For many first-time investors, airline stocks look easy to read. Summer demand rises, airlines add routes, aircraft utilization improves, and revenue follows. But that only covers half the story. The other half is cost, and in aviation, cost is often what changes the market’s tone fastest.

On June 5, VJC closed limit-up at VND 184,600 per share, with matched volume above 3 million shares. Znews noted that the move pushed the stock to its highest level in more than three months.VietnambizZnews On the surface, that session confirmed that the market is still willing to pay up for Vietjet’s recovery story. But heading into the new week, the more important variable is no longer passenger demand or route expansion. It is jet fuel.

What exactly is the market pricing into VJC?

At a basic level, stocks do not rise simply because a business is “doing better.” They rise because the market believes that improvement can continue for several more quarters. For VJC, at least three separate expectations seem to be stacked on top of each other right now.

The first is the stock dividend story. Vietjet has finalized the shareholder record date for a 30% stock dividend, equivalent to nearly 178 million new shares.Vietnambiz A stock dividend does not put cash into investors’ accounts immediately, but it often draws short-term attention because it signals that the company is confident enough to distribute accumulated earnings in equity form.

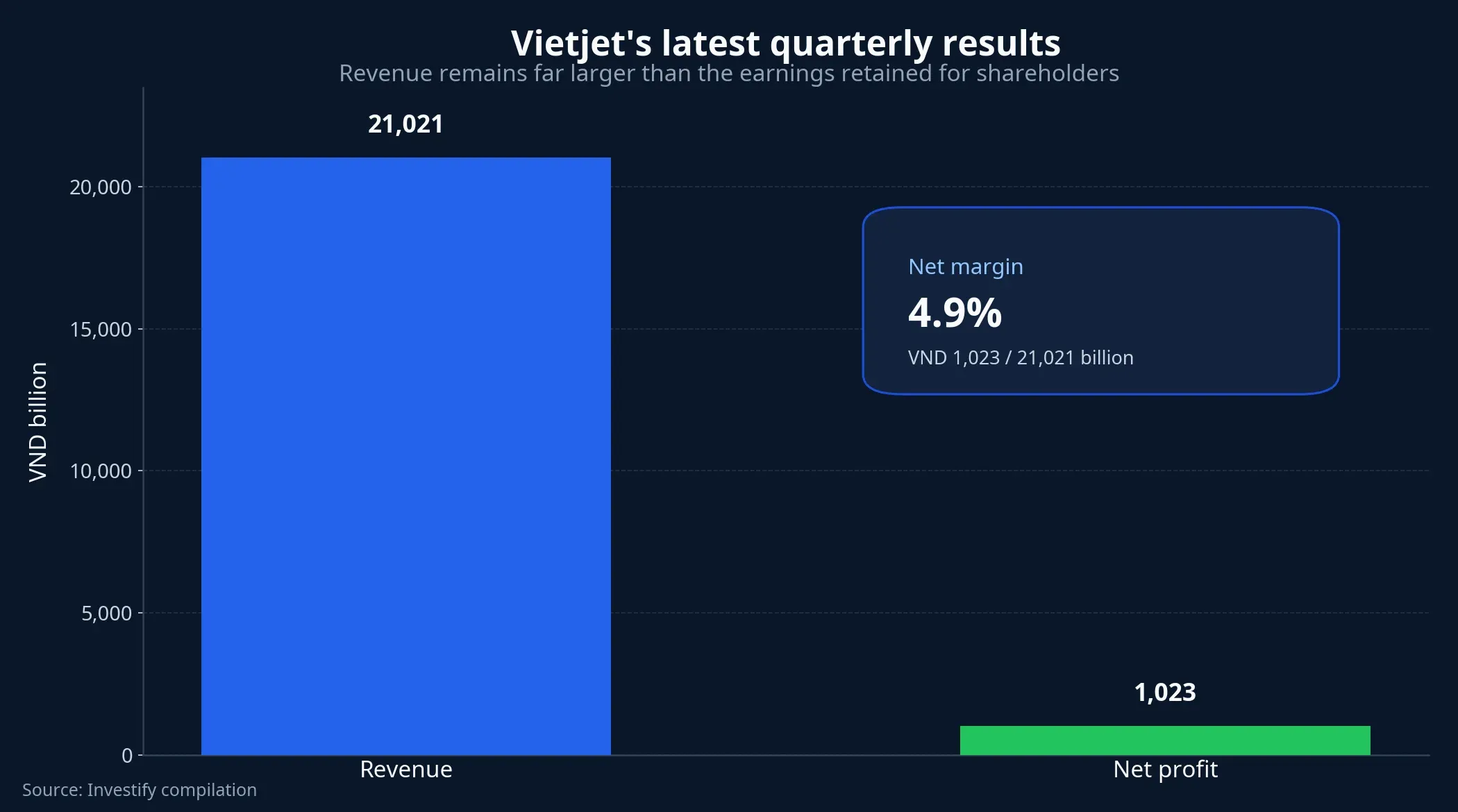

The second is the latest quarterly result. Vietjet posted VND 21,021 billion in revenue for the first quarter of 2026, up 17% year over year. Net profit reached VND 1,023 billion, up 59% from the first quarter of 2025.Vietnambiz For newer investors, the key point is straightforward: the market does not stop at revenue. It cares about how much of that revenue still remains for shareholders after costs are absorbed.

The third is operating momentum. In the first three months of the year, the airline ran around 39,903 flights, served 7.2 million passengers, and transported 23,344 tons of cargo.Vietnambiz Those figures suggest that demand is not the main problem for Vietjet at this stage. When traffic and activity are still expanding, the market has a reasonable basis for assuming that revenue growth is not over yet.

The important discipline point is this: there is not enough evidence to claim that VJC’s jump came from one single catalyst. The stock dividend, first-quarter earnings, peak summer expectations, and short-term positioning may all have contributed at the same time. A cleaner reading is that VJC is benefiting from several overlapping expectations, not that one headline alone fully explains the move.

Why airline stocks are always so exposed to fuel costs

Put simply, airlines sell seats in advance but carry a large part of their cost structure early. Flight schedules are already set, aircraft leases are already in place, crews have already been arranged, and route networks cannot be resized overnight just because input prices move for a few sessions. That is why rising fuel usually hits margins faster than airlines can pass the increase through to ticket prices.

