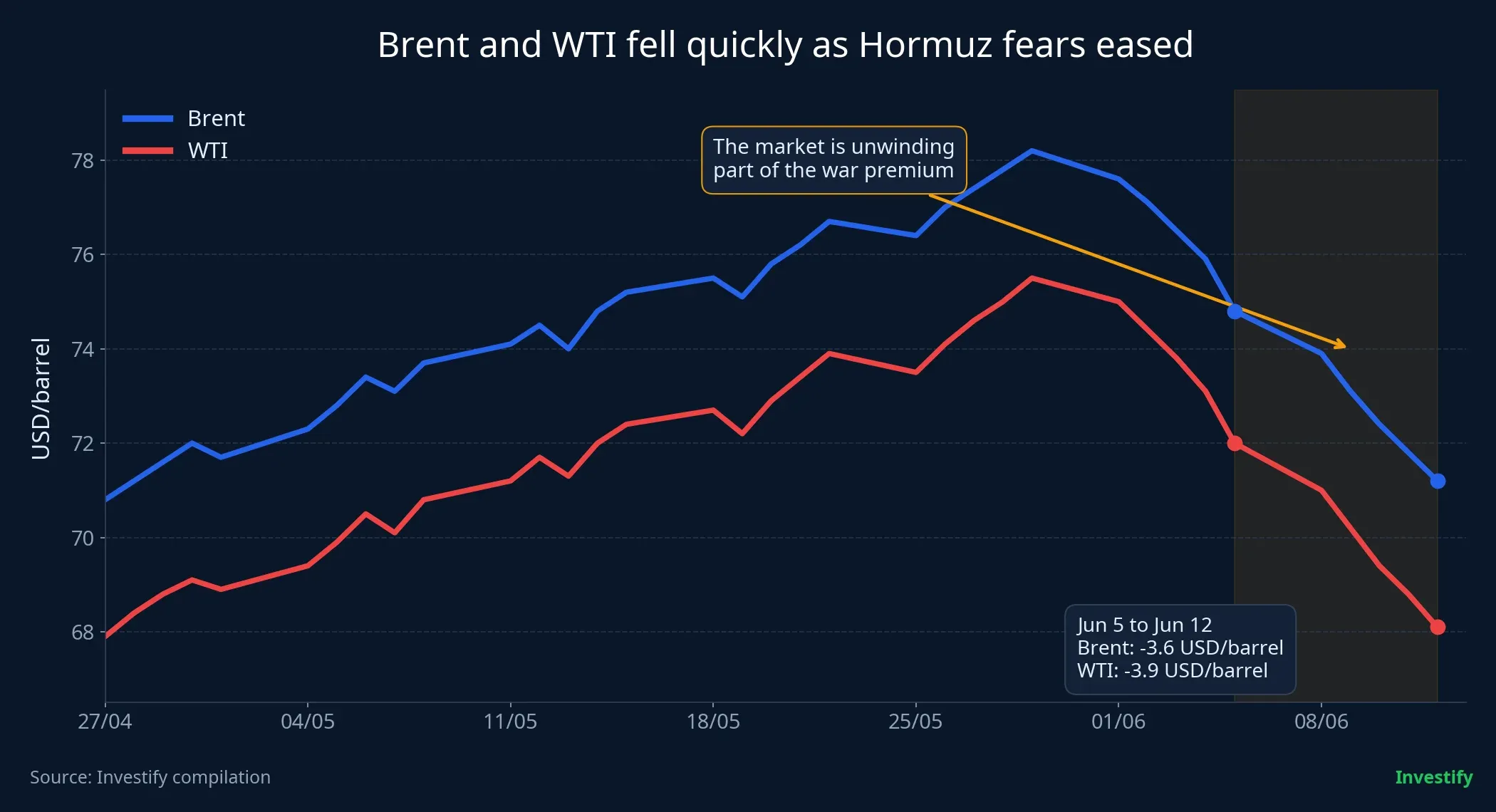

Oil is changing its question set very quickly. On June 12, Brent briefly dropped from about USD 93 a barrel to below USD 85 before rebounding above USD 89, as traders bet that traffic through the Strait of Hormuz could normalize sooner than feared.Guardian By the end of June 12, internal market data showed Brent at USD 88.33 a barrel, down 5.1% from USD 93.09 on June 5, while WTI stood at USD 85.45, down 5.6% from USD 90.54 over the same span.

