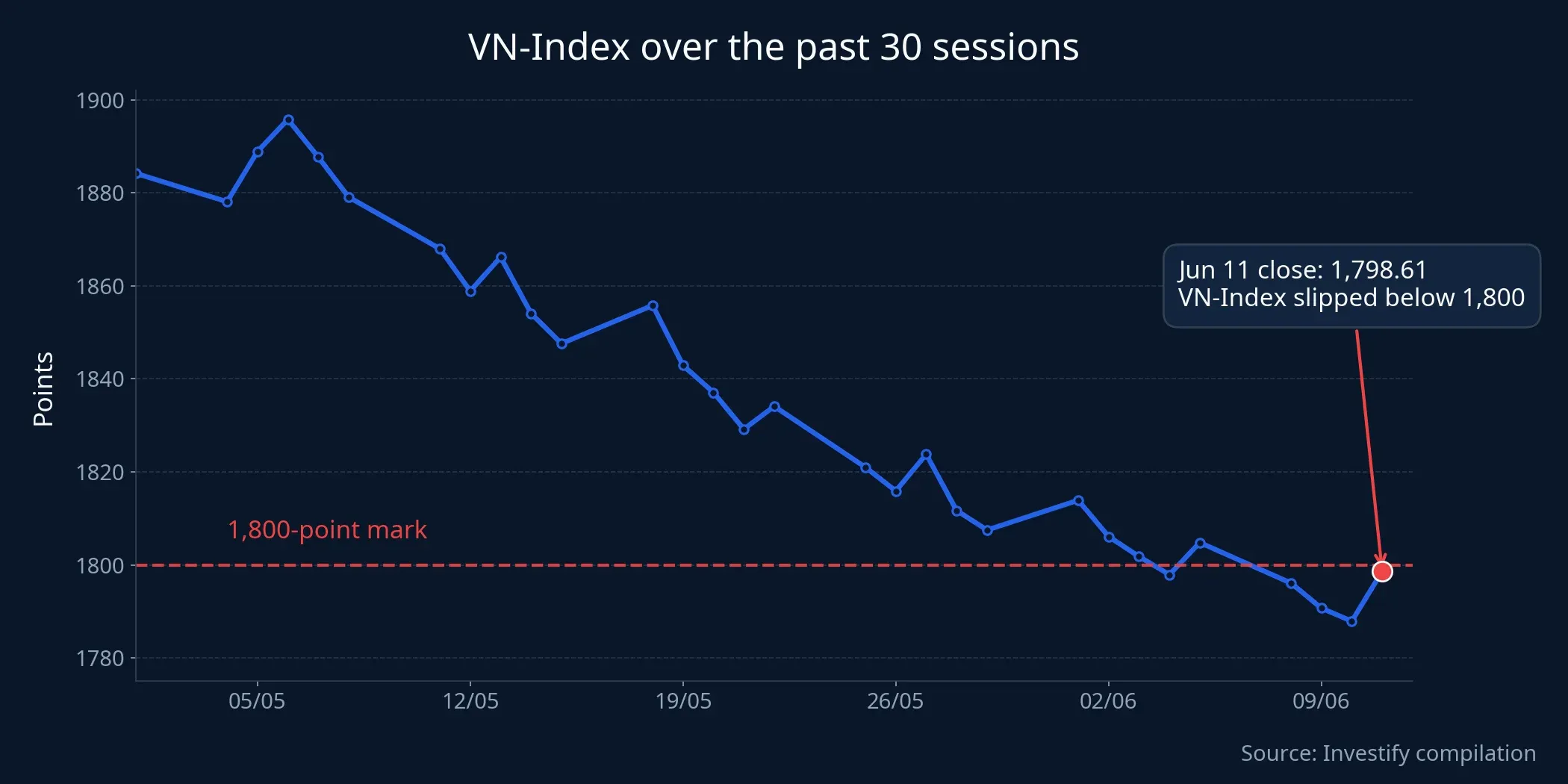

VN-Index closed June 11 at 1,798.61, down 5.10 points, or 0.28%. On the surface, that does not look like a damaging session. The HoSE still had 122 advancers, the screen was not flooded with limit-down stocks, and the overall mood did not resemble a market-wide liquidation.

