Vietnam’s largest listed developer has just said it has enough land. That sounds counterintuitive in a market where investors have long treated a swelling landbank as the clearest marker of strength. But Vinhomes’ June 16 message does not read like a retreat. It reads like a change in emphasis: away from collecting more land and toward extracting more value from every square meter already on the books.CafeF

When Phạm Thiếu Hoa, Chairman of Vinhomes Joint Stock Company (VHM), said the company would completely stop expanding its project landbank in Vietnam under the direction of Phạm Nhật Vượng, Chairman of Vingroup Joint Stock Company (VIC), the key word was not “stop” by itself. The more important part came right after it: Vinhomes said its current landbank is sufficient for 5-7 years of continuous development, and that the next priority is to raise quality and value added per square meter of project area.CafeF

When “enough land” becomes a strategic choice

The simplest way to read this is to treat landbank like raw material inventory. A deep inventory matters, but it only turns into money when the developer can convert it into projects with approvals, infrastructure, buyers, handovers, and recurring activity. If the raw material already covers the next several years, buying more stops being the first priority.

CafeF reported that as of the end of 2025, Vinhomes held a 29,500-hectare landbank, which management considers enough for 5-7 years of continuous development. The same article also noted that Vinhomes has brought 6 new projects to market in just over a year. That points to a business that is not short on things to build. The harder question is how quickly it can turn its existing landbank into saleable and deliverable product.CafeF

This is also where newer investors can misread the signal. A halt to new land acquisitions can easily be framed in two extreme ways: either the company is pulling back because the market is weak, or it is so dominant that it no longer cares about expansion. The available evidence supports a third reading more strongly. Vinhomes says operations remain normal, its project pipeline is already deep enough, and management now wants to concentrate resources on the part of the cycle that matters most: executing faster and monetizing more reliably.CafeF

From landbank scale to execution quality

Owning land is the ticket into the game. Delivering projects is how a developer scores. Vinhomes can say it has enough because it already controls a large project inventory. But the market does not pay for inventory on paper forever. It eventually asks harder questions: which projects are close to launch, what can be handed over, and how much cash can come back this year.

