SJC gold has climbed back to VND 150.5 million per tael, while the VN-Index closed the June 15 session at 1,799.31 points.VietnamNetVietnamPlus Those two numbers appeared on the same day, but they are selling two very different promises. Gold is selling peace of mind. Equities are selling the possibility of a recovery if money flow returns with enough conviction.

For a new investor, that distinction matters more than the headline price. When gold clears a psychological level like VND 150 million per tael, it feels safer because it is tangible and familiar. But that feeling is not free. At current levels, a fresh SJC buyer is paying not just for global gold, but also for the domestic premium, the buy-sell spread, and the belief that physical gold will hold its value if markets turn unstable.

That leads to a fairly simple thesis. SJC gold at VND 150.5 million per tael still has a defensive role, but it has become materially more expensive for anyone whose real goal is just to park money for one to three months. If capital preservation is the priority, bank deposits are now a much closer competitor than they look at first glance. Equities, meanwhile, only become a stronger case if the VN-Index moves decisively above 1,800 with credible liquidity behind it.

What SJC buyers are really paying for

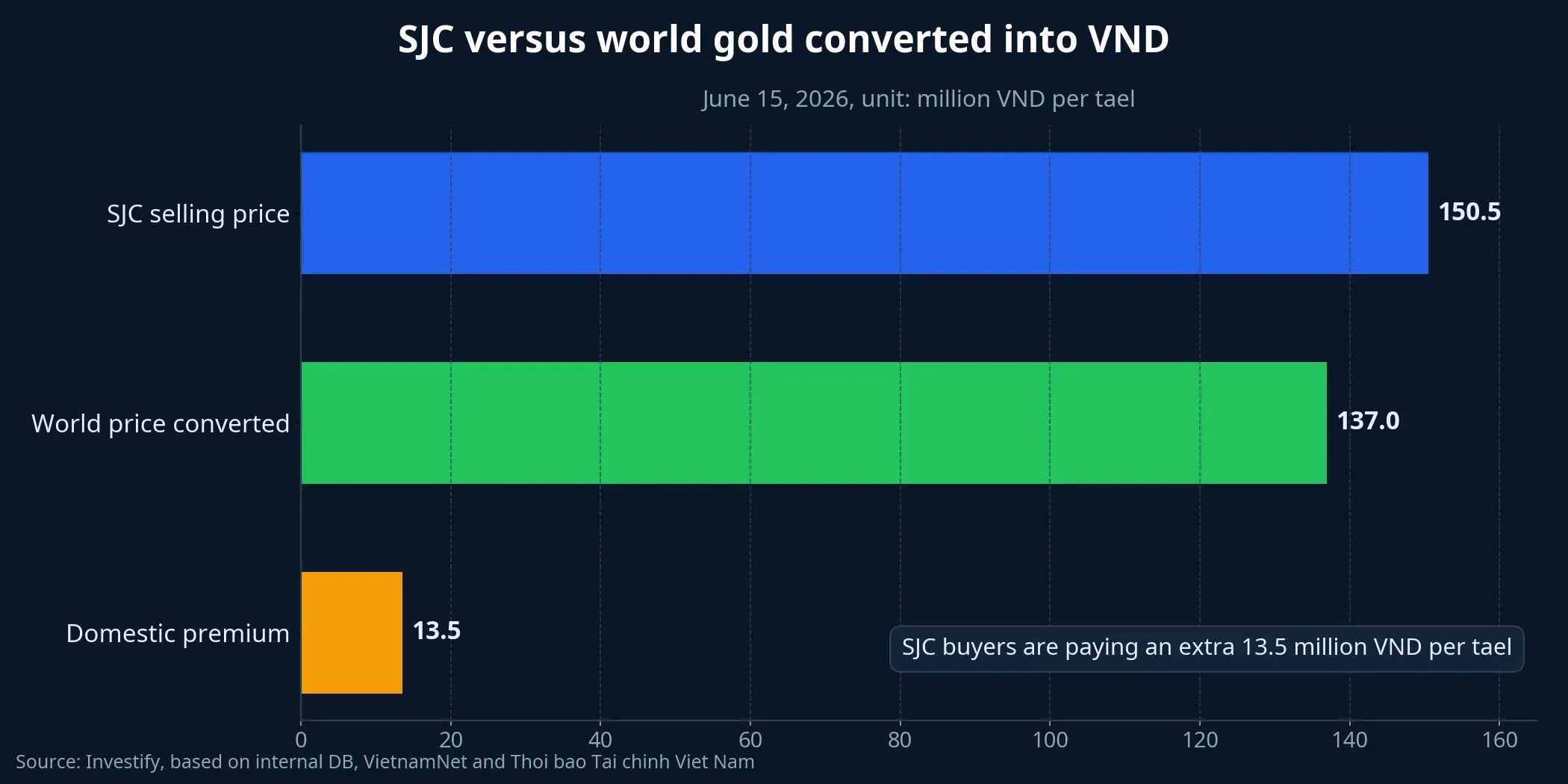

The first thing to separate is SJC gold from global gold. On June 15, Thoi bao Tai chinh Viet Nam reported spot gold at about USD 4,302 per ounce, which translated into roughly VND 137 million per tael using Vietcombank’s exchange rate, before taxes and fees.Thời báo Tài chính Việt Nam On the same day, VietnamNet put SJC’s selling price at VND 150.5 million per tael.VietnamNet

That leaves a gap of about VND 13.5 million per tael based on the banking exchange-rate reference used in the source article. The point is not whether the premium is exactly VND 13.0 million or VND 14.0 million. The point is that an SJC buyer is paying for a distinct domestic layer on top of global bullion pricing. That layer reflects local supply, distribution, trading points, and the long-standing preference for physical gold among Vietnamese households.

