VN-Index ended June 5 at 1,838.90, up 7.35 points from the previous session. On the surface, that looks like a market trying to stabilize after a bruising stretch. But the bigger picture suggests the June 8-12 trading week will not be decided by a small rebound in the benchmark. It will be decided by whether short-term funding conditions and exchange-rate pressure leave enough room for money to rotate back into equities.

This is why the new week should be read as a test of underlying conditions, not just price action. If overnight funding costs stay lower, dollar selling rates at major banks stop tightening and stock-market turnover improves, the rebound can broaden. If one of those links breaks, last week’s bounce will still look more like a pause than the start of a fresh risk-on phase.

Three numbers that matter more than the headline index

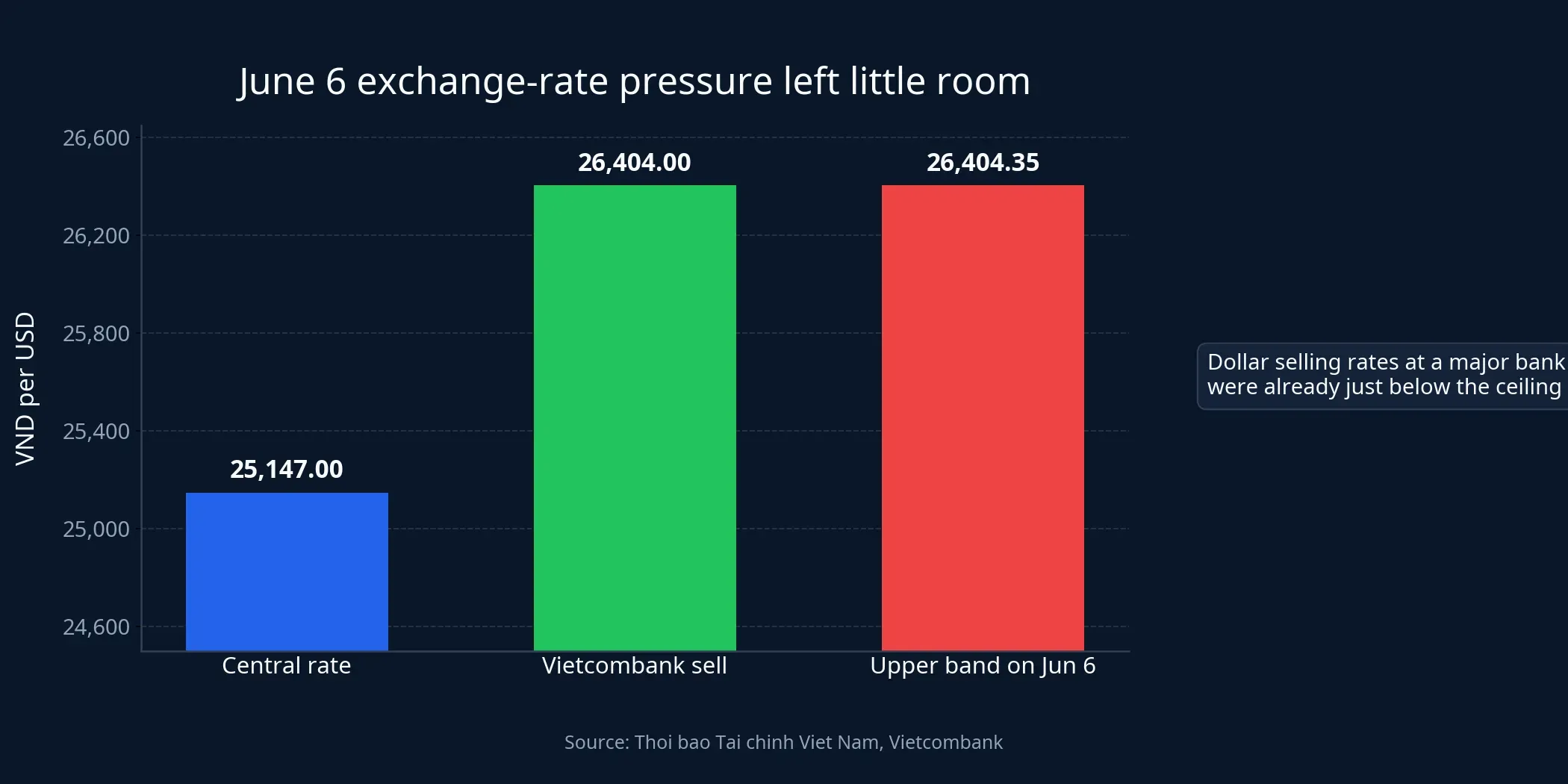

The first number is the exchange rate. By the end of the week, Vietnam’s central exchange rate stood at VND 25,147 per dollar, up VND 9 on the week and marking a fourth straight weekly increase. At the same time, Vietcombank listed the dollar at VND 26,094-26,404, while the official trading band for June 6 ran from VND 23,889.65 to VND 26,404.35.TBTCVN

