Nvidia has returned to the U.S. corporate bond market with a $25 billion deal, up from an initial target of about $20 billion after demand reportedly reached $85 billion. It is also the company’s first corporate bond sale since 2021, with maturities stretching as far out as 2056.Yahoo Finance

At first glance, the headline sounds simple: why would the company at the center of the AI boom need to borrow more money. But that framing misses the real signal. Nvidia is not the interesting part because it borrowed. Nvidia is interesting because the market is starting to price the AI boom through the cost of long-duration capital.

What this deal is really saying

The structure of the deal matters more than the headline amount. Orders came in at 3.4 times the offered size, which suggests credit investors still see Nvidia as strong enough to absorb a very large financing without demanding an extreme risk premium.Yahoo Finance

That distinction matters for newer investors because stocks and bonds answer different questions about the same company. Equity investors are paying for growth expectations. Bond investors are asking something colder and more mechanical: if this company needs long-term capital, what yield do we require to lend it the money.

Reuters, via Yahoo Finance, said the proceeds are intended for general corporate purposes. That may sound broad, but broad is the point. It suggests Nvidia is trying to preserve flexibility in its capital structure rather than tie the proceeds to one narrowly defined use case.Yahoo Finance

Why the real issue is the cost of capital

The most useful way to read this sale is not as a one-off funding event. Companies borrow for many reasons: refinancing, extending debt maturities, expanding capacity, or simply taking advantage of favorable market conditions. In Nvidia’s case, the available evidence points more strongly to a different conclusion. The company appears to be helping the market establish a clearer benchmark for its own funding costs as AI moves into a capital-intensive infrastructure phase.

Put plainly, Nvidia used to be judged primarily on chip revenue, margins, and shipment momentum. But when AI stops being just a software and model story and becomes a story about servers, memory, power, networking, and data center buildouts, competitive advantage no longer rests only on technology. It also rests on access to long-term funding at a tolerable price.

That is the layer many retail investors miss. The larger the growth cycle, the more capital analysis matters. Once a company has to sustain heavy investment over multiple years, even a modest shift in borrowing spreads can change return on capital, valuation discipline, and the durability of the growth story.