The key point is not that Middle East risk has disappeared. The larger picture is that the market is shifting away from asking how much more supply could be disrupted and back toward an older question: if Hormuz starts flowing more normally again, does oil return to a market shaped by relative oversupply, thin inventories and weak demand? That is the pivot new investors need to read correctly.

The Big Picture Has Changed

The Strait of Hormuz is small on a map but enormous in oil-market math. According to the EIA, roughly 20 million barrels a day of crude and petroleum products moved through the strait in 2024, equal to about 20% of global oil consumption. Across 2024 and the first quarter of 2025, flows through Hormuz accounted for more than a quarter of global seaborne oil trade.EIA When a chokepoint of that scale comes under threat, the market is not adding a minor surcharge. It is repricing the probability of a real physical shortage.

But oil does not respond only to whether the route is legally open or closed. What traders want to see is whether real barrels are getting through, whether tankers are moving, and whether the risk premium still has to stay in the price. The Guardian reported that 36 ships passed through Hormuz between June 1 and June 7, with 17 of them switching off their automatic identification systems. The same report cited estimates that harder-to-track flows may have delivered about 1.9 million barrels a day to market since early April.Guardian That is still far below the pre-conflict level of 15.6 million barrels a day, but it is enough to make a total blockage look less certain.

From a pricing perspective, that is why oil can fall sharply on little more than a negotiating signal. Once prices are carrying a large war premium, even a modest increase in the probability of reopening can remove that premium fast. From May 12 to June 12, Brent fell from USD 107.77 a barrel to USD 88.33, a decline of 18.0%. WTI fell from USD 102.18 to USD 85.45 over the same period, down 16.4%. That is a strong correction, but it is not yet a panic selloff.

Why One Signal Can Move the Market

Investors often confuse correlation with causation. The current evidence is not strong enough to say that a single political statement alone pushed oil lower. A more defensible reading is that three forces are operating at once: expectations that diplomacy may move forward, evidence that Hormuz is no longer in a complete freeze, and a renewed focus on inventories and end demand.

That is why this should not be framed as some hidden side story. The sequence is fairly logical. As the risk of a supply choke eases, traders go straight back to the familiar model: who still needs to buy oil at elevated prices, can inventories absorb a period of softer demand, and will OPEC+ tolerate a return to lower price territory? The war is not over, but the way the market prices that war is already changing.

Removing part of the war premium also does not mean cheap oil immediately. In its June 9 Short-Term Energy Outlook, the EIA still assumed that flows through Hormuz would only begin recovering gradually in the third quarter of 2026, with trade patterns not returning close to pre-conflict conditions until early 2027. In that same report, the agency projected Brent at about USD 89 a barrel in the fourth quarter of 2026 and about USD 79 in 2027 if normalization follows that path.EIA

If Hormuz Clears, the Market Returns to Older Questions

If next week brings signals with real execution behind them, such as visibly higher tanker traffic or a specific monitoring mechanism, oil will likely continue moving away from crisis pricing and back toward the more familiar framework of supply, demand and inventories. In that scenario, the market focus would shift from fear of an outright supply squeeze to whether global demand is healthy enough to support elevated prices for much longer.