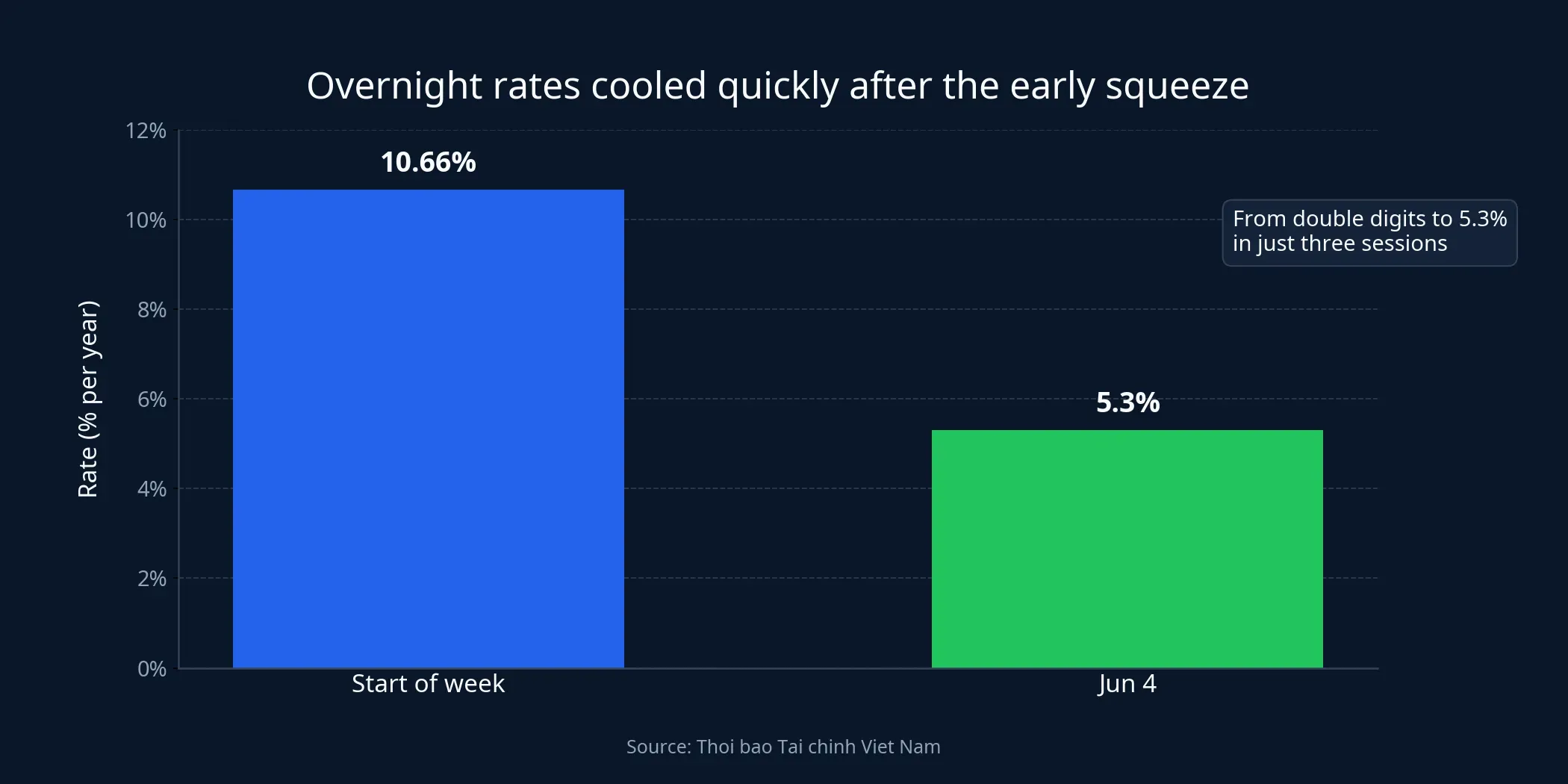

The second number is the overnight interbank rate. For retail investors, that can sound remote from a stock portfolio. In practice, it is one of the fastest signals of stress in the banking system. Early in the week, the overnight rate briefly reached 10.66% per year before easing to 5.3% by June 4, while the one-week tenor fell to 6.2% per year.TBTCVN