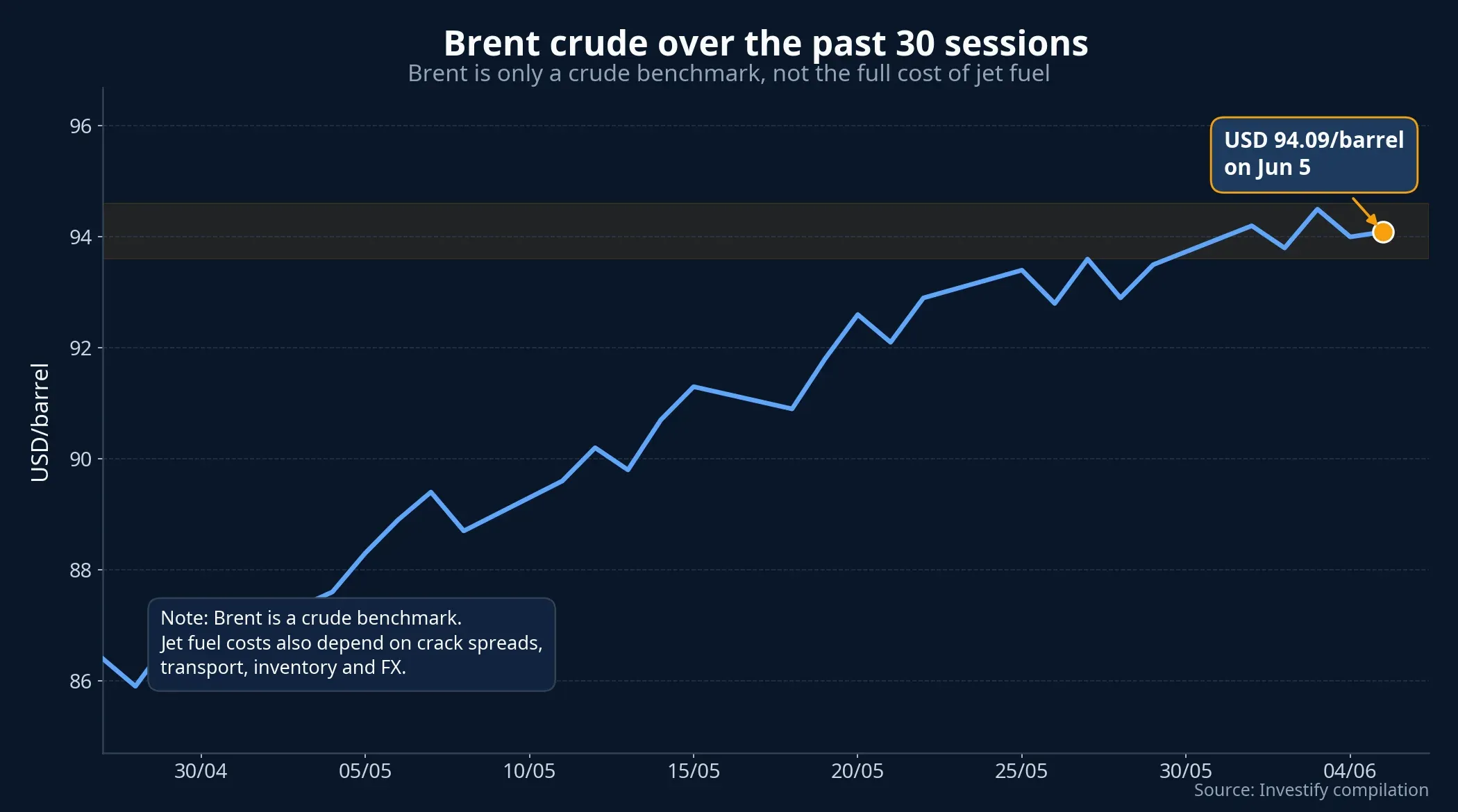

This is also where many investors misread crude oil headlines. Internal market data show Brent closing at USD 94.09 per barrel on June 5. If you only look at a one-day move, a mild pullback may create the impression that cost pressure is easing. But airlines do not buy raw Brent and pour it directly into aircraft. They pay for finished jet fuel, and that price reflects more than crude alone. Refining spreads, insurance, logistics, storage, and foreign exchange all matter.

That distinction is important because “Brent is softer” and “airline fuel costs are falling” are not interchangeable statements. In some periods, Brent may move only modestly while jet fuel stays elevated because the gap between crude and refined product widens. For first-time investors, this is one of the most useful mechanisms to remember. Watching the right variable helps avoid the false assumption that airline stocks should always trade in lockstep with the oil price shown in commodity headlines.

