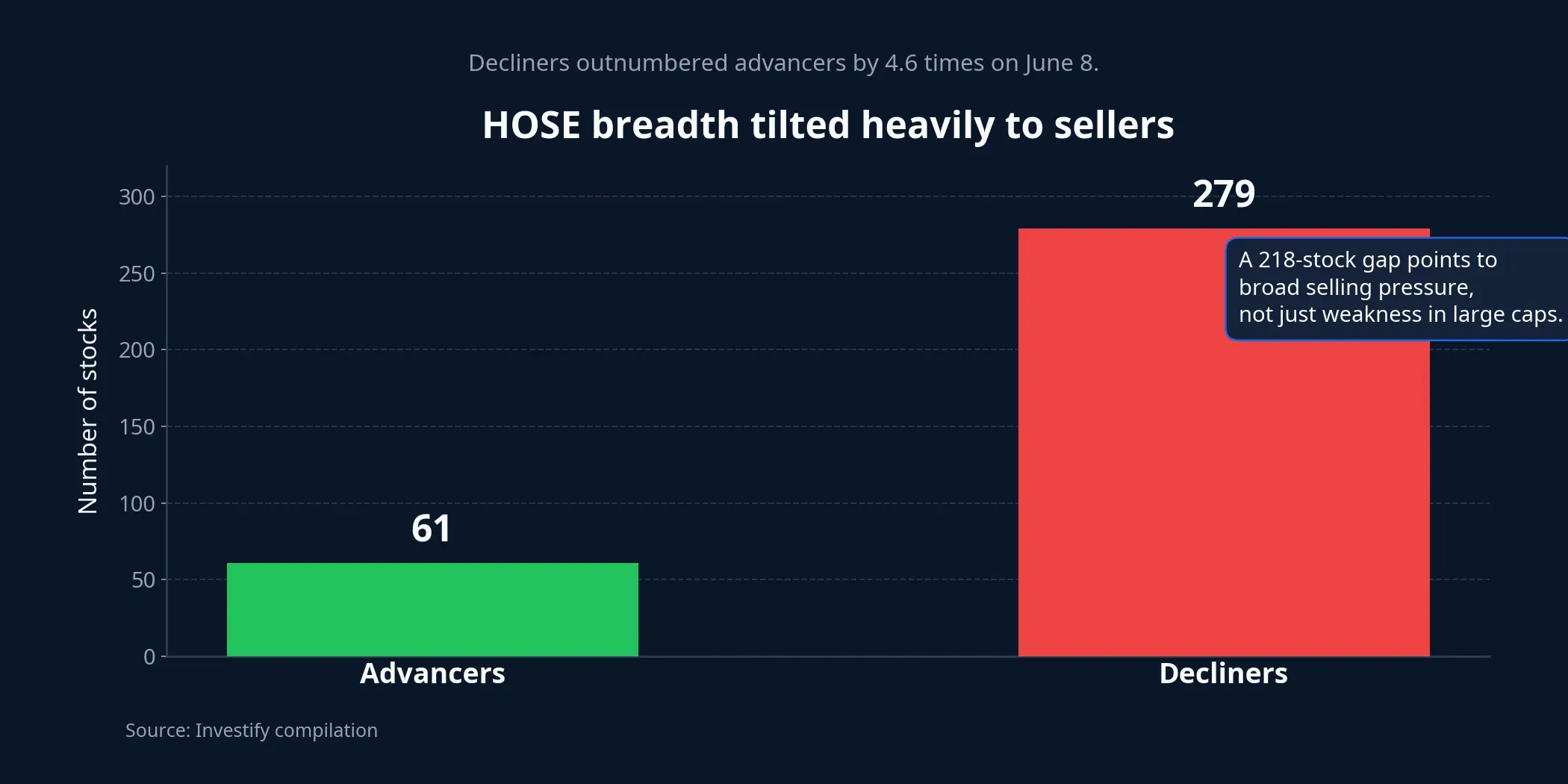

After a near-50-point sell-off, the key takeaway from June 8 is not just that the market closed in the red. VN-Index finished at 1,790.53, down 48.37 points, or 2.63%. Volume on the index reached 714,568,751 shares, while HOSE breadth narrowed to just 61 advancers against 279 decliners. In plain terms, this was not a mild pullback caused by a few heavyweight stocks. Selling pressure spread across the board.

