomes on matters requiring shareholder approval after the IPO. For public-market investors, that is a major distinction between economic ownership and actual decision-making power.

Many large technology companies have used concentrated voting structures and still created enormous shareholder value. But no filing can decide for investors how much governance concentration they are willing to tolerate. Buying a company like SpaceX is not only a bet on Starlink or Starship. It is also an acceptance that strategic power remains tightly concentrated in a very small circle.

The cleanest way for retail investors to read this deal

The simplest framework is to divide SpaceX into three layers. The first is Starlink, the part with the clearest commercial proof and the strongest cash-flow foundation. The second is the launch and engineering platform that gives SpaceX its strategic edge but is not yet the profit engine in the same way Starlink is. The third is the long-duration layer around Starship, AI, and orbital infrastructure, where valuation error bars remain wide.

If I had to commit to one thesis, it would be the conservative one: $1.75 trillion only makes sense if investors are willing to pay not just for today’s Starlink business but for many years of near-flawless execution beyond it. That thesis does not deny how unusual or powerful SpaceX is. It simply insists that the part already proven by profit and the part still being sold on expectation are not the same thing, even if they are bundled into one price.

The signals worth watching in the next set of documents are concrete: whether Starlink keeps expanding its subscriber base, whether consolidated losses begin to narrow, and what valuation the market is willing to accept for a business with such concentrated voting control. If those answers improve, the valuation story becomes less strained. For now, the main lesson from SpaceX is not how to chase a famous IPO. It is how to separate the cash business from the long-dated dream.