IATA has already changed its tone

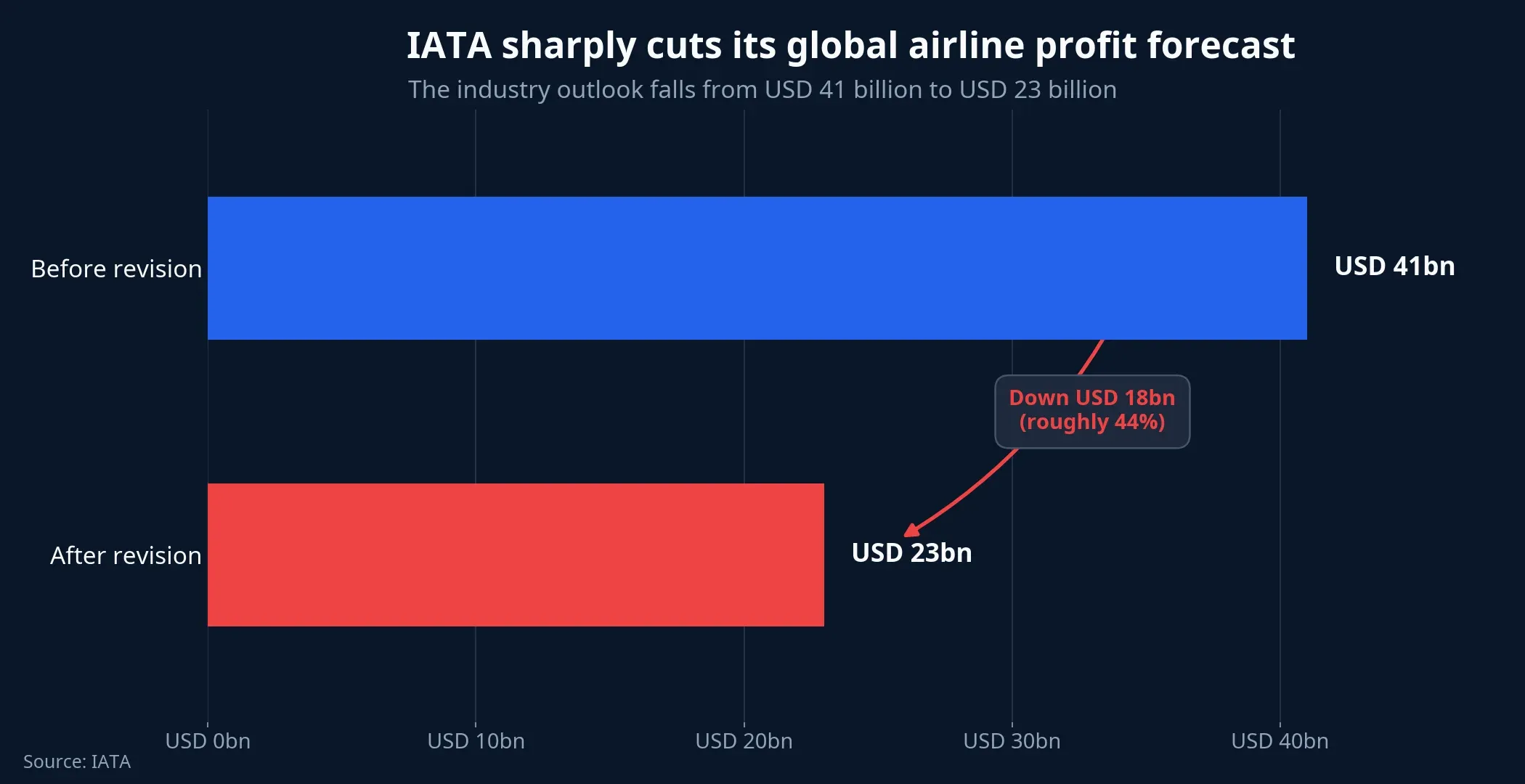

If the market needed a fresh reminder that cost pressure deserves more attention, IATA provided one on June 7. The industry body cut its 2026 global airline net profit forecast to USD 23 billion, down sharply from its previous projection of USD 41 billion.IATA

What matters is not only the lower profit number, but the reason behind it. IATA now expects industry fuel costs to rise by nearly 40%, from USD 252 billion in 2025 to USD 350 billion in 2026. Average jet fuel is projected at USD 152 per barrel, almost 70% above the prior year, while the spread between jet fuel and Brent is expected to reach USD 57 per barrel.IATA

For a new investor, those may sound like distant global numbers with little to do with one Vietnamese stock. The transmission mechanism is actually very direct. When a major industry body cuts profitability this aggressively because of jet fuel, the message is that airline margins can compress quickly even if travel demand remains healthy. In other words, a growth story in aviation does not automatically translate into a profit story once input costs change direction.

For Vietjet, that does not mean earnings will deteriorate immediately, and it certainly does not mean the recent limit-up session was somehow “wrong.” It means that from this price zone onward, the market is less likely to ignore cost risk. A stock that is being rewarded for recovery becomes more sensitive when the portion of earnings ultimately retained for shareholders is at risk of narrowing.

The real test is margin defense, not just passenger growth

When investors read an airline, many stop at one question: are passenger numbers still rising? That question matters, but it is incomplete. The more important question is how much profit each flight leaves behind after the full cost of operating it is counted.