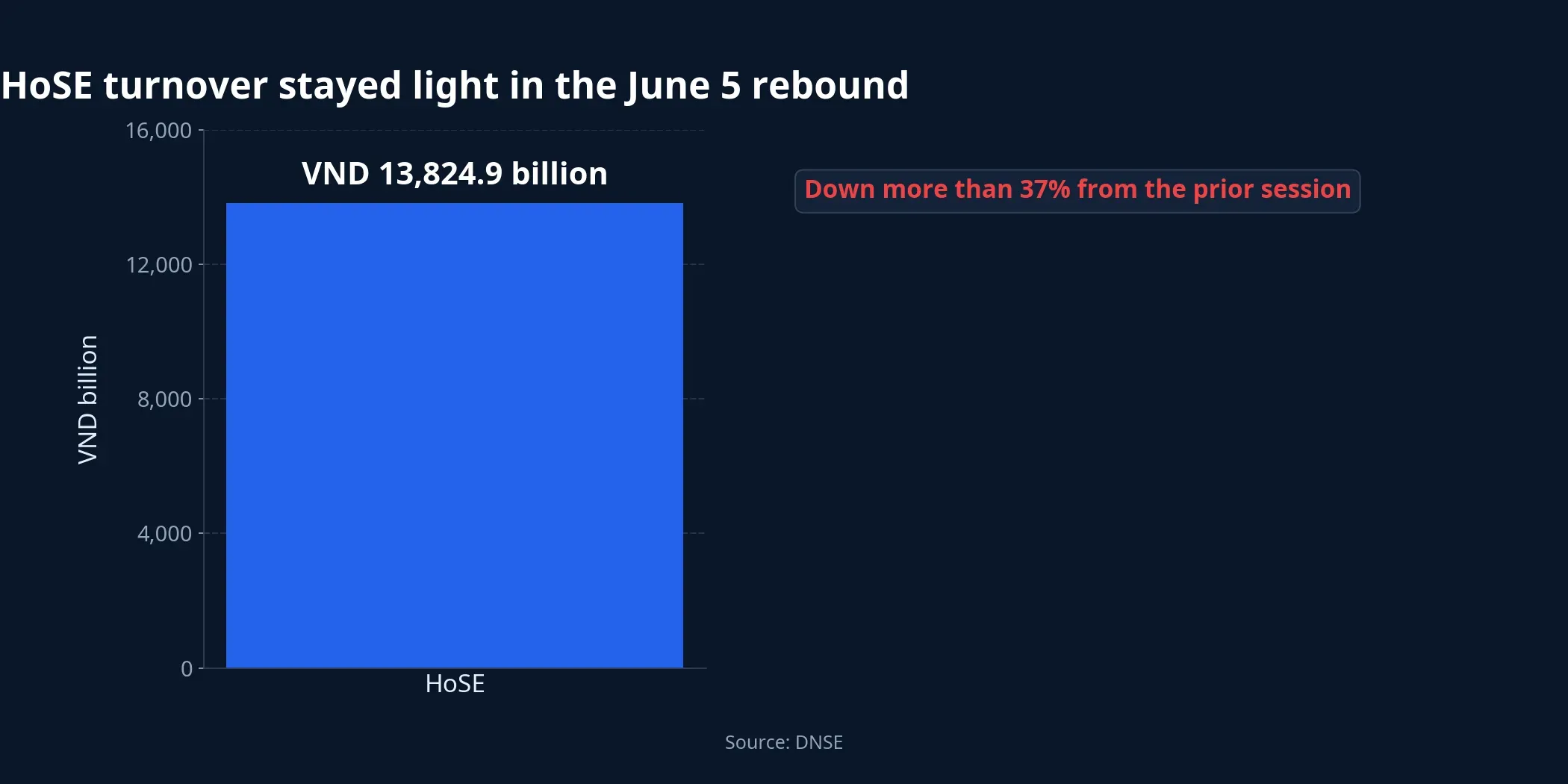

The third number is stock-market liquidity. On June 5, HoSE matched nearly 503 million shares for turnover of VND 13,824.9 billion, down more than 37% in value from the previous session. Market breadth was not especially convincing either, with 95 gainers against 203 decliners on the exchange.DNSE

Put those three data points together and the market looks less comfortable than the index alone suggests. Prices recovered, but liquidity did not confirm. The exchange rate has not turned into a fresh shock, but bank dollar selling rates are already just below the official ceiling. Interbank funding costs came down quickly, yet the market still has to decide whether the early-week squeeze was only temporary.

Why overnight funding costs matter more than the look of the index

The overnight interbank rate matters because it is a live price for short-term dong funding. When that rate jumps, it usually means demand for liquidity inside the banking system has risen sharply. Equity investors feel that before they see it in a quarterly earnings report, because tighter money changes how the market prices risk almost immediately.

The first sectors to react are usually the ones most sensitive to funding conditions: banks, brokerages, property developers and companies that rely heavily on working capital. In those areas, valuations do not only reflect current earnings. They also reflect confidence that funding will remain available at a cost compatible with future growth. When short-term rates move into double digits, investors start demanding a higher risk premium.

