What Vingroup gave the market on June 8 was not a completed capital transfer. The group was granted the right to receive transferred stakes from Pham Nhat Vuong, Chairman of Vingroup (VIC), and related parties, lifting its interest in companies tied to GSM and VinEnergo to as much as 35%.Người Lao Động

The key phrase is “granted the right,” not “has acquired.” That right gives Vingroup a reserved lane to pull more value from electric transport and energy assets back into the listed parent, while stopping short of forcing an immediate cash outlay on announcement day.DNSE

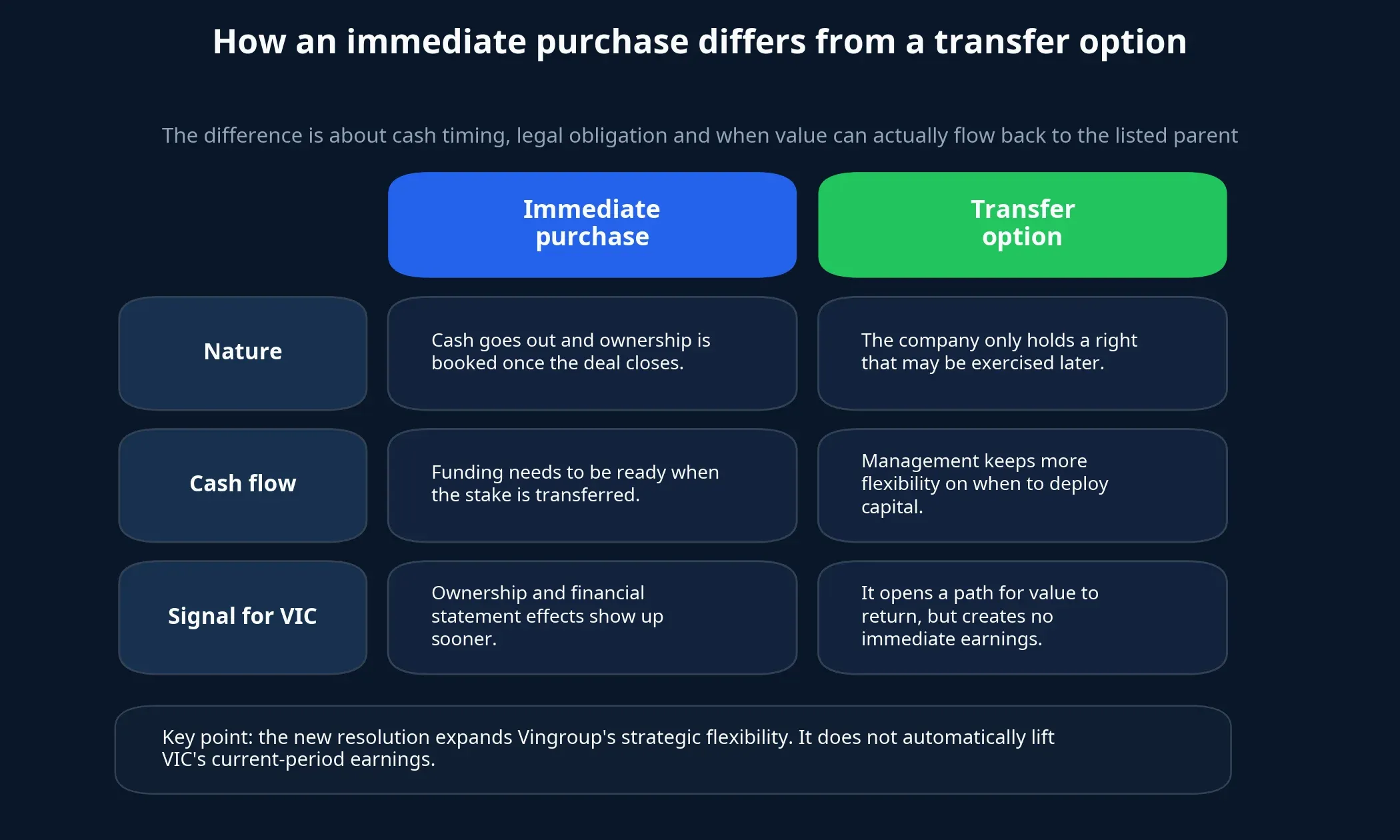

For newer investors, that distinction matters. An outright purchase is about cash leaving the company, ownership being booked and the financial statements changing soon after. A transfer option is about structure. Vingroup is preserving room to act later in an ecosystem where value does not automatically flow to VIC simply because the businesses sit under the same broader umbrella.