But on days like this, the more useful question is not only how many points the market lost. It is where the money that stayed behind actually went. On June 8, the clearest answer came from a handful of real-estate stocks with meaningful turnover, not from thinly traded names posting eye-catching percentage gains.

The first read: Sellers still control the tape

Newer investors often misread a session like this in one of two ways. One mistake is to see a sharp index drop and assume liquidity has completely left the market. The other is to spot a few green real-estate tickers and conclude that the sector is leading again. Market breadth is what helps separate those impressions from the underlying reality.

When decliners outnumber advancers by more than four to one, the broader market is still trading in a defensive mood. That matters because it sets the context for every stock-specific move that follows. A few green names in a red session do not automatically prove that an entire sector is regaining strength. In this kind of tape, green only matters if it comes with real liquidity and holds into the close.

So June 8 did not show a decisive return of market-wide buying. What it showed instead was that some investors were still willing to hold risk, but only in very selective pockets.

What the real-estate bounce says, and what it does not

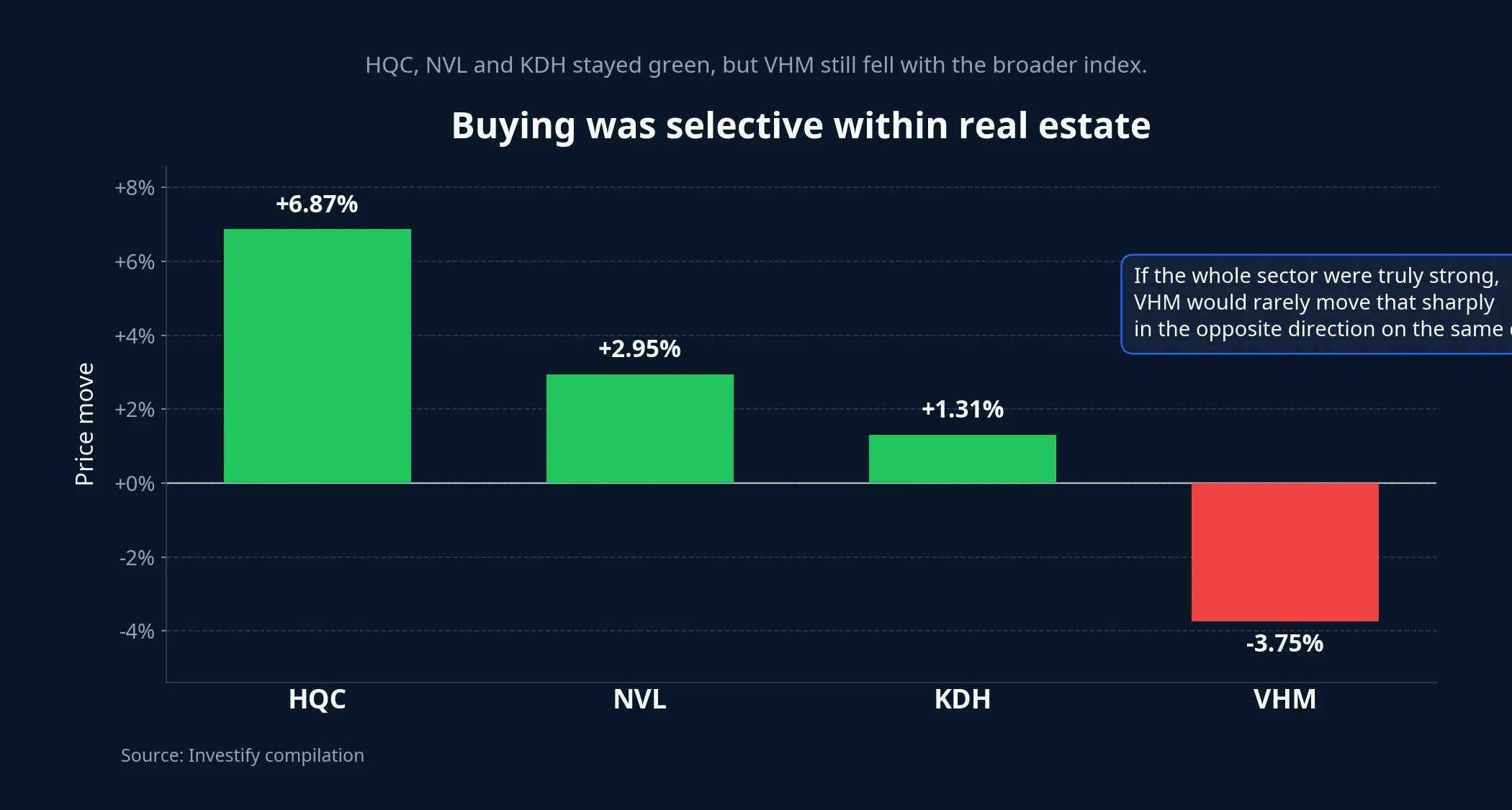

Within real estate, HQC closed at VND 2,800 per share, up 6.87%, with matched volume of 14,874,800 shares. NVL rose 2.95% to VND 13,950, trading 20,760,300 shares. KDH added 1.31% to VND 23,200, with 5,454,400 shares changing hands. These are liquid enough to treat as a short-term flow signal rather than isolated price spikes.

But the equally important point is what this move does not prove. On the same day, VHM fell 3.75% to VND 146,300. If the entire real-estate complex were truly moving in sync, a large-cap name like VHM would not usually break so sharply in the opposite direction during the same session. That is a reminder that investors were not buying “real estate” as one broad theme. They were buying specific tickers, specific narratives and specific price zones.