In the latest quarter, Vietjet showed that it can still grow revenue and keep activity levels expanding. That is the constructive part of the story. But a constructive operating backdrop does not make margins immune to an input shock. If jet fuel rises for only a few sessions and then fades, the impact may remain limited to short-term market noise. If fuel prices stay elevated for weeks, the market will start scrutinizing average ticket prices, surcharges, load factors, and especially profit margins in the next set of financial results.

That is why VJC can still trade with high sensitivity even if the operating backdrop has not clearly worsened. Equity markets price the future, and the future for an airline depends not only on how many seats it sells, but on what it costs to get each flight into the air.

What matters most in the next few sessions

The most coherent thesis right now is that VJC still has a credible growth narrative, but the stock’s new price zone is likely to be much more sensitive to jet fuel than before. The rally has not been invalidated. The bar for sustaining it has simply become higher.

Over the next few sessions, three signals matter most. The first is Brent, but even more importantly the global conversation around jet fuel spreads, because that is the part that feeds directly into airline cost lines. The second is VJC’s own price behavior after a limit-up session. If it can hold the new base, the market is probably still prioritizing the growth story. If volatility rises quickly, cost risk is likely starting to be repriced. The third is what shows up in subsequent operating data and quarterly reports, especially average fares and profit margins, because that is where an input shock turns into reported numbers.

For newer investors, the key lesson is not that higher oil prices automatically mean avoiding airline stocks. The lesson is to separate the story into two layers. The first is demand growth, where Vietjet still has supportive data. The second is the company’s ability to protect profit when jet fuel changes direction. That second layer is the real test for VJC after its recent limit-up move.