Oil is not staying high because the market ignored OPEC+. If anything, traders heard the message clearly and still refused to relax. The real issue is whether barrels can leave the Gulf, secure insurance, and reach buyers on time. Until that confidence returns, every quota increase only softens the fear at the margin. It does not remove the geopolitical premium embedded in crude.

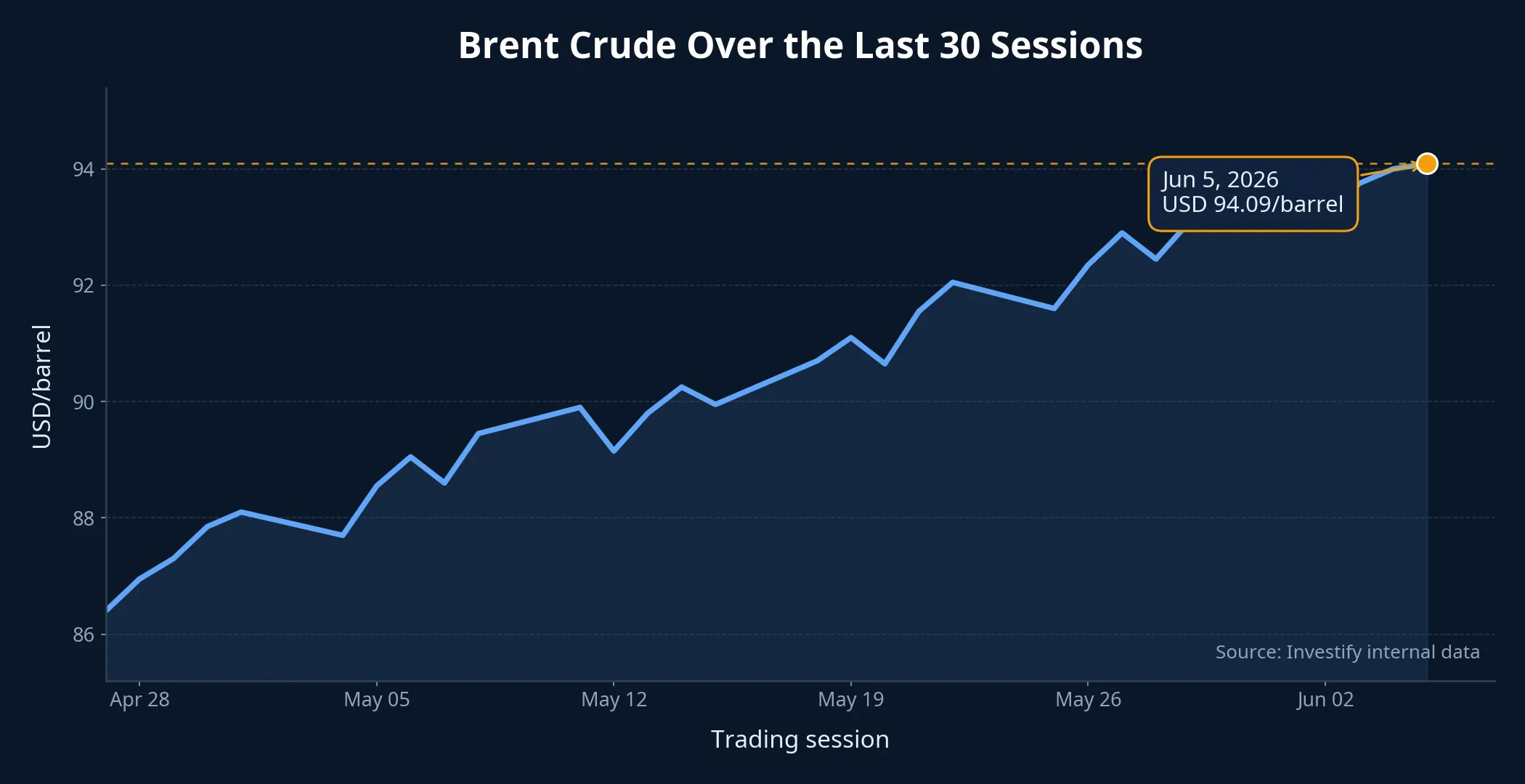

On June 7, the seven core OPEC+ members, Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria and Oman, agreed to raise July 2026 output by 188,000 barrels per day.OPEC In a cleaner market, that would usually pressure prices lower. Yet Brent settled at USD 94.09 per barrel on June 5, up 3.3% from USD 91.12 on May 29 and roughly 54.9% above its early-year level. The broader picture is straightforward: the market is not treating this as a normal supply response.