Yet the market does not need to crash to leave investors uncomfortable. Once a psychological level like 1,800 gives way, the more useful question is not “how much did the index lose?” but “why did such a modest decline still push it below an important line?” VnEconomy framed the session in similar terms: the problem was fading leadership among index-heavy stocks rather than a full-scale selloff.VnEconomy

Put simply, VN-Index is a weighted index. A handful of mid- and small-cap winners cannot offset weakness in the stocks that carry the biggest weight. June 11 was a clean example of that mechanism. The market’s surface did not look disastrous, but the layer of stocks that normally pulls the index higher was no longer doing its job.

What the index was really saying

For newer investors, this is exactly the kind of session that is easy to misread. If you focus on the board, you still see green names and may assume the market is merely wobbling. If you look only at the headline loss, the 0.28% decline seems too small to matter much.

What matters is that VN-Index does not measure every stock equally. It gives far more influence to the largest listed companies. That means the index can slip through a key level even when the broader market is only mildly weak, as long as the heaviest stocks stop providing support.

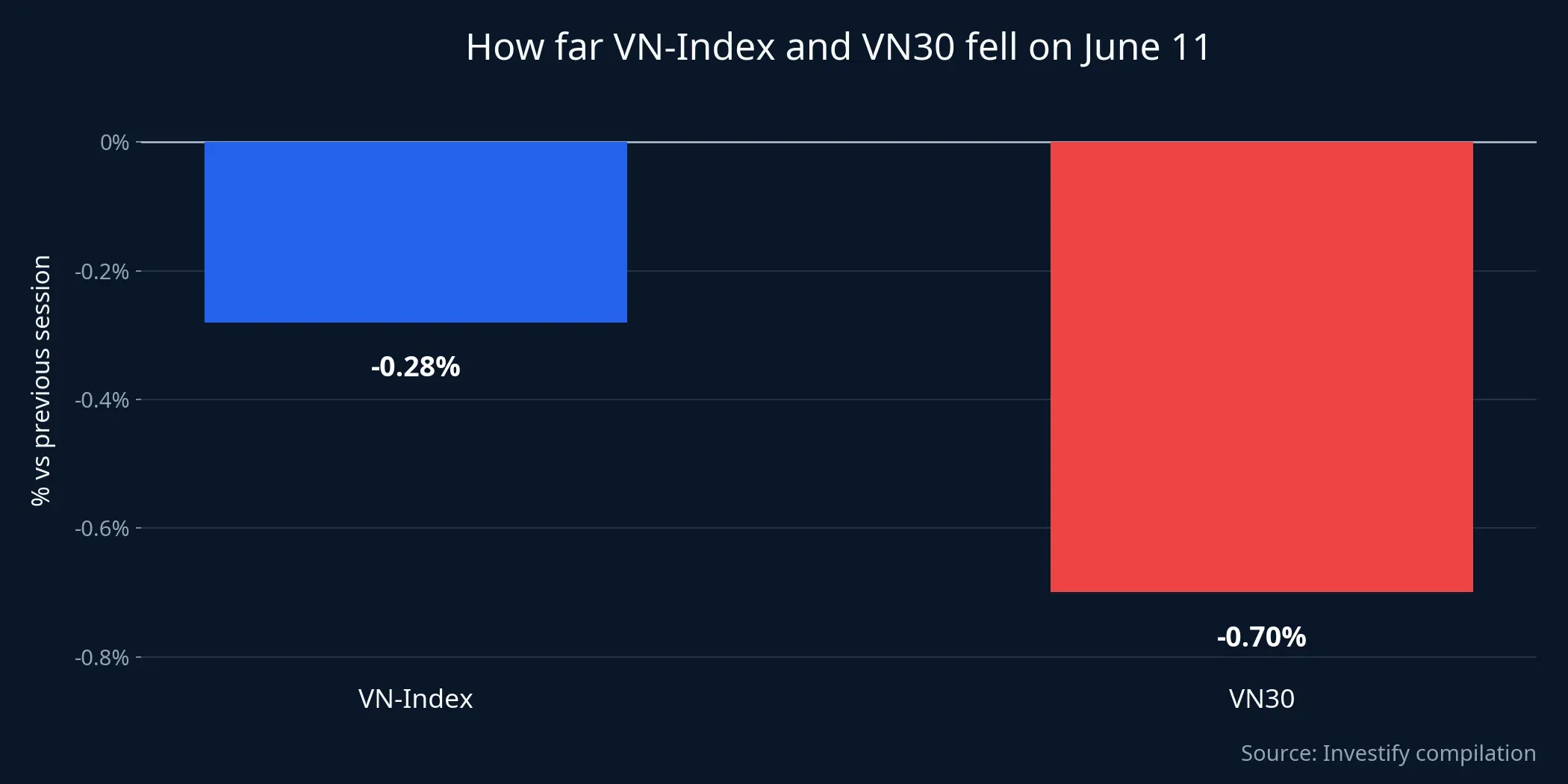

That was even more obvious in the VN30 basket. VN30-Index finished at 1,947.28, down 13.69 points, or 0.70%. That decline was materially larger than the move in VN-Index. Breadth inside the basket was worse as well, with 8 gainers and 19 decliners. When the 30 largest stocks weaken more than the broader market, the message is that the market’s backbone is softening.

That matters because levels like 1,800 only hold when large caps help defend them. If a level is held mostly by isolated rallies in smaller stocks, it tends not to last. A rebound can look respectable on the tape and still prove fragile if the leadership layer does not come back.

