Markets react to a headline in minutes, but the useful signal usually arrives later. That is the right way to read this morning as well. Oil moved lower after news that the United States and Iran had reached a deal to end the war and reopen the Strait of Hormuz, yet Vietnam’s next session should not be framed as a simple one-way relief trade. The bigger picture is a test of whether the cooling move in oil spreads into defensive assets and into sectors that benefit from lower input costs.

What stands out is that investors are repricing geopolitical risk, not responding to a fully completed process. AP reported that the full details of the agreement were not immediately released, and that signing is expected in Switzerland on June 19.AP A day earlier, AP also reported that Pakistan said a deal could be completed within 24 hours, while Iran signaled it needed more time and had not signed yet.AP In other words, price has already moved on the expectation of de-escalation, while physical shipping flows and the market’s deeper risk posture still need confirmation.

A political statement is not the end of the process

Donald Trump, President of the United States in the U.S. government, accelerated the market reaction when he said the U.S. had reached a deal with Iran and had allowed the naval blockade of Iranian ports in the region to be lifted.AP For energy markets, the mere possibility of Hormuz reopening is enough to pull down the geopolitical risk premium. The strait is not just a geopolitical symbol. It is a choke point for oil, liquefied natural gas, fertilizers and shipping. Once that choke point looks less threatening, commodities are the first place where prices reset.

Still, new investors can easily jump from “there is a deal” to “the risk is gone.” Macro rarely works that cleanly. A statement is followed by signing, then by implementation guidance, then by the practical question of whether vessels move through the route smoothly again. AP also noted that Iran’s nuclear issue remains unresolved in the arrangement now being discussed.AP That is why the important part is not the headline itself but the chain reaction that follows it.

