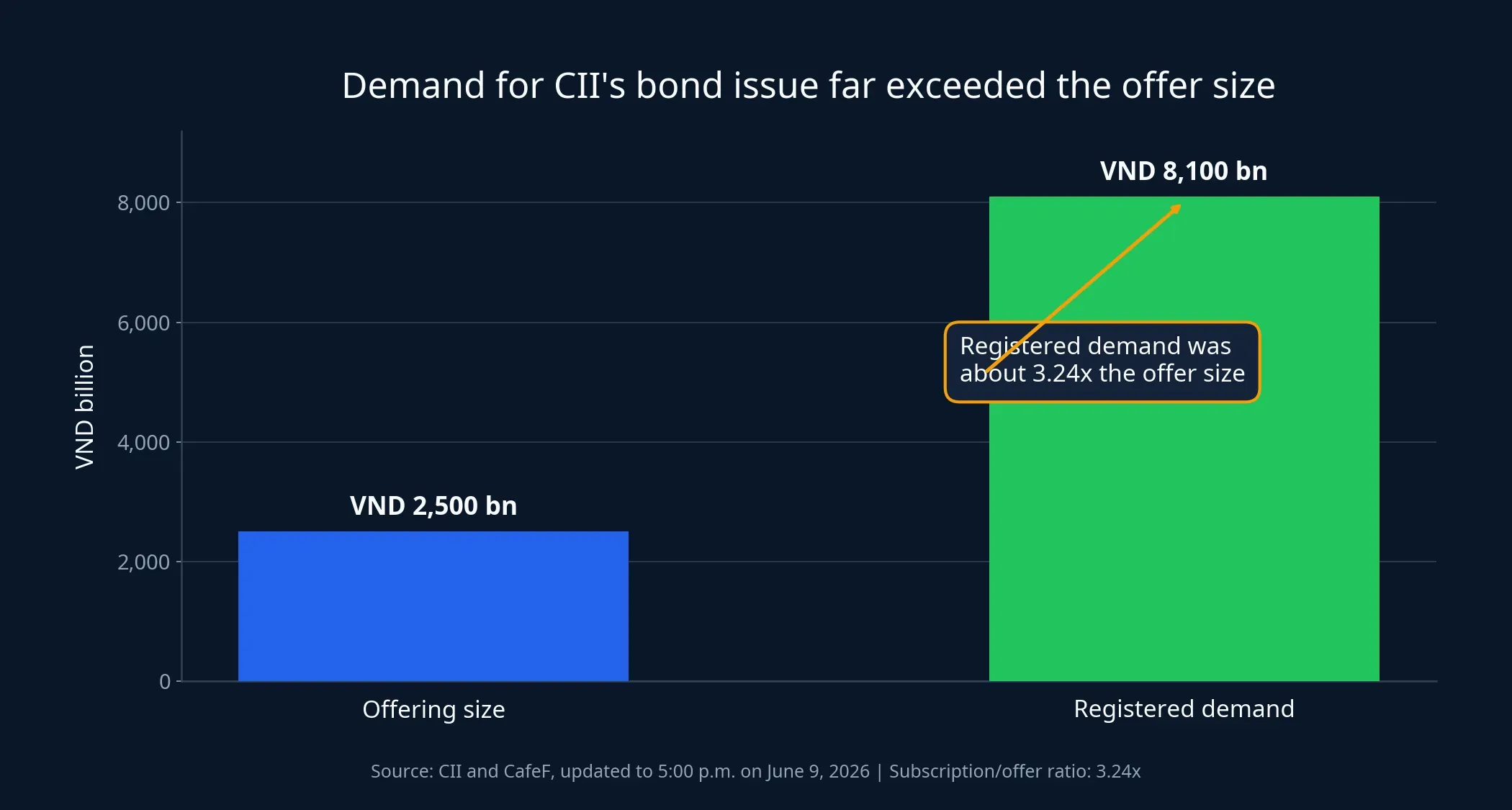

CII’s ceiling hit on June 10 mattered for a reason that had little to do with a sudden improvement in quarterly profit. The bigger shift came from funding: registrations for the company’s unsecured convertible bond offer exceeded VND 8,100 billion against an offer size of VND 2,500 billion. For an infrastructure name, that was enough for the equity market to cut some of the discount it had been placing on fundraising risk.CIICafeF

That distinction matters because stock prices do not always wait for an earnings report before they move. Sometimes they respond first to the probability that a company can raise capital, keep a project on schedule, and shorten a bottleneck investors were already worried about. CII fits that pattern: the stock closed at VND 17,500 per share, up 6.71%, on volume of 31,623,000 shares on June 10.