Nvidia is not an isolated case

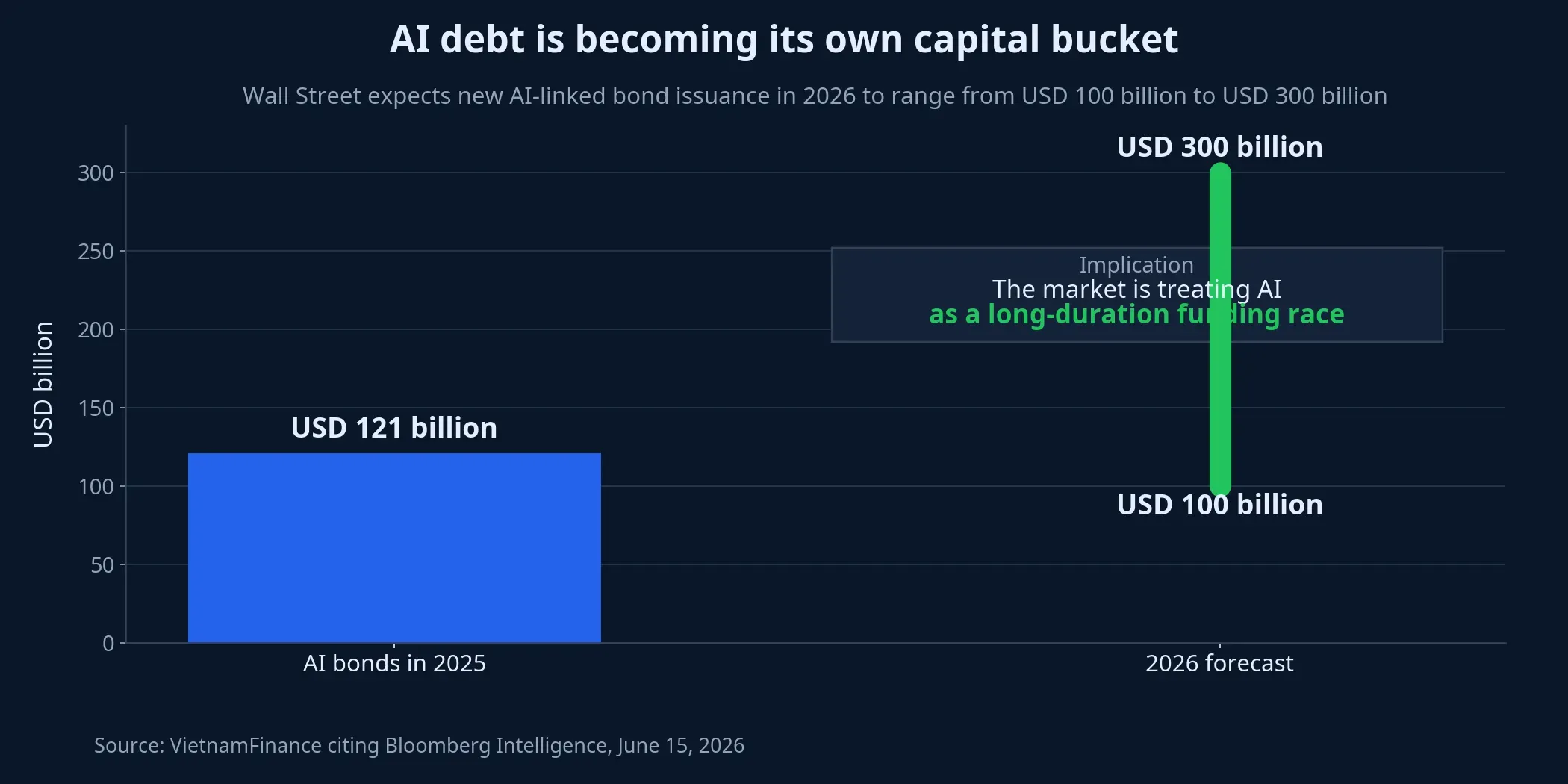

The broader backdrop shows that Wall Street is increasingly funding AI as an infrastructure buildout rather than just a stock market theme. VietnamFinance, citing Bloomberg Intelligence, reported that five major technology companies issued about USD 121 billion of corporate bonds in 2025, far above the roughly USD 28 billion average seen in the prior period.VietnamFinance

The shift is not only about headline volume. AI-linked debt now accounts for about 15% of the broader corporate bond market, while technology’s share of the investment-grade credit market has climbed from below 2% in 2005 to around 10% today.VietnamFinance That tells investors something important: AI is no longer being financed mainly through equity excitement. It is increasingly building its own capital stack in the bond market.

Wall Street is now projecting that new AI-related bond issuance in 2026 could land somewhere between USD 100 billion and USD 300 billion.VietnamFinance That makes Nvidia’s deal less of an isolated event and more of a marker in a larger transition: AI is moving from a growth narrative to a funding race.

Why this is not automatically bad news

Retail investors tend to overreact to borrowing headlines in two opposite directions. One camp assumes new debt means financial strain. The other treats strong bond demand as proof that the stock itself remains a one-way bet. Neither reaction is disciplined enough.

The first interpretation is weak because a deal that drew USD 85 billion of orders does not look like a market response to a borrower under immediate financial suspicion.Yahoo Finance The second interpretation also goes too far because the bond market and the stock market are not paying for the same thing. Bondholders care first about whether future cash generation can cover interest and principal. Equity holders care about how much growth remains after the company has paid for that capital.

In other words, strong demand is a positive signal about market access. It does not automatically prove that Nvidia will deploy that capital more efficiently than rivals. To make that call, investors still need more evidence on infrastructure returns, enterprise AI demand durability, and the path of U.S. yields over the next few quarters.

The core thesis for investors

The most important takeaway is a change in analytical lens. Nvidia is still central to the AI infrastructure trade, but the market is starting to evaluate the company not just as a high-growth chip supplier, but as a large-scale borrower. Once that shift happens, the stock’s valuation becomes more tightly linked to capital structure discipline.

This is also where counterfactual discipline matters. There are at least three plausible readings of the deal: Nvidia is taking advantage of receptive credit markets, it wants extra balance-sheet flexibility, and debt investors still believe the AI buildout can absorb huge amounts of capital. The second and third explanations fit the available evidence best. But it would still be a stretch to declare, with certainty, that this deal alone proves a new investment supercycle for Nvidia without more operating evidence behind it.

The most coherent thesis today is this: the USD 25 billion bond sale does not weaken Nvidia’s story, but it does show that the story has entered a more mature phase. From here, the market will not only ask how fast Nvidia can grow. It will ask how much capital that growth requires, what price the company must pay for it, and whether the spread between returns and funding costs stays wide enough to justify premium valuations.

That is why the signals worth monitoring next are not just day-to-day stock moves. The real watch list is the ease of future fundraising, the spread debt investors demand from large AI issuers, and whether 2026 AI bond supply ends up closer to the low end or the high end of the USD 100 billion to USD 300 billion forecast range.VietnamFinance If those variables remain supportive, Nvidia stays on the favorable side of the cycle. If they worsen, the market will start revaluing the AI boom through a harsher metric: the cost of capital.