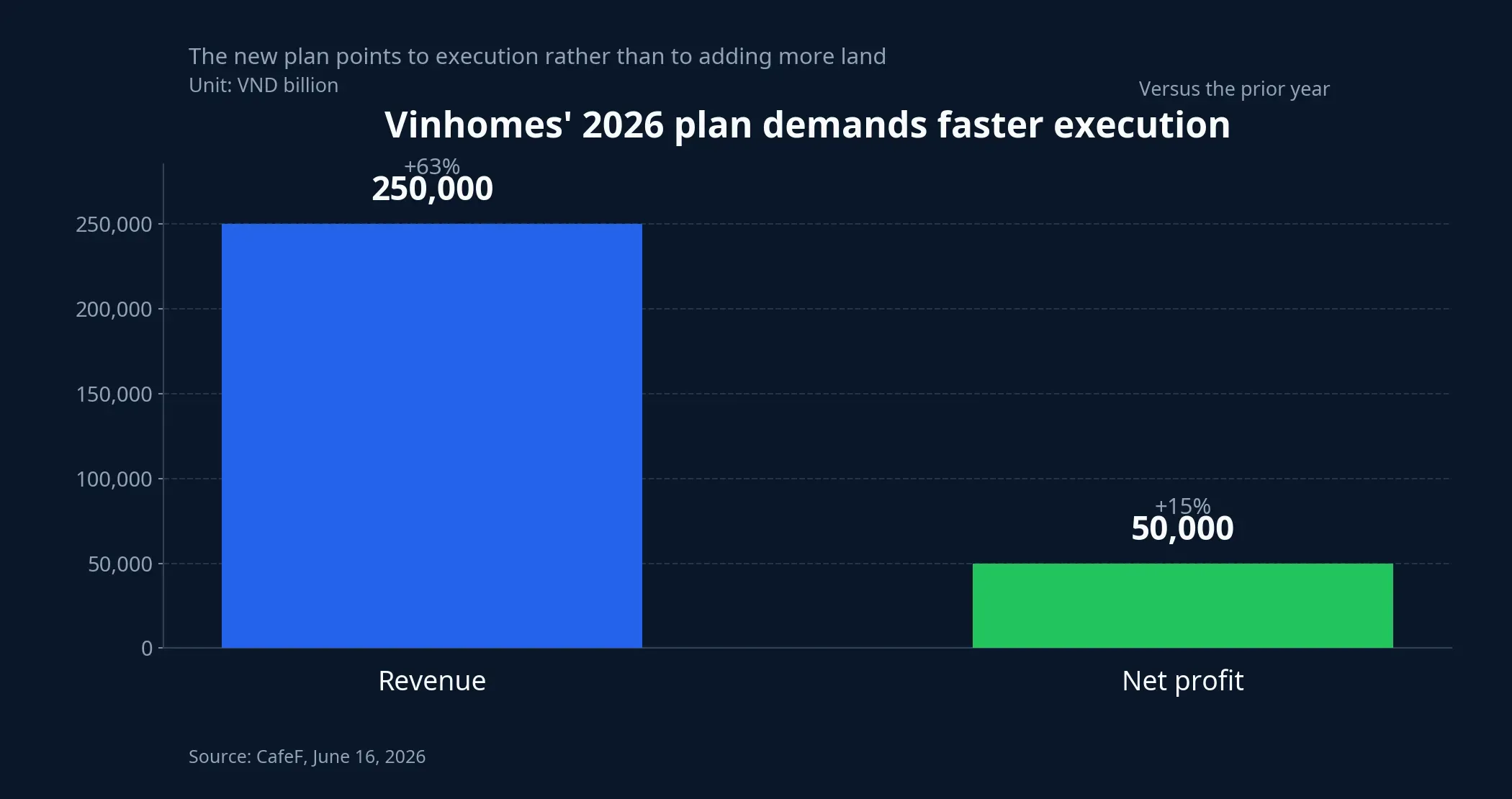

That is why the 2026 business targets matter so much in interpreting the new message. CafeF says Vinhomes is targeting VND 250 trillion in revenue and VND 50 trillion in net profit this year, up 63% and 15% from the prior year. A plan of that size cannot be delivered by telling a bigger land story. It requires approvals, construction progress, well-timed launches, and profit recognition from projects that already exist.CafeF

For retail investors, that is the key shift to remember. In an earlier phase of the market, when expansion stories carried more weight and the cost of capital was scrutinized less aggressively, a large landbank could itself support valuation. In the current phase, a landbank is only a starting condition. What matters next is whether the developer can turn that land into neighborhoods with residents, functioning amenities, and steady cash inflows. The same square meter can create very different value depending on how well it is executed.

This is also why Hoa’s comment should not be read as a bearish statement about growth. Growth can still happen. What changes is the engine of that growth. Instead of adding more input assets, the company is trying to squeeze more output from the assets it already controls. For newer investors, that changes the checklist. The better question is no longer just how many hectares remain. It is which projects are execution-ready, how fast they can be launched, and whether handovers are converting into cash on schedule.

Capital is still available, but no longer cheap enough for sprawl

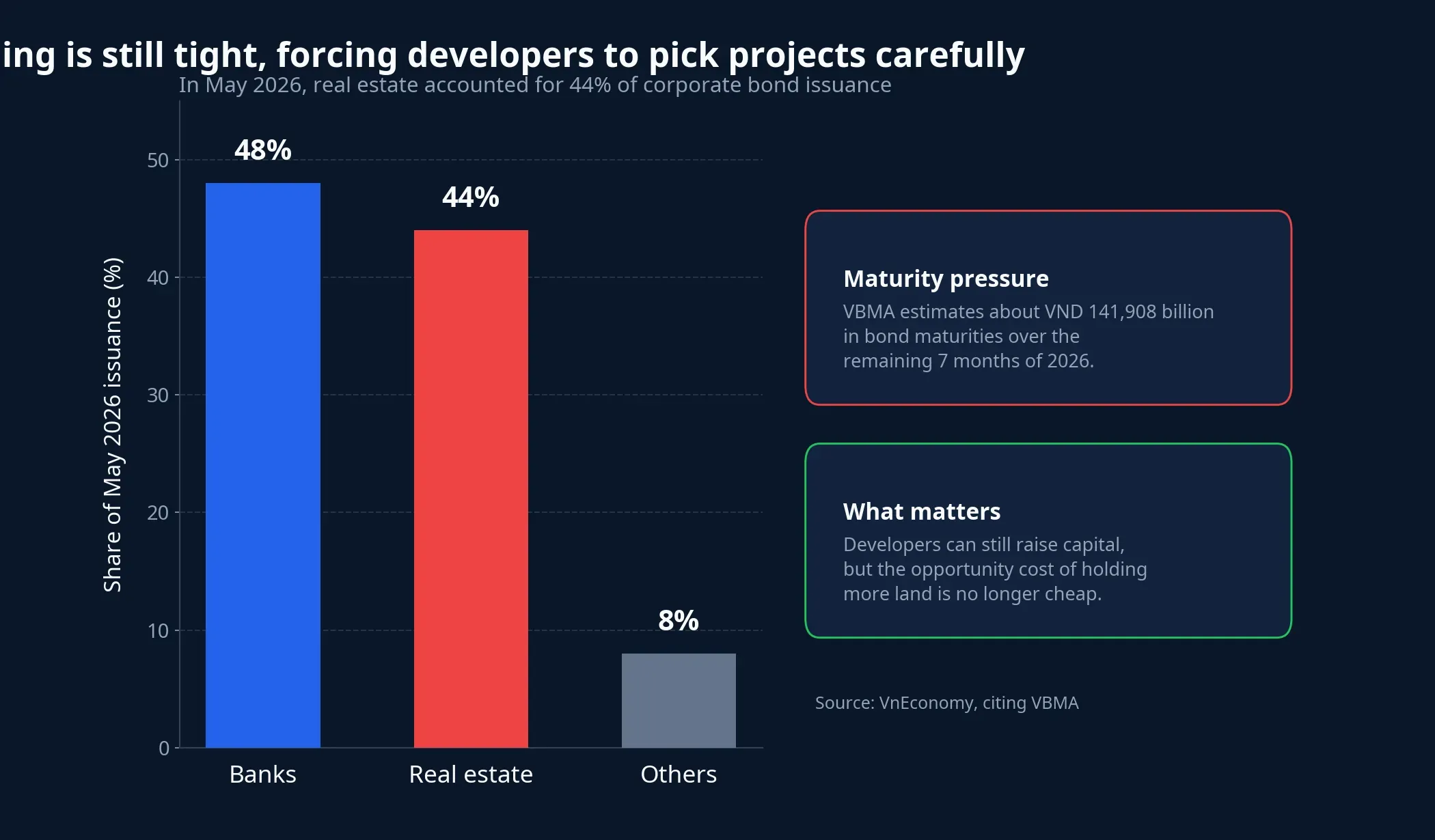

If you look only at Vinhomes, this can seem like a company-specific choice. The wider funding backdrop suggests something broader. VnEconomy, citing VBMA data, said real estate accounted for 44% of corporate bond issuance in May 2026, close to the 48% share of banks. At the same time, VBMA estimated roughly VND 141.908 trillion of bond maturities over the remaining 7 months of 2026.VnEconomy

That does not mean the funding window is shut. Developers are still raising money. But it does mean capital is no longer cheap enough for every company to warehouse more land and wait. When upcoming maturities remain large, every đồng tied up in a site that is still far from launch carries a clearer opportunity cost. For stronger companies, that is a reason to prioritize projects that can be converted into cash flow faster. For weaker ones, it can become a balance-sheet risk.

A caveat matters here. Not every developer will immediately follow Vinhomes, and stopping land accumulation is not automatically the right choice in every case. Some companies still need to expand because their current pipeline is too thin or poorly located. But with the evidence now on the table, Vinhomes’ move still looks like a clear signal that this phase of the market rewards capital discipline and execution capacity more than it rewards land accumulation for its own sake.

What newer investors should track next

For first-time investors, the lesson is not to start ranking developers by who owns the most land. The better habit is to read a landbank through the full cash-generation chain. A good landbank is not simply large. It has to move through approvals, infrastructure, launches, handovers, and ongoing operations. Only after that full chain does land turn into revenue and profit that show up in the numbers.

That is why three questions matter more than “how many hectares are left.” First, which projects are approaching launch or handover. Second, whether the company has enough resources to push those projects forward without stretching capital too thin. Third, whether the expected revenue story is matched by real cash conversion rather than by paper assumptions alone. In Vinhomes’ case, the June 16 message suggests management wants to concentrate much more heavily on the second and third questions.CafeF

The cleanest conclusion is this: Vinhomes is not stopping its land chase because it has run out of things to do. It is moving into a harder but more credible form of growth, where value no longer comes from adding more hectares, but from converting the hectares already owned into product, profit, and cash flow faster. The risks to watch are still approvals and market absorption, but they only overturn the thesis if they materially slow execution. Based on what management has just signaled, the core takeaway is clear: in Vietnamese real estate right now, execution efficiency is the real game.