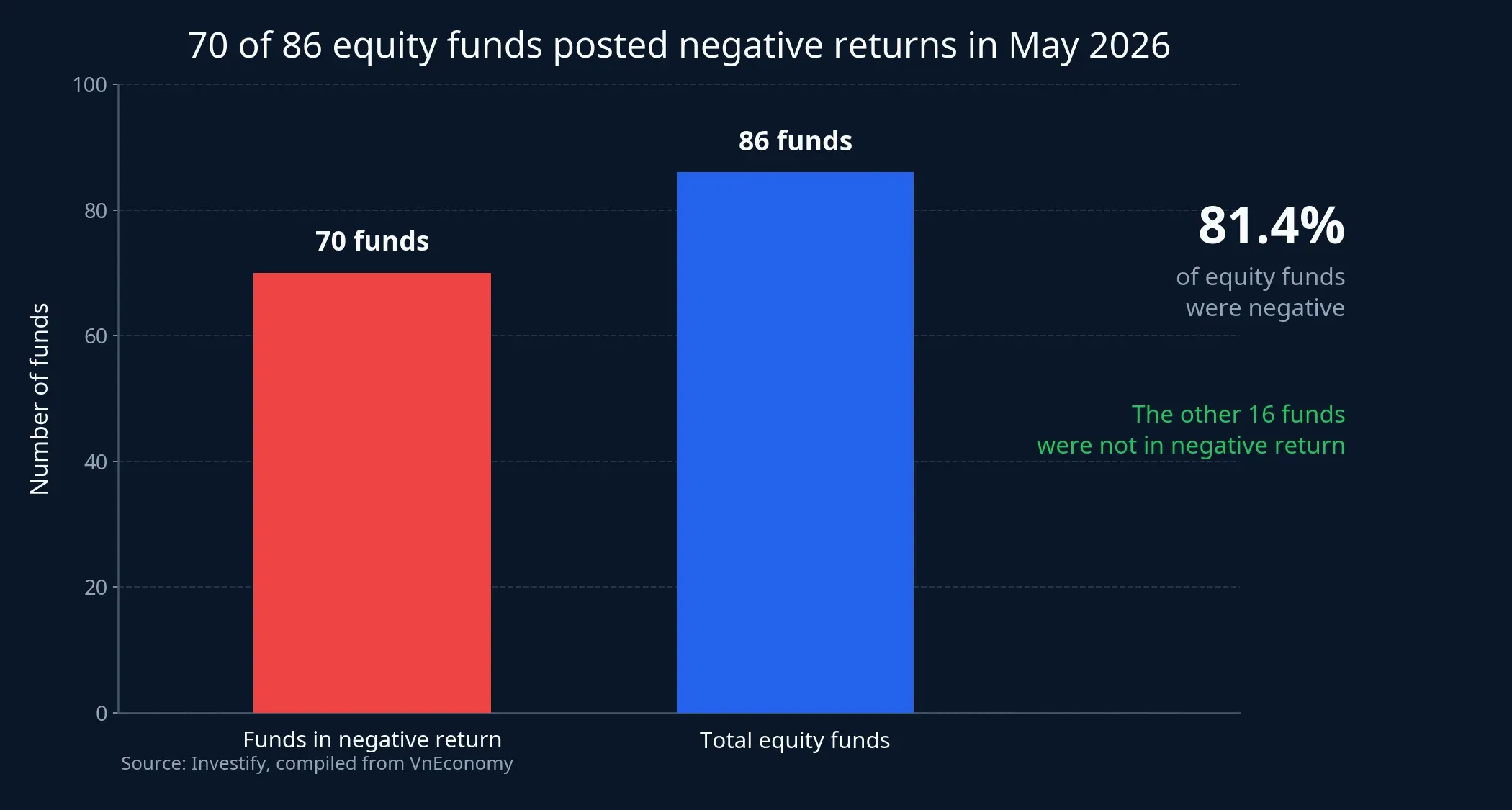

May offered a useful lesson for first-time investors: an equity fund does not automatically make a market setback easier to stomach. The latest data show that 70 of 86 equity funds posted negative returns in May 2026, with the group down an average of 1.4%.VnEconomy If you only focus on the word “fund,” that result can look puzzling. Once you focus on what the product actually holds, it becomes much easier to understand.

What you are buying in an equity fund is still, first and foremost, a portfolio of stocks. You no longer need to pick each name yourself or follow every corporate headline every day, but the volatility of the underlying asset class is still there. Put simply, a fund lets you hire someone to steer the portfolio. It does not turn a mountain road into a flat highway.