Quotas Are Not the Same as Usable Supply

That distinction matters more than it sounds. OPEC+ can authorize more production, but refiners and traders only care about oil that is actually pumped, loaded, shipped and delivered safely. If even one part of that chain is impaired, nominal supply is not the same as effective supply.

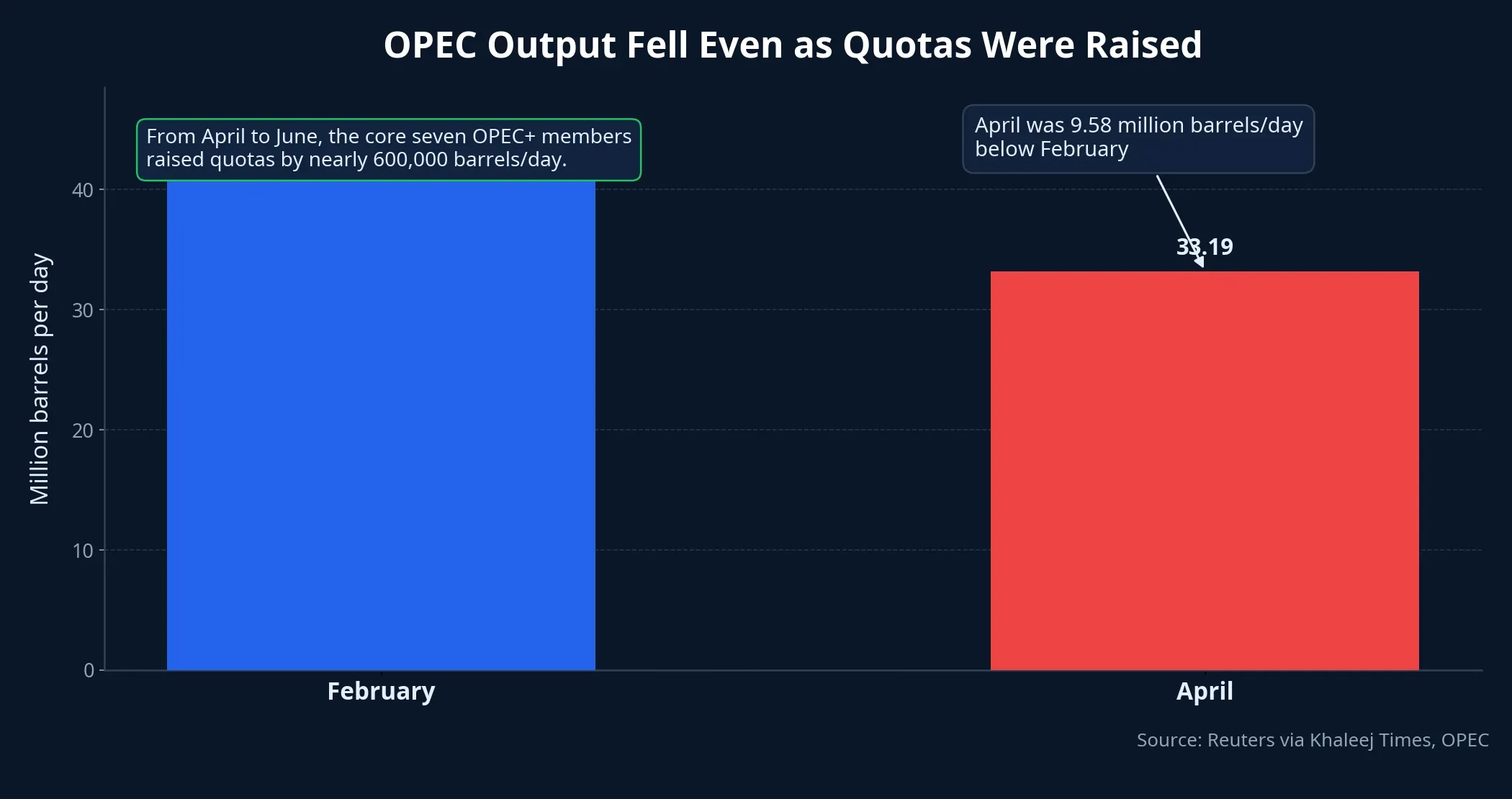

Reuters, cited by Khaleej Times, reported that the seven-country group lifted quotas by nearly 600,000 barrels per day from April through June.Khaleej Times The same report also cited OPEC data showing average group output fell to 33.19 million barrels per day in April from 42.77 million in February.Khaleej Times That gap is the market’s real headline. Quotas moved up. Actual supply, at least in the reported data, moved the other way.