What stood out last week was not a one-way policy stance from the State Bank of Vietnam. According to Thời báo Tài chính Việt Nam, the SBV injected VND 13,619.46 billion on June 1 before shifting back to net withdrawals, leaving total weekly net absorption at VND 26,372.11 billion via open-market operations.TBTCVN The cleaner reading is that the central bank was responding to changing liquidity pressure in real time, not signaling a simple easing or tightening narrative.

That makes the coming week less about a single policy headline and more about day-by-day confirmation. If overnight rates stay anchored near the lower level reached on June 4, investors can treat the squeeze as noise. If they rebound sharply, every recovery story in equities will have to trade through another layer of discounting.

The friendlier scenario for equities

The bullish case does not require the exchange rate to reverse lower in dramatic fashion. It only requires the pressure to stop building. If the central rate moves in a narrow range, bank dollar selling rates do not tighten further and overnight funding costs remain well below last week’s 10.66% spike, money can begin rotating back into sectors that were hit hardest by funding worries.

Brokerages tend to respond first in that environment because trading liquidity is their most direct earnings lever. When investors feel less stressed about the monetary backdrop, they are usually more willing to re-engage with securities firms, margin-linked names and other businesses that benefit from a faster circulation of capital. Banks can also recover, but only if the market believes short-term liquidity pressure is no longer squeezing margin expectations.

Property and construction-material names could also stabilize, though their recovery would still be conditional. Those sectors need a less hostile funding backdrop before sentiment can improve in a lasting way. If the index rises but turnover stays thin, rallies in these groups are unlikely to travel far because buyers will stay selective and quick to step back.

The more likely middle ground

This is probably the scenario worth taking most seriously. Exchange-rate pressure stops getting worse, interbank rates stay out of the danger zone, but stock-market turnover remains weak. In that setting, the market does not fall apart, but it also lacks the energy for a broad-based risk rally.

When that happens, money usually sorts companies by balance-sheet quality rather than by crowd enthusiasm. Businesses with lower short-term debt burdens, steadier operating cash flow and stronger pricing power tend to hold up better. By contrast, long-duration growth stories often lag because investors are not yet willing to pay aggressively for earnings that sit far out in the future.

One common mistake is to assume that a slightly weaker dong automatically benefits all exporters. That is too broad. A company earning dollar revenue can still see limited upside if it also imports dollar-priced inputs, borrows in dollars or operates on thin margins. The exchange rate is one variable in the profit equation, not a shortcut to sector-wide winners.

The harder scenario starts with the U.S.

Outside Vietnam, the U.S. jobs report released on June 5 showed that the economy added 172,000 jobs in May, far above the 80,000 consensus estimate, while the unemployment rate held at 4.3%.Kiplinger That report does not mean the Federal Reserve is about to hike rates, but it does weaken the case for early cuts.

For Vietnam, the key transmission channel is not an immediate Fed decision. It is the interest-rate gap and the pressure involved in keeping the dong stable. If the dollar stays firm globally, or if the market keeps pushing back the expected timing of Fed easing, exchange-rate pressure at home becomes harder to relieve quickly. That is why the exchange rate and interbank liquidity need to be read together rather than in isolation.

If that harder scenario gains traction this week, long-duration growth stocks, property names, brokerages and heavily short-funded businesses are the ones most likely to face additional valuation pressure. Not because next quarter’s earnings suddenly collapse, but because investors become less willing to pay up for profits that are still far away.

The three signals to watch each day

The first signal is the overnight interbank rate. If it remains meaningfully below last week’s early spike, concerns about system liquidity should fade quickly. That is the minimum condition for money to move back into rate-sensitive sectors.

The second signal is the dollar selling rate at major banks. If it stays around VND 26,404 without being pushed tighter by further moves in the central rate, the market can still treat the situation as pressured but manageable.TBTCVN If bank dollar quotes keep hugging the ceiling for several sessions, risk appetite will be slower to recover.

The third signal is equity-market liquidity. A green session with only about VND 13,824.9 billion in HoSE turnover is not enough to say money is back.DNSE What the market needs is a sequence of stronger value traded sessions, with breadth no longer skewed so heavily toward decliners. Only then does a rebound start to look properly funded.

The cleanest thesis for June 8-12 is straightforward: last week’s rise in VN-Index was not enough to confirm a new risk-on phase. Capital flows still depend on three conditions happening together: overnight rates must stay down, bank dollar pressure must stop tightening and stock-market liquidity must improve. U.S. data and exchange-rate pressure remain real risks, but they do not overturn that view unless those three signals deteriorate together again. In other words, the number worth watching this week is not the prettiest index level on the screen. It is the quality of money standing behind it.