A misconception worth fixing

Many new investors assume that buying an equity fund means buying a safer version of the stock market. That is only half true. A fund can reduce the risk of concentrating too much money in a single stock, cut down on emotional trading mistakes, and add discipline to how a portfolio is managed. But the second half of the story remains unchanged: if the stocks inside the fund decline, the fund’s NAV declines too.

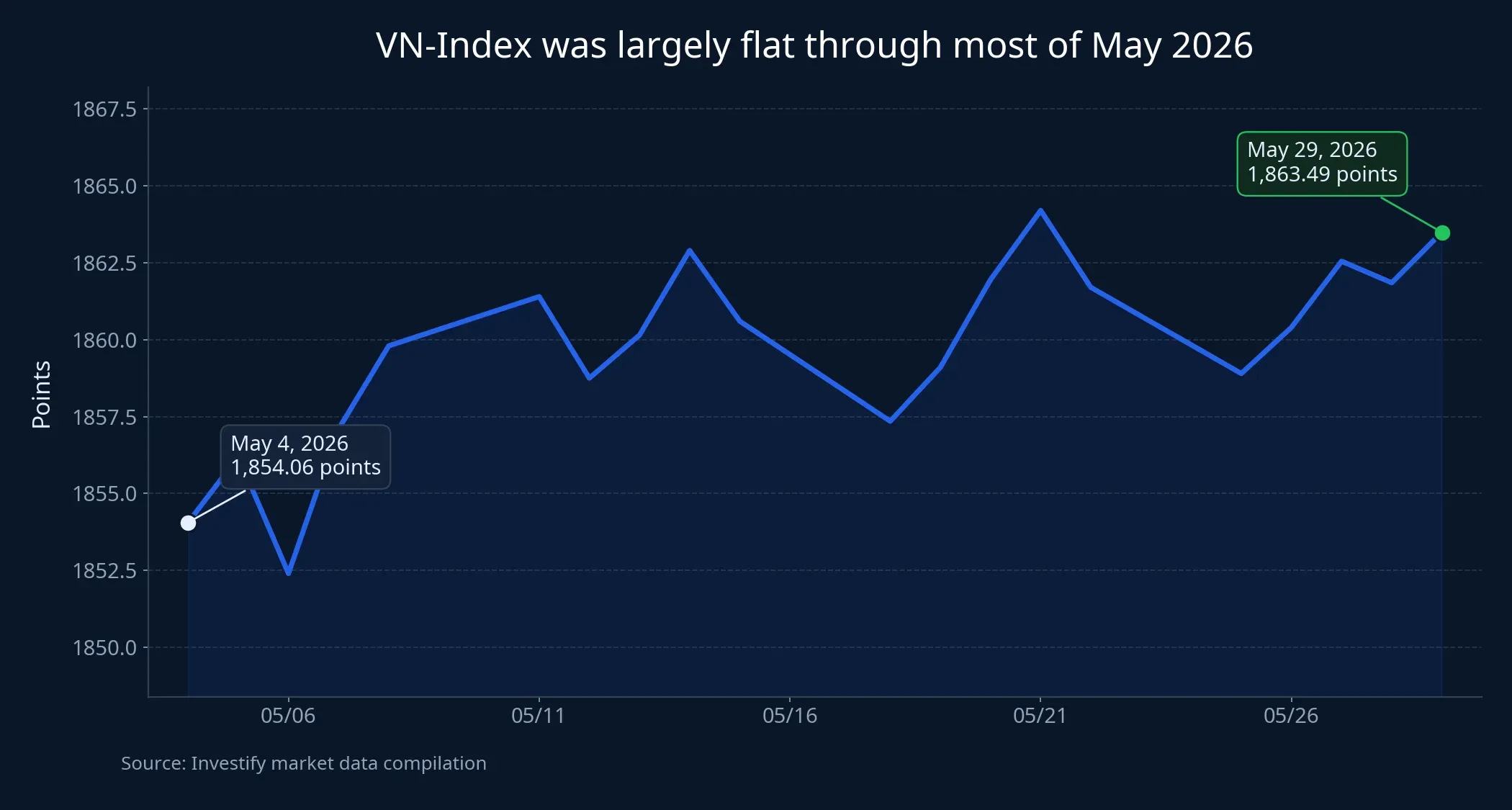

The important detail is that May was not a month of market panic. The VN-Index moved from 1,854.06 points on May 4 to 1,863.49 points on May 29, spending most of the month in a relatively narrow band rather than collapsing.VnEconomy That matters because it reminds investors that a fund can still post a negative month even when the headline index does not suffer a deep drop. The answer usually lies in portfolio construction, sector exposure, and investor withdrawals rather than in the headline move of the benchmark alone.