The simple way to read this is that money inside the sector is being tiered. One group of stocks is attracting short-term interest because of low price levels, improving turnover or an identifiable near-term story. Another group is still moving with the market’s broader weakness.

Why real estate still has a policy angle

Part of that story comes from policy. In late May, the State Bank of Vietnam issued Official Letter 4551/NHNN-CSTT for the period from January 1, 2026 to December 31, 2026, allowing incremental credit outstanding versus year-end 2025 in social housing, industrial parks and export-processing zones to be excluded from real-estate credit balances when authorities monitor growth in property lending.VnEconomy

The point to keep in mind is that this is not a blanket easing signal for the whole sector. Thoi bao Tai chinh Viet Nam reported that 25 commercial banks are eligible for the mechanism that excludes additional lending in those segments from the 2026 property-credit growth limit.TBTCVN In other words, any incremental room is still being steered selectively toward social housing, industrial parks and export-processing zones rather than spread across all developers.

VnEconomy, citing KBSV, said the incremental boost to real-estate credit from this policy is still fairly limited at about 1-2%. The same report said social-housing loans had reached only about VND 41,000 billion by mid-March 2026, well below the size of the VND 145,000 billion credit program.VnEconomy That means the policy story is real, but not large enough on its own to justify a full-sector rerating overnight.

For equity investors, the implication is a differentiated one. Companies tied more clearly to social housing, industrial parks, project legal progress or earlier cash-flow recognition are more likely to draw attention first. Firms without a story that fits this selective-credit framework can still trade with the market’s broader weakness.