So when investors ask whether SJC above VND 150 million per tael still makes sense with global gold near USD 4,300 per ounce, there are really two questions underneath. One is about the international gold price, which is the base layer. The other is about the domestic premium, which is what determines whether a new buyer is overpaying for safety.

If you only watch global gold, it is easy to assume you are buying the same defensive asset that an international investor is buying. In practice, SJC in Vietnam comes with a meaningful local markup. That does not automatically make it a bad asset. It simply means future upside has to cover that premium, rather than relying on the assumption that any rise in global gold will flow straight through.

The buy-sell spread is an immediate cost

One of the most common mistakes new investors make is focusing on the quoted selling price and ignoring the buy-back price. On June 15, VietnamNet reported SJC at VND 148 million per tael on the buy side and VND 150.5 million on the sell side.VietnamNet That VND 2.5 million spread is the cost of entering the position, and it is paid immediately.

Put differently, if you buy now and need to sell right away, you are almost certainly taking a loss because the price has not had time to rise enough to offset the spread. Equity investors are used to thinking in marked-to-market terms, so trading costs feel visible. With physical gold, the cost is often hidden behind the emotional comfort of holding something tangible. But in cash-flow terms, it is still a real entry bill.

That is why SJC at VND 150.5 million per tael is no longer a straightforward “buy and you are safe” story. It is a defensive asset with a high ticket price. Anyone choosing gold at this level needs one very specific conviction: that the comfort gold provides is worth more than the premium and spread being paid today.

This is also where it helps to distinguish between preserving wealth and parking cash. If the goal is to hold part of your wealth outside the financial system as insurance against larger shocks, gold still has a clear role. If the goal is simply to keep cash aside for a few months, a VND 2.5 million buy-sell spread makes gold much less efficient than many first-time buyers assume.