Diversification reduces stock-picking risk, not market risk

This is where beginners most often get the story wrong. Diversification and downside protection are not the same thing. If you buy a single stock on your own, risk is highly concentrated: a weak earnings report, a management issue, or one heavy selloff session can hit your account hard. In a fund, that company-specific risk is spread across many positions. That often makes the experience less extreme, but it does not mean the fund is insulated from a broader decline in equities.

The easiest way to picture it is as a basket. If the basket holds 30 stocks instead of 3, one bad name hurts less. But if many of the items inside the basket come under pressure at the same time, the basket still tilts lower. That is why an equity fund should be seen as a more organized way to participate in the market, not as a built-in shock absorber.

May 2026 was a clean example. According to VnEconomy, the funds that still delivered positive performance during the month largely benefited from heavier exposure to stocks that rose, including VCB, ACB, LPB, GAS, PLX, VHM, and GEX.VnEconomy That does not prove that simply owning the right names guarantees success. What it does show is that the difference between funds is highly concrete: what they own, in what size, and how tightly they track an index.

Why many funds were negative while the index stayed flat

There are at least three plausible explanations, and it would be sloppy to collapse them into a single cause. The first is portfolio dispersion. The VN-Index is one aggregate number for the whole market, while every fund carries its own structure of holdings. A fund that leans heavily into weak sectors can underperform the index materially, while another fund with more exposure to winning names can still finish positive.

The second is fund flow pressure. As of the end of May 2026, the total NAV of investment funds stood at more than VND 260 trillion, down VND 6.1 trillion, or 2.3%, during the month. Compared with the August 2025 peak, industry-wide NAV was still 20.3% lower, while cumulative net withdrawals since that point had exceeded VND 39.3 trillion.VnEconomy That is no longer a minor short-term contraction. It suggests that impatience among fund holders remains a major variable.

The third is how each vehicle operates. ETFs are built to replicate an index, so when money leaves the product, the portfolio adjustment pressure often lands directly on large and liquid stocks inside the basket. Active funds have more flexibility because they can hold more cash or deviate from the benchmark, but in exchange investors take on the risk that the manager may get the timing or sector call wrong. In other words, neither ETFs nor active funds come with a default shield. They simply absorb market stress in different ways.

What new investors should actually read in an equity fund

Start with the holdings. Do not stop at a familiar or reassuring fund name. Look at the top 5 to 10 positions, check how much exposure sits in banks, property, energy, or consumer names, and see whether the fund is leaning too heavily on one leadership group. A fund with 60% of assets clustered in a few sectors will react very differently from a more evenly spread fund, even if both are marketed as equity funds.

Next comes cash. Cash often makes a fund look less exciting during a strong rally, but it can provide useful cushioning in a correction. For beginners, this is a practical detail because it determines whether the fund has to ride every market swing in full. A low-cash fund will usually move much more closely with market volatility. A fund with a larger buffer may sacrifice some upside in exchange for better shock absorption.

Then look at tracking behavior. If the vehicle is an ETF, you should expect it to move with its benchmark most of the time. If it is an active fund, look across several months rather than anchoring on a single green or red month. One negative month is not enough to call a fund weak. But if a fund repeatedly lags the market over a longer stretch, the real question is where the strategy is drifting and whether the fee you pay for active management is still justified.

The final variable is your own holding period. This is often where a beginner’s wallet feels the most damage. If you use short-term money to buy an equity fund, you can easily turn an ordinary bout of volatility into a poorly timed redemption decision. Equity funds are better suited to money with enough time to sit through more than one correction cycle, not to money you may need to pull out as soon as the market becomes uncomfortable.

Conclusion: a fund buys risk management, not risk removal

The central point of this piece is straightforward: an equity fund is not a tool for avoiding declines. It is a tool for entering the market with better structure and discipline. May 2026 made that visible. When 70 of 86 equity funds posted negative returns even though the benchmark did not suffer a major fall, the problem was not that funds had somehow “failed.” The problem was the expectation that handing money to professionals would automatically shrink volatility.VnEconomy

For new investors, the better question is no longer “is this fund safe.” It is “what kind of risk is this fund carrying right now.” Is the pressure coming from concentrated holdings, from a low cash buffer, from close benchmark tracking, or from withdrawals by other fund holders. Once you can read those four layers, you start seeing equity funds more clearly: not as a perfect umbrella, but as a better-prepared way to walk into the rain.