Liquidity is the real test

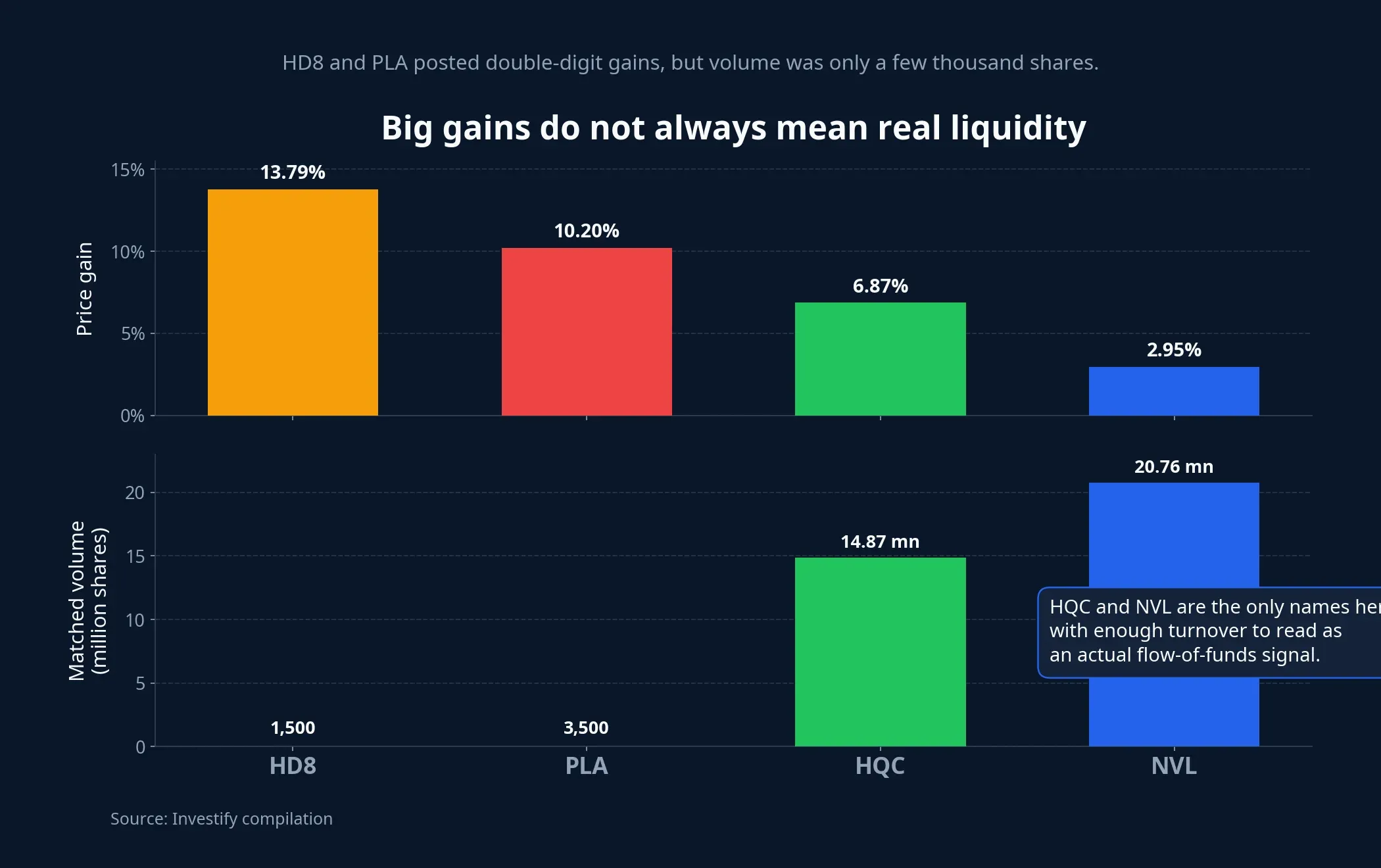

A common reading mistake is to see a double-digit gain and assume strong money is piling in. But price change is only half the story. The other half is matched volume. If a stock jumps more than 10% while trading only a few thousand shares, the move looks impressive on screen but says very little about actual market participation.

June 8 offered a clean example. HD8 rose 13.79% to VND 6,600 per share, but matched volume was only 1,500 shares. PLA climbed 10.20% to VND 5,400, with just 3,500 shares traded. By contrast, HQC and NVL posted much smaller percentage gains, yet turnover ran into the tens of millions of shares. That difference matters more than the closing color alone.

Put simply, HQC and NVL are the names that can reasonably be read as a short-term flow signal. HD8 and PLA are better understood as examples of how large percentage moves can appear in thin stocks. If those two categories are blended together and labeled as a broad “real-estate rally,” the market’s main message gets lost: money did not return evenly, it only clustered where liquidity was deep enough to enter and exit.

How to read June 9

After VN-Index slipped below 1,800, the right question for the next session is not whether real estate can “save” the market. The better question is whether the green pocket from June 8 can hold its quality. If HQC, NVL and KDH keep their buying support into the close and gains spread to other reasonably liquid real-estate names, the market may be testing a selective bottom-fishing move.

If those same names fade after the open, however, while the rest of the sector stays weak and the biggest gains remain concentrated in thin stocks, then the green screen is just a temporary shelter inside a fragile market. In that case, the important signal is not that a few names are still rising. It is that bargain hunting remains too narrow to alter the wider balance of the tape.

That is why the cleanest thesis from June 8 is not “real estate is back.” The more defensible view is that risk appetite still exists, but it is narrow and highly selective. The main risk for newer investors is not missing a huge upside move. It is mistaking a small cluster of green stocks for broad sector strength. The signals worth tracking over the next one or two sessions are the durability of turnover in HQC, NVL and KDH, and whether buying spreads to additional real-estate names with real liquidity behind them.