Defensive does not mean stable

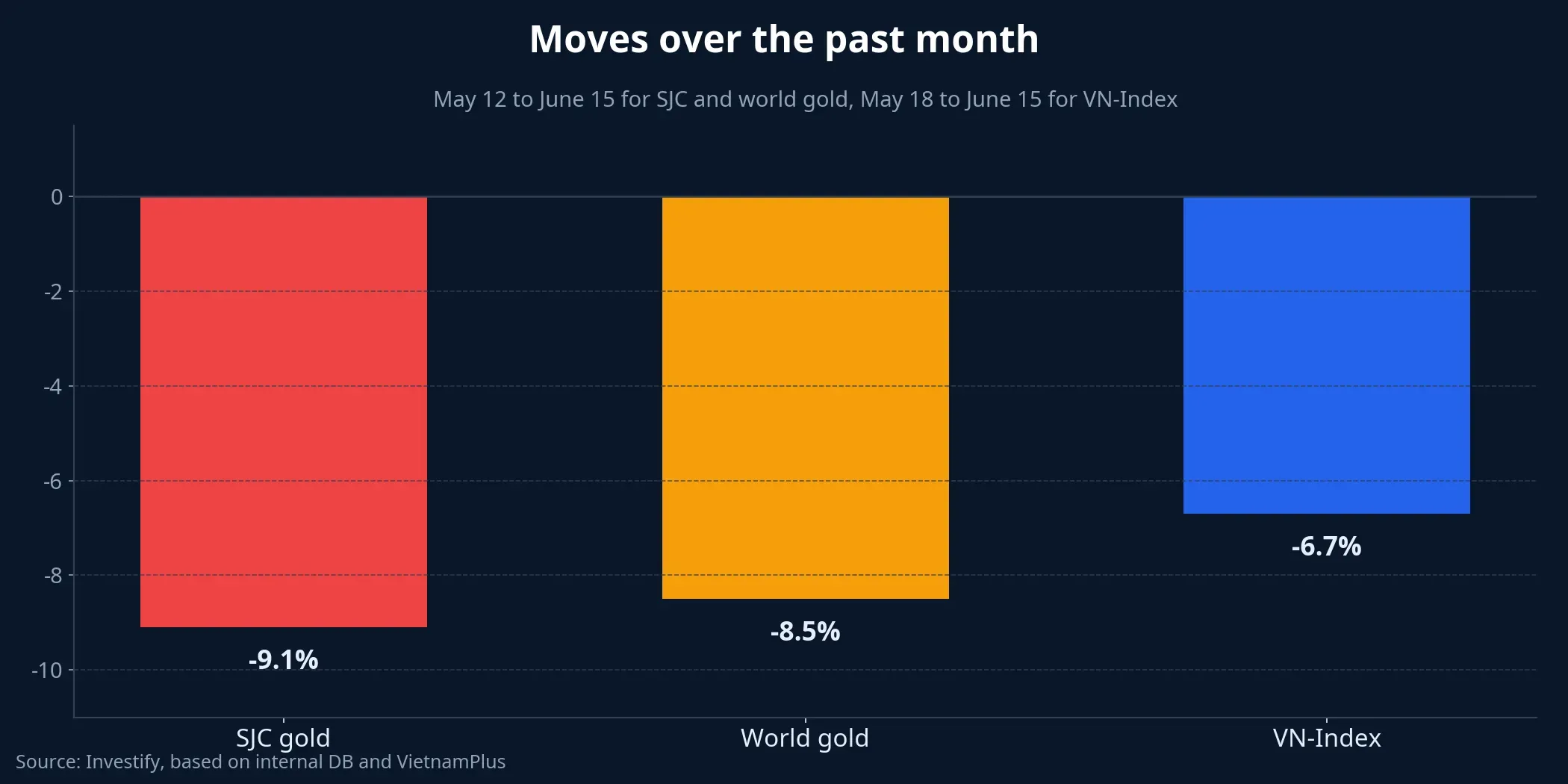

Another important point is that a defensive asset is not the same thing as a static asset. The internal data referenced in the source article shows SJC’s selling price falling from VND 165.5 million per tael on May 12 to VND 150.5 million on June 15, a drop of about 9.1% over a little more than a month. Over the same period, global gold fell from USD 4,715.13 per ounce to USD 4,314.18, or roughly 8.5%. The VN-Index was also about 6.7% below its 1,927.94-point level on May 18.