Oil has clearly moved lower, but that is only the first layer

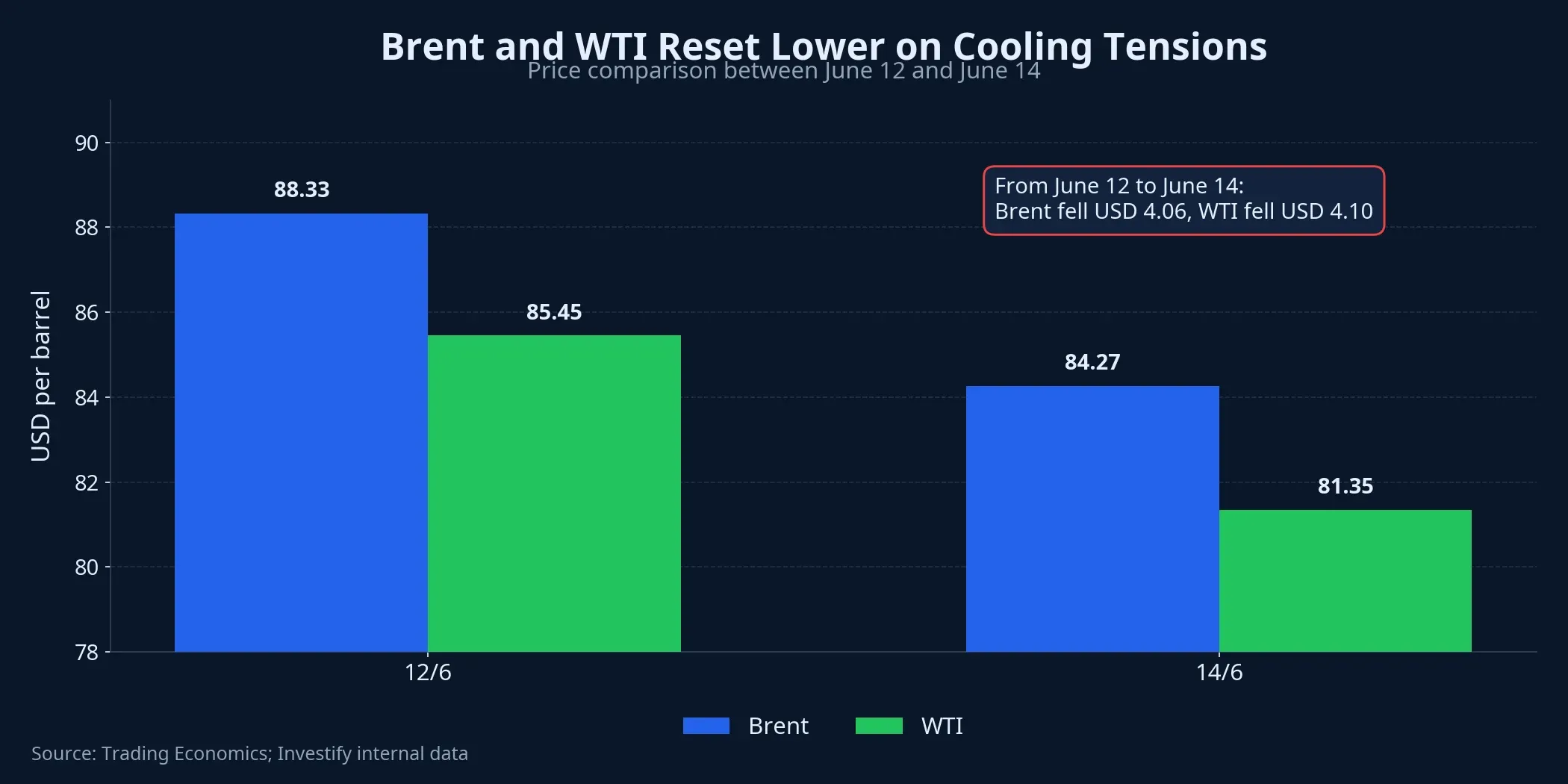

Trading Economics showed WTI at USD 81.35 per barrel and Brent at USD 84.27 per barrel on June 14, down 4.16% and 3.50% from the previous session, respectively.Trading Economics In Investify’s earlier internal data, Brent had closed at USD 88.33 per barrel on June 12, while WTI stood at USD 85.45. Read across those two points, this is more than a few hours of noise around a hot headline. The market had already started taking out a meaningful chunk of geopolitical premium before the narrative became more widely circulated.

That matters because oil is the first transmission channel into Vietnam. When crude drops, the most direct pressure usually falls on upstream oil and gas names, oil services and stocks that investors price closely against commodity swings. But the second layer is more important for retail investors: domestic fuel prices, inflation expectations, exchange-rate pressure and whether capital starts rotating into businesses that benefit from cheaper inputs.

Discipline matters here. Lower oil does not automatically mean every airline, transport or plastics stock must rally on cue. Investors may wait for another round of confirmation if they believe the U.S.-Iran story can still be challenged or delayed. So cheaper oil is a necessary condition for easier sentiment, but not enough on its own to prove that a full risk-on turn has arrived.