What the approved right actually covers

Under the June 8 resolution, Vingroup may receive preferred shares equal to a planned 29.99% stake in GSM VN Holding and 30% in Smart & Green Trans Limited, or SGT. On the energy side, it may receive preferred shares equal to a planned 16.01% stake in VinEnergo Holding and 16% in G-Energo Limited.Người Lao Động

The structure is broad, but it is still framed by a maximum interest ceiling of 35%. In other words, Vingroup is not saying it wants to bring all of the value from those businesses directly onto its own books. It is reserving a meaningful enough level of participation so that, if the timing becomes attractive, incremental value can move back to the listed parent through a mechanism already set up in advance.

If a transfer happens, the price will be based on the transferor’s contributed cost. The transaction must also be completed before SGT and G-Energo list, within a maximum of 36 months from the signing date of the relevant contracts.Người Lao Động Put plainly, the resolution creates a lane for Vingroup to act before a new funding or listing milestone, rather than declaring that the action has already taken place.

Why VIC investors should care

If investors focus only on short-term price action, they can miss the more important point. VIC is the listed parent, so the real question is not just whether the wider Vin ecosystem expands. The bigger question is whether that expansion leaves a clear enough footprint at the Vingroup level for public shareholders to benefit from it.

GSM sits in the operating layer of the electric mobility story. VinEnergo sits in the energy layer, the part of the ecosystem that could matter more over a multi-year electric vehicle build-out. By securing a right to increase its interest in both, Vingroup is showing the market that it wants to retain an option for value created in those newer growth nodes to sit closer to the listed parent rather than entirely outside it.

There are at least two reasonable ways to read this. One is that Vingroup is preparing for a deeper role in entities that could become more important as the electric vehicle ecosystem matures. The other is that management mainly wants capital flexibility in case SGT and G-Energo approach listing or valuation milestones under more favorable conditions. The current evidence is not strong enough to prove which view will dominate, but the resolution does show that management chose to keep the option on its side instead of letting that door close.

That point matters when you read financial statements. Ecosystem value only matters directly to VIC shareholders when ownership is clear enough, dividends or gains can flow upstream, or consolidated earnings start to reflect those positions. Without those links, investors may still see an appealing growth story around Vingroup, but not necessarily one that translates into economic benefit for the listed parent.

How this differs from an immediate stake purchase

A completed capital purchase usually brings three things at once: a payment obligation, a change in ownership, and the potential for accounting effects to show up in subsequent reporting periods. This case is still at a different stage. Vingroup has been granted the right, but it is not required to take the transfer, so as of the announcement the group has no transfer payment to make.DNSE

That changes how the market should read the news. If the purchase had already closed, the conversation would quickly move to funding, book value and whether the new ownership mix changes consolidated earnings. Because this is still a transfer option, the emphasis shifts elsewhere. Vingroup is buying strategic flexibility, not booking a new asset into the accounts right away.

For retail readers, a simple comparison helps. An immediate purchase is like signing the final contract and wiring money for an apartment. A transfer option is more like securing the unit with terms in place while waiting for the right moment to complete the last step. The value of that reserved lane is optionality, not immediate cash flow.

VIC’s one-day drop does not tell the whole story

On June 8, VIC closed at VND 196,700 per share, down 4.98%. Its market capitalization was roughly VND 1,515.8 trillion. The VN-Index fell 48.37 points in the same session, or 2.63%.

Those numbers point to an important caution. VIC’s decline that day should not be assigned directly to the new resolution. This is where counterfactual discipline matters. The same price outcome can be explained by several competing drivers, from the broader market sell-off and pressure on large-cap names to the way investors processed company-specific news. The evidence currently supports a narrower claim: the June 8 resolution helps investors understand Vingroup’s longer-term value structure better, but it does not prove that the one-session move was caused by this announcement.

That is also why the next checkpoint should not be whether VIC rebounds in the following session. The more useful watch list is concrete: whether Vingroup exercises the right, whether the final ownership percentages stay close to the current framework, how contributed cost is determined, and how close SGT and G-Energo move toward listing. Only when those pieces start to shift does today’s reserved option begin turning into recorded value for the future.

The real thesis is about value architecture

The most important takeaway from the June 8 resolution is not a short-term earnings catalyst. It is the way Vingroup is arranging the right to benefit from its own ecosystem. By reserving the ability to raise its interest in the GSM and VinEnergo groups, the company is trying to keep future growth at those newer nodes from drifting too far away from the listed parent.

That thesis still comes with a condition. If the right is never exercised, the resolution mostly reflects higher flexibility in capital structure. If the right is exercised before SGT and G-Energo list, the debate moves to harder but more meaningful questions: how much cash goes out, how the new ownership is booked, and whether VIC shareholders actually gain a more tangible claim on the growth of those businesses.

The cleanest conclusion for now is this: Vingroup has opened a route through which value may return to VIC, but that route does not create earnings in the current period by itself. The signals worth tracking in upcoming quarters are the exercise decision, the pre-listing conditions attached to SGT and G-Energo, and the footprint those changes eventually leave on Vingroup’s consolidated financial statements.