For investors, this changes how the news should be read. A quota increase is first-order information. Actual physical flow is second-order information, and second-order information often matters more for price. If the physical market still looks unreliable, Brent can remain firm even when policymakers and producers are trying to sound reassuring.

Hormuz Is Where the Market Is Taking Its Cue

The current stress point is the Strait of Hormuz, not the OPEC+ communiqué itself. CafeF reported on June 7 that the US-Iran diplomatic track remains uneven, while Iran still wants to preserve influence over Hormuz rather than restore the route to a fully normal operating state.CafeF In oil markets, “not fully normal” is already enough to keep risk premium in place.

This is why traders do not need a total shutdown scenario to stay defensive. Shipping disruptions can start well before that point. Tanker operators may rethink routes, buyers may demand wider delivery buffers, and logistics providers may build in extra protection costs. The shock does not have to be absolute. It only has to be serious enough to slow the rhythm of physical movement.

It is also worth being disciplined about causality. High oil prices today could reflect several overlapping forces: concerns over physical supply, a geopolitical risk premium, hedging activity in commodity markets, and broader defensive positioning across financial assets. Of those explanations, the strongest evidence currently supports the physical-flow argument. Quotas have risen, actual output has fallen, and diplomacy around Hormuz still has not convinced the market to remove its safety margin.

The Impact for Vietnamese Investors Goes Beyond Oil Producers

The instinctive trade is to see Brent rise and jump straight to oil and gas equities. That instinct is understandable, but it is incomplete. Oil is an input for airlines, transport, chemicals, plastics, logistics and, eventually, inflation expectations. If crude stays high for long enough, the effect spreads far beyond one industry group.

In the near term, Vietnamese retail fuel prices do not move in lockstep with Brent every day. Investify internal data show E5 RON92 gasoline at VND 21,780 per liter on June 4, down from VND 23,250 on May 28. Diesel 0.001S-V was VND 28,120 per liter on the same date, also below VND 28,910 a week earlier. That means investors should not assume a one-week move in Brent instantly translates into a one-week squeeze on every fuel-consuming business.

But the picture changes if Brent stays elevated. Once companies start budgeting around more expensive fuel, the issue shifts from short-term volatility to real cost pressure. Airlines, trucking operators and other fuel-sensitive sectors then have to reassess margins. At that stage, the better question is not which stock “wins” from higher oil, but which industries can absorb higher input costs more effectively.

From a macro perspective, higher oil also keeps another concern alive: inflation may not cool as quickly as the market hoped. If investors start to believe energy prices will remain high for longer, bond yields, rate expectations and the valuation of growth-sensitive equities all come under pressure. For newer investors, this is usually the most overlooked layer because it does not show up as clearly on the screen as a sharp move in oil names.

Higher Oil Does Not Automatically Mean a Simple Trade

The cleaner framework is to separate the story into three layers. First, OPEC+ is trying to add supply on paper, which should be price-negative in theory. Second, actual output data still suggest the market is not seeing enough real barrels. Third, the security and diplomatic backdrop around Hormuz remains unstable enough to preserve a risk premium.

Once those layers are separated, investors are less likely to fall into one-direction thinking. Oil producers may benefit in some stretches, but fuel-intensive sectors face the opposite pressure at the same time. The broader market also has to reprice the odds of firmer inflation and a slower decline in interest rates. Capital therefore does not move in a straight line. It rotates across sectors based on who can absorb the shock and who cannot.

The core thesis is simple: oil is not currently being priced off the slogan that OPEC+ is adding supply. It is being priced off a tougher question, whether physical crude can move through Hormuz on something close to a normal schedule. Until actual output improves and transport risk eases, Brent is likely to retain part of its geopolitical premium. The most useful signals to watch over the next one to two weeks are OPEC’s realized production, the diplomatic backdrop around Hormuz, and how bond markets react to renewed inflation risk.