On June 17, HoSE added FUEMITEC and FUEVN50G to the list of securities ineligible for margin trading. On the surface, that looks like a routine pre-market update ahead of the June 18 session. For new investors, though, it is a useful reminder that “margin cut” is not a one-size-fits-all warning. These two ETFs were excluded because they have not yet completed six months on the exchange, and their addition brought the total number of non-marginable securities to 68 as of June 16.CafeFCafeF

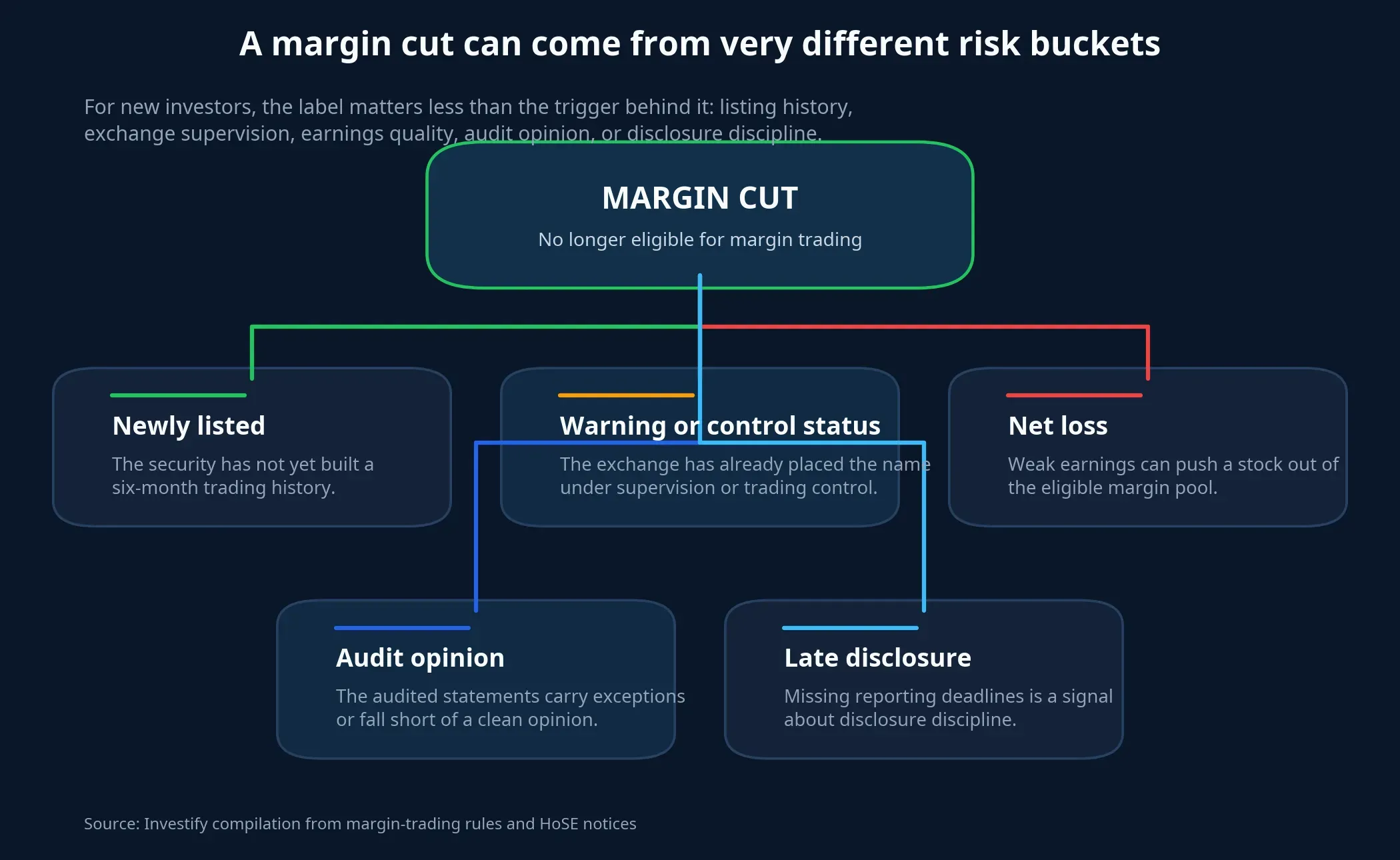

That distinction matters more than it seems. The same