Domestic fuel prices show that part of the support is already here

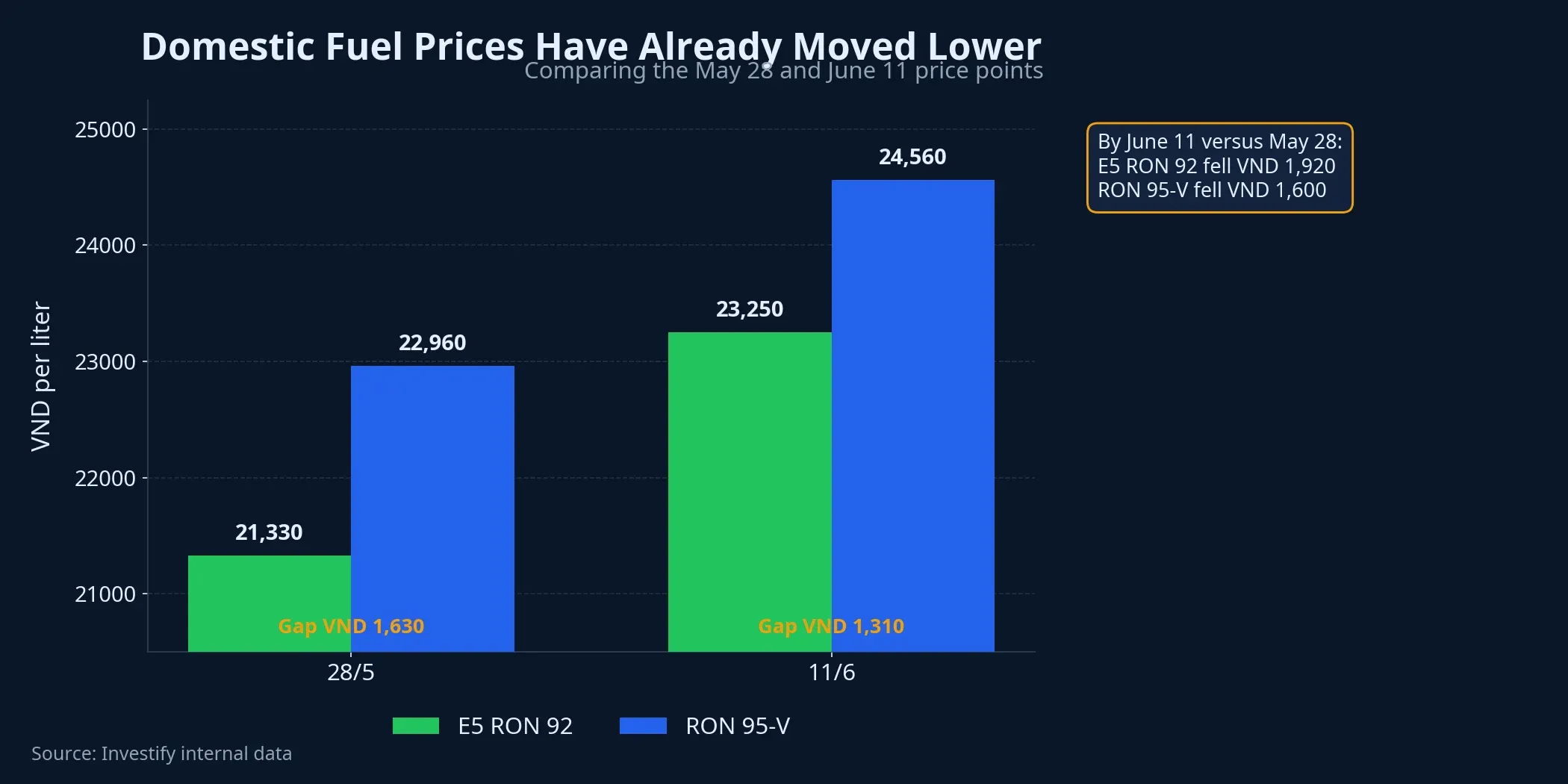

If investors only watch international markets, they can miss the detail that sits much closer to household budgets. Internal data show Vietnam’s E5 RON 92 gasoline price at VND 21,330 per liter on June 11, down from VND 23,250 per liter on May 28. RON 95-V stood at VND 22,960 per liter on June 11, versus VND 24,560 per liter on May 28. That means part of the cost relief story had already started to show up before the U.S.-Iran headline became the weekend’s dominant narrative.

For airlines, transport operators and some consumer businesses, this is more useful than watching crude in isolation. Lower fuel costs can change margin expectations, especially for companies that have just come through a period of anxiety over rising energy prices. Put differently, the next session may not immediately settle who wins and who loses. It is the point where the market starts testing which groups deserve to be repriced first.

There is still one variable that cannot be ignored: transmission speed. Lower international oil prices do not guarantee another immediate cut in domestic fuel prices. If crude only falls briefly and then rebounds because signing is delayed or real-world implementation gets messy, the optimism being built this morning can fade quickly by the close or in the next few sessions. This is a story about probability and durability, not about reflex trading.

Vietnam’s session should be read through three confirmation signals

Rather than trying to predict how many points the index may gain in the first few minutes, retail investors can read the morning through three clearer signals.

- Whether Brent holds its new lower range. If oil keeps falling or at least stays near the lower post-headline level, markets have stronger grounds to believe that geopolitical premium is genuinely coming out.

- Whether gold and USD/VND cool alongside oil. Internal data put spot gold at USD 4,202.09 per ounce on June 12, after a 3.46% jump on June 11, while USD/VND stood at VND 26,337.50 per dollar on June 12 and was nearly flat versus prior sessions. If oil falls but gold stays elevated and USD/VND does not ease, the message is that only one layer of risk has softened while defensive positioning remains in place.

- Whether domestic capital rotates in the way the mechanism suggests. VN-Index was recorded at 1,791.65 points before the opening bell, but the more useful signal is the breadth of liquidity. If the index rebounds while sectors benefiting from lower input costs fail to attract money, the market is still questioning the durability of the headline.

The value of these three signals is that they keep investors from overreacting to a green screen. A good index print is not always the same as good market quality. By contrast, a mixed but mechanically consistent session can say much more about what comes next. The bigger picture is that confirmation across assets is usually more reliable than the reaction of any single stock group.

What decides whether the rebound has substance

If the constructive scenario plays out, meaning oil keeps easing, gold softens, USD/VND does not tighten and local money spreads into sectors helped by lower input costs, then Vietnam can read this as a more credible easing of risk conditions. In that case, pressure on oil and gas names may appear early, but the more important question is whether capital finds somewhere else to go. When the market can rotate rather than simply react, a rebound usually lasts longer than a purely emotional bounce.

If instead oil rebounds because signing is pushed back, or if gold and the dollar remain in defensive mode, any relief rally is more likely to be headline-driven and short-lived. That is not a bearish verdict by itself. It is simply the right order of analysis: read the cross-asset response first, then move into sector-level interpretation. Retail investors often get hurt by reversing that order, picking tickers before they understand how broad risk conditions are shifting.

The conclusion is fairly direct. Vietnam has enough reason to open with lighter sentiment, but the right thesis is not contained in the phrase “a deal has been reached.” The real thesis is whether the cooling move is confirmed at the same time by oil, gold, USD/VND and sector rotation inside the equity market. The main signals to watch over the next one to two sessions are whether oil holds the new lower range, whether gold stops staying elevated, whether USD/VND eases and whether input-cost beneficiaries attract real money.