That matters for beginners. Many people choose gold because they want to avoid stock-market swings, but gold has its own volatility and can fall quickly when global pricing resets or when the domestic premium narrows. The difference is mostly psychological. Gold may shield you from watching a flashing trading screen, but it does not remove price risk from the asset itself.

From a personal balance-sheet perspective, gold can still reduce anxiety in uncertain periods. But reducing anxiety is not the same thing as removing downside. The higher the entry price, the more disciplined investors need to be about the possibility that gold does not keep moving in a straight line.

Bank deposits offer a different kind of comfort

If the real objective is simply to park money for one to three months, bank deposits now have an advantage that gold does not: the outcome is broadly knowable if the term is held to maturity. Techcombank’s June 12, 2026 rate summary shows many banks offering around 2.1%-4.75% per year for one-month deposits, 2.4%-4.75% for three-month deposits, and up to 7.1% for six-month deposits at some institutions.Techcombank

That does not make deposits the most exciting return vehicle. What it does mean is that deposits offer a kind of clarity that new investors often underestimate. You can estimate the outcome upfront instead of waiting for future price appreciation to cover a buy-sell spread the way you do with gold. It is a quieter kind of comfort, but a more transparent one.

At 4.5% per year, a VND 100 million three-month deposit would generate roughly VND 1.125 million in nominal interest before bank-specific terms. That is not a large return. But it is an expected return you can calculate on day one. By contrast, an SJC buyer first has to recover the VND 2.5 million spread before real gains even begin to appear.

In that sense, gold is better suited to people who want protection against bigger uncertainty and want part of their wealth in physical form. Deposits are better suited to those who want to park money for a short period, map cash flows in advance, and avoid paying a high upfront spread. Both serve a safety instinct, but they are not selling the same product.

Equities still need confirmation

The last part of the comparison is equities. The VN-Index closed June 15 at 1,799.31 points, up 7.66 points from the previous session, but still only near the 1,800 threshold rather than clearly above it.VietnamPlus That means a recovery path is reopening, but not yet with enough strength to call it a fully confirmed trend.

So the gold-versus-equities comparison should not be framed as a question of which side is guaranteed to win. Each asset is solving a different problem. Gold is solving for defense when investors do not want major downside surprises. Equities are solving for capital growth, but only if the market can show stronger flows and a more durable rebound.

For a new investor, that calls for discipline rather than excitement. If the index has not clearly reclaimed 1,800, equities are still a conditional opportunity rather than an automatic destination for idle cash. On the other hand, if the market breaks above that level decisively with solid liquidity, the opportunity cost of sitting in gold or deposits will become much more visible.

Conclusion: gold still has a place, but it is no longer cheap

At VND 150.5 million per tael, SJC gold still fits investors who want part of their wealth in a tangible asset and are willing to pay for peace of mind. But the bill is now quite explicit: a premium of roughly VND 13.5 million per tael versus converted global gold, a VND 2.5 million buy-sell spread, and the risk that the domestic gap can narrow if market sentiment shifts.

That is why bank deposits look cleaner if the main goal over the next one to three months is simply to preserve cash value and know the likely outcome in advance. Equities deserve a higher priority only if the VN-Index can break clearly above 1,800 on a convincing move. SJC gold remains most logical when buyers understand exactly which layer of protection they are purchasing, and are comfortable with the price of that protection.

The next two weeks offer a simple watch list. First, does the SJC premium versus global gold start to narrow. Second, do short-term deposit rates keep inching higher or stay flat. Third, does the VN-Index move through 1,800 with enough liquidity to suggest the recovery is broadening rather than merely testing resistance.