The market is repricing funding risk

The headline figure is not just the VND 8,100 billion in registered demand. The more important point is that the instrument is an unsecured convertible bond. Investors were not leaning on a specific pledged asset for protection. They were effectively backing CII’s ability to stay open to long-term capital and turn major infrastructure projects into real cash flow over time.CII

For an infrastructure company, that variable often matters more than a short-term jump in profit. Transport projects have long cycles, from legal preparation and financing to construction and eventual operation. If the funding leg looks fragile, the market applies a deeper discount because timing slips, financing costs rise, and shareholder returns get pushed further out.

One ceiling session can still contain other forces, including short-term momentum buying. But if one signal deserves the largest share of the explanation for June 10, it is the bond demand update. It arrived right before the stock moved and addressed the precise area where CII has long been questioned: whether it can keep securing capital for large projects.CafeF

Why a debt-market signal can move the stock

Newer investors often treat bonds and stocks as separate stories. For capital-intensive businesses, they are tightly linked. When the debt market shows that a company can still attract long-duration money with strong demand, the equity market has a reason to reduce the discount it applies to financial risk.

That logic is especially clear for CII because the company is tied to infrastructure projects that require large upfront capital and long payback periods. CafeF noted that the expansion of the Ho Chi Minh City - Trung Luong - My Thuan expressway carries a total investment of nearly VND 37,000 billion and is targeted to start operations from 2029. A VND 2,500 billion deal does not solve the full equation, but it can change how the market views the first bottleneck: whether the funding door is still open.CafeF

Put differently, the market is not rewarding CII because all risks have disappeared. It is rewarding the stock because the probability of one major risk has just eased. That difference matters. Confusing the two would turn a funding-risk repricing into a claim that the company’s full long-term value has already been validated, and those are not the same thing.

A ceiling move does not close the case

The first thing to separate after the excitement is registered demand from money actually received. More than VND 8,100 billion in registrations showed very strong interest as of 5:00 p.m. on June 9, but investors still need to see the final allocation result, the real proceeds collected, and how that money is deployed against project timelines. A more durable rerating only happens when the funding signal is followed by execution.

That is why June 10 should be read as an initial repricing step rather than a final verdict on CII’s financial strength. The stock had already been climbing gradually over the previous 30 sessions before accelerating on June 10. The latest move suggests the market is attaching fresh value to fundraising capacity, not that there is new proof of an immediate earnings inflection.

This matters for first-time investors because the market tends to react quickly to probability, while financial statements confirm things later. Without separating those two layers of information, it is easy to assume that a price surge means the fundamental story has already shifted into a new state. In reality, the stock is just moving ahead of what investors think may happen next.

Three signals to watch after June 10

The first is real cash. If the final distribution result confirms that most of the registered demand converts into actual proceeds, the market will have firmer ground for a more constructive view of CII’s funding capacity. If there is a large gap between registrations and real money collected, the June 10 enthusiasm will be much easier to question.

The second is project progress tied to the new funding. The expansion of the Ho Chi Minh City - Trung Luong - My Thuan expressway is where the market appears to be placing much of its rerating thesis. Investors therefore need to watch not only whether CII raises the money, but whether that capital helps legal, implementation, and construction milestones move forward in visible ways.CafeF

The third is whether funding costs become more manageable over coming quarters. An infrastructure company can live with leverage for a long time, but the market only pays a higher multiple when the capital burden starts to look more predictable. In that sense, strong bond demand opens the door to a better story, but the proof still has to come from future reporting periods.

Bottom line: a discount-rate reset, not a final judgment

The most coherent thesis right now is that the market has turned less pessimistic on CII’s fundraising risk. That is meaningful because for an infrastructure company, access to capital can matter almost as much as a strong quarter of profit. But this is still a repricing of one specific risk, not proof that the entire long-term growth story is now locked in.

The watch list for the next two weeks is therefore straightforward: the final bond distribution result, tangible progress on the project linked to the new funding, and signs that funding costs are becoming easier to manage. If those three pieces keep strengthening, June 10 may end up looking like the start of a more durable rerating. If not, it will stand as a market that moved quickly on a good signal before execution had fully caught up.