Why VN30 matters more than a few green stocks

If there is one core difference between June 11 and a true capitulation session, it is that the market did not break all at once. But if there is one reason to stay cautious, it is that the stocks with the greatest ability to drive the index were the weakest part of the structure. Both things can be true at the same time, and newer investors often miss the second point.

Among large caps, the individual declines were not dramatic: VHM fell 1.57%, VCB lost 0.16%, BID slipped 0.60%, CTG gave up 0.45%, TCB declined 0.32%, and VPB lost 0.19%. VIC was flat after the previous session’s rise. None of those moves, in isolation, suggests a breakdown. But when several large caps fail to lift together, their combined effect on the index becomes meaningful.

That is why investors should not reassure themselves simply by saying “some stocks were still up.” GAS held flat and MBB still gained 0.20%, but a few scattered supports cannot replace the role of a broader leadership group. A healthy market does not require every heavyweight to rally, but it does need a sufficiently large cluster of them to anchor sentiment. June 11 did not show that.

An easy way to think about it is that VN30 functions like the engine of the index. The body of the car may still look intact, and the wheels may still be on, but if the engine loses power, the whole vehicle slows down. The fact that VN30 fell more than VN-Index tells us the engine was running weaker than the rest of the market.

Thin liquidity made 1,800 easier to lose

A mild down day with heavy turnover usually means buyers and sellers are actively fighting for control. In that setting, even a decline can contain a constructive message because capital is still engaged. A mild down day with shrinking turnover says something else: many investors are standing back rather than stepping in.

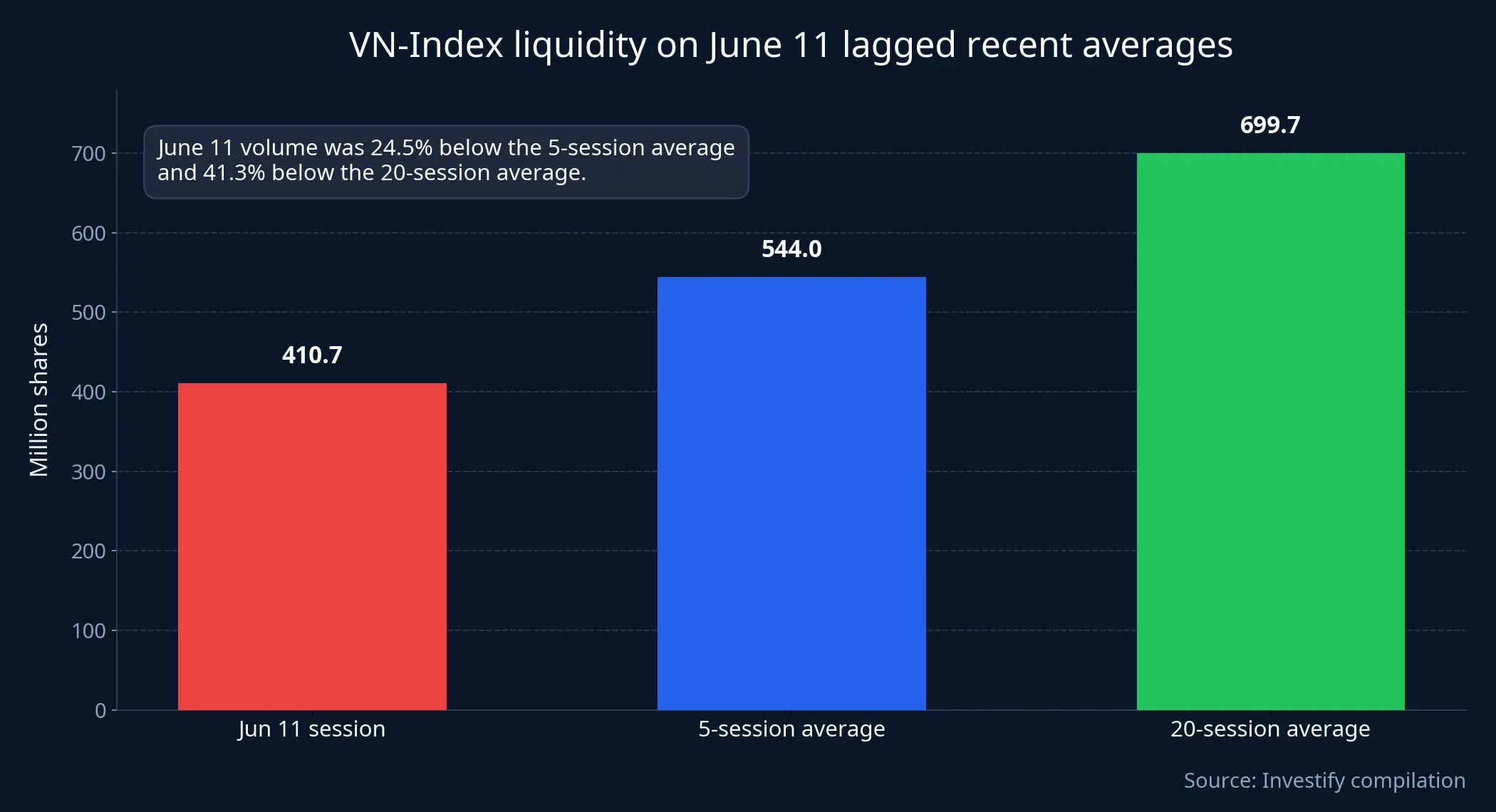

Internal data show VN-Index volume on June 11 reached 410,733,903 shares. That was 24.5% below the 5-session average and 41.3% below the 20-session average. In other words, not only did prices fail to break higher, but the money behind the move was materially thinner than what the market had recently been used to.

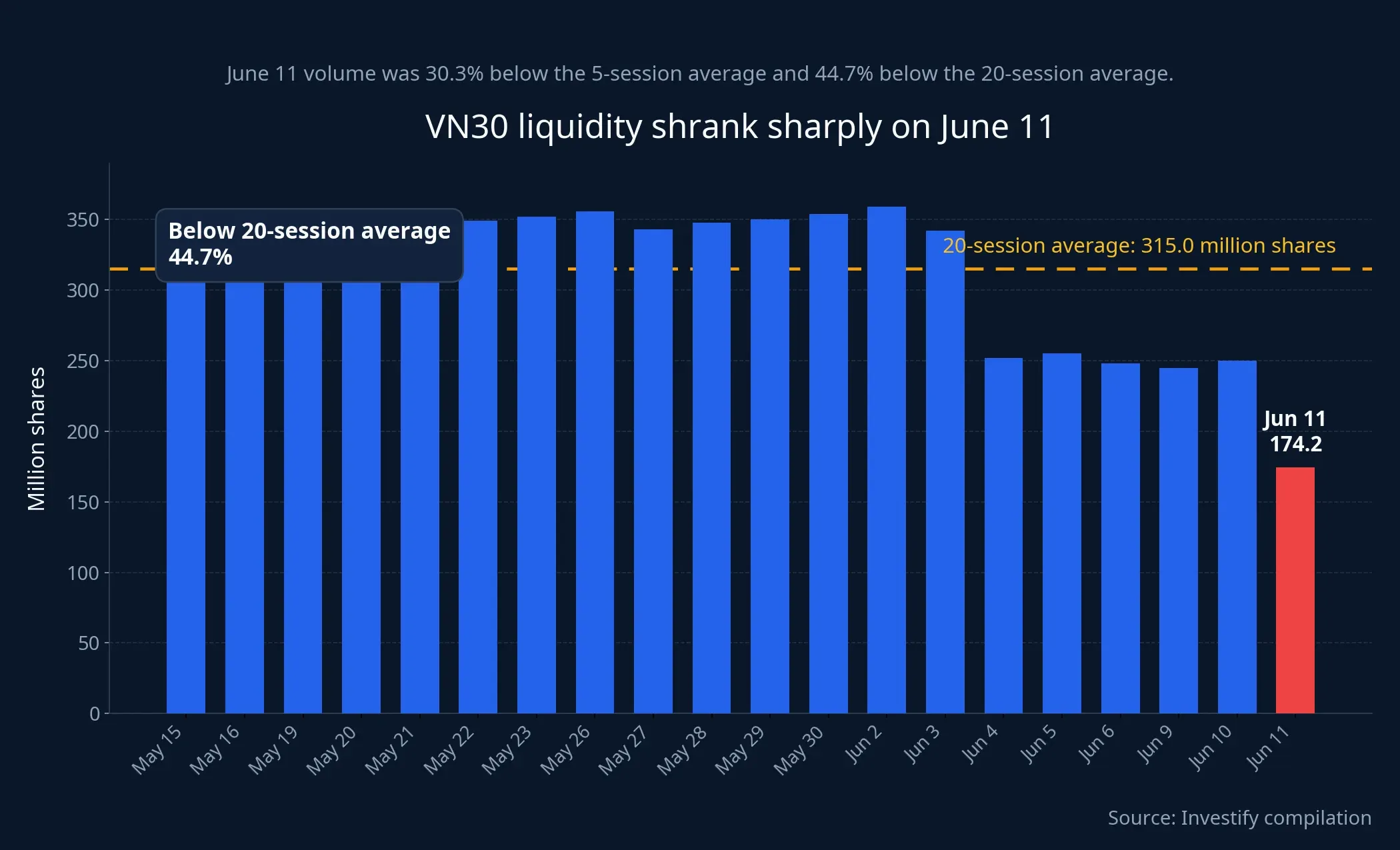

The picture was even clearer inside VN30. Volume for the basket came in at 174,219,205 shares, down 30.3% from the 5-session average and 44.7% from the 20-session average. When the stocks most capable of carrying the index also show that kind of turnover contraction, losing a psychological level is no surprise.

VnEconomy noted as early as the morning session that the key issue was not the size of the price decline, but the weakness in turnover. Morning matched value on HoSE was only about VND 4.009 trillion, while the VN30 basket generated just over VND 2.078 trillion.VnEconomy Those were not full-day numbers, but they fit the closing picture: money was not coming back forcefully enough to support the leaders.

This also helps distinguish “not enough buying” from “forced selling.” In a genuine panic, turnover usually spikes because people are trading at any available price. On June 11, the market looked more like it slipped because too few participants were willing to bid prices higher. For newer investors, that distinction matters because it changes how the next session’s risk should be read.

What to watch in the next session

Once you identify the main problem on June 11 as a leadership gap combined with thin liquidity, the follow-up checklist becomes clearer. Many investors focus only on whether VN-Index opens green or red in the first few minutes. That is quick, but it often produces the wrong conclusion because it ignores the quality of the rebound.

The first signal is VN30 itself. If VN-Index rebounds but VN30 stays sluggish, the market may simply be getting cosmetic help from smaller names or isolated technical bounces. A durable rebound usually starts with large caps stabilizing first and then broadening out.

The second signal is breadth with weight behind it. A session with many gainers is positive, but not sufficient on its own. Investors still need to ask which groups those gainers come from, how large they are, and whether banks, property developers, or consumer names are participating. If most of the green is concentrated in low-weight stocks, the index can remain vulnerable even when the market’s surface looks decent.

The third signal is whether liquidity returns to the heavyweight layer. The 1,810 area remains the nearest resistance zone, while broker views compiled by VnEconomy suggest the short-term downtrend only eases in a meaningful way if VN-Index can move beyond higher resistance with better market quality.VnEconomy In other words, a green close alone is not enough. What matters is whether the index turns green because real money has come back to the stocks that matter most.

The thesis from this session is straightforward: the market has not flashed panic, but it is missing the leadership layer needed to defend an important psychological level. That is not the loud kind of risk that comes with a sharp plunge, yet it is exactly the kind that makes investors too complacent. If VN30 and liquidity in the heavyweight group do not improve, any bounce back above 1,800 is likely to remain fragile. The three signals worth tracking over the next one to two sessions are whether VN30 recovers first, whether breadth starts to include large caps, and whether money genuinely thickens in the market’s leadership group.