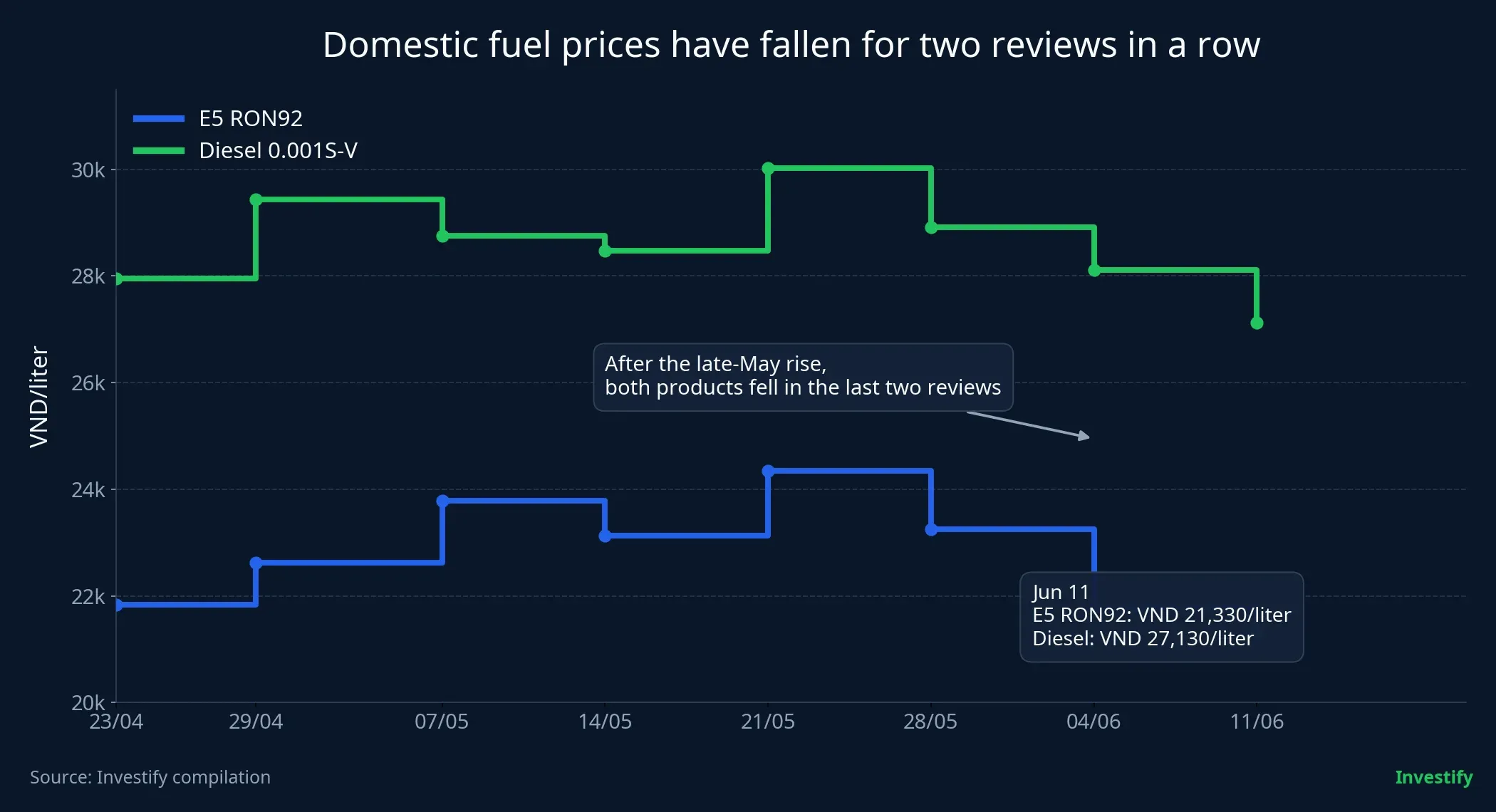

That matters for Vietnamese investors because the effects do not travel in a straight line. The first layer is inflation expectations. Domestic E5 RON92 gasoline was at VND 21,330 per liter on June 11, down 2.1% from VND 21,780 on June 4. Diesel 0.001S-V was at VND 27,130 per liter, down 3.5% from VND 28,120. Vietnam’s retail fuel adjustments move with a lag and are shaped by taxes and fees, but lower global oil still eases fuel-cost pressure.

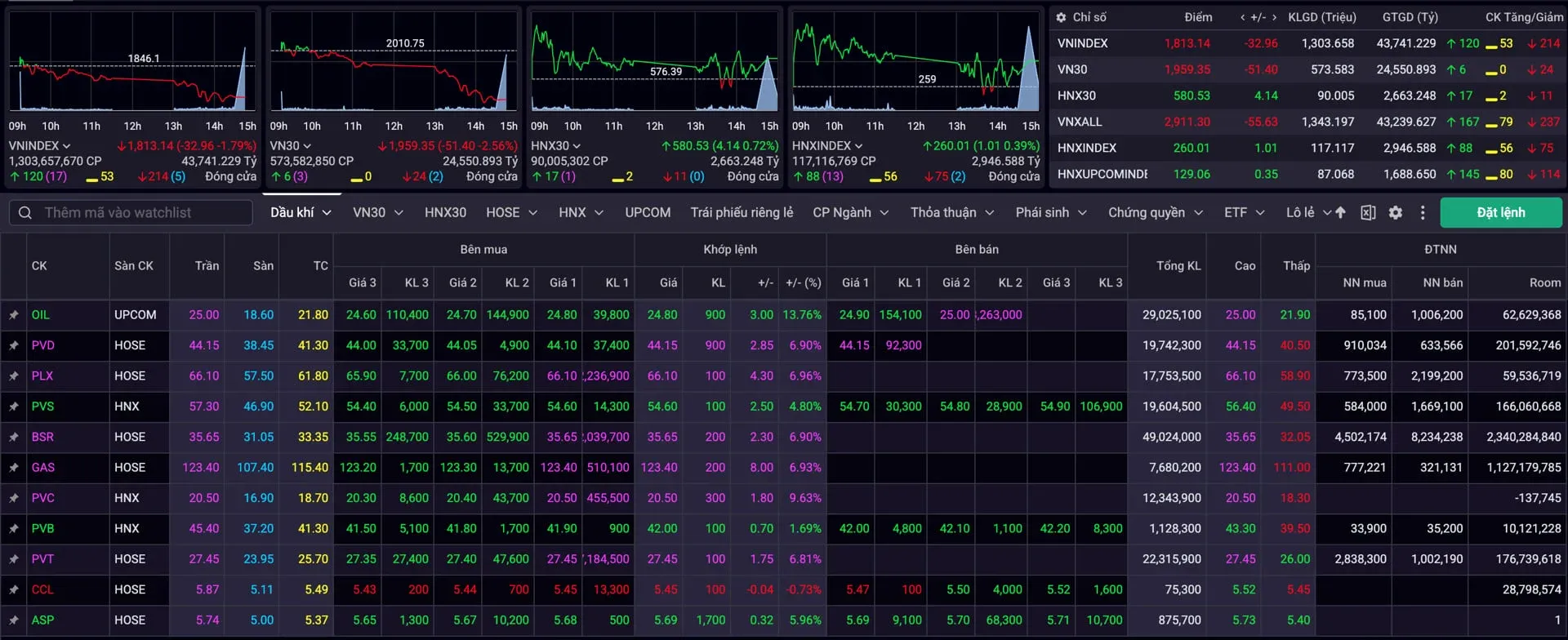

The second layer is oil and gas equities. Many newer investors still treat the sector like one switch: oil up means every stock benefits, oil down means every stock suffers. That is too simple. On June 13, PVD traded at VND 29,900 a share, down 0.8% from the previous session. PVS was at VND 38,500, down 0.3%. GAS, by contrast, rose 2.7% to VND 84,700. That divergence reflects different contract structures, revenue timing and earnings expectations across upstream, services and midstream names.

The third layer is market risk appetite more broadly. If oil falls because supply routes are clearing, global equities often breathe easier as cost pressure and inflation fears ease. But if oil falls because world demand is weakening, that becomes a negative growth signal. The same lower oil price can carry two very different messages, which is why investors cannot read the crude chart in isolation and assume the same implication for stocks.

The Reverse Scenario: The War Premium Comes Back

The opposite branch remains very much alive. If negotiations stall, key terms are disputed, or tanker flows through Hormuz fail to improve as expected, part of the war premium can return quickly. The Guardian noted that Brent rebounded above USD 89 a barrel on June 12 after doubts emerged around the reported deal terms.Guardian That is a useful reminder that oil is still being pulled around by each headline rather than trading inside a settled trend.

The EIA also provides a more cautious anchor for that scenario. The agency warned that OECD oil inventories could fall below 2.3 billion barrels by the end of 2026 if flows recover slowly, versus a prior five-year average of 2.8 billion barrels.EIA Thin inventories make the market far more sensitive to bad news, even before any new shock becomes large.

For Vietnam’s market, that still does not justify a one-click read on the oil and gas complex. PVD and PVS usually get more immediate attention if higher oil prices revive expectations for drilling and engineering activity. GAS needs to be read through power-gas demand and pricing policy as well. Fuel-intensive businesses such as airlines and transport operators face the opposite pressure if oil turns higher again. High oil prices have never distributed benefits evenly across every energy-linked stock.

What to Watch Next Week

The first signal is actual flow, not just rhetoric. If the headlines stay optimistic while tanker traffic remains murky, oil can rebound quickly.

The second signal is how crude responds to good news. If positive updates arrive and Brent barely falls, much of the reopening hope may already be in the price. If even a small negative headline triggers a sharp rally, the market still does not believe in the easing scenario.

The third signal is the cross-asset reaction inside Vietnam: retail fuel adjustments, the divergence among PVD, PVS and GAS, and the response of fuel-heavy industries. That is where investors can separate commodity volatility from company-level earnings effects.

The core thesis for this week is fairly straightforward. If real flows through Hormuz improve, oil is more likely to move out of crisis pricing and back into a market governed by oversupply, demand and inventories. The risk to that thesis is simple as well: shipping data may fail to validate the political story. The three signals worth tracking over the next few sessions are tanker traffic through Hormuz, Brent’s reaction to fresh updates and the degree of divergence inside Vietnam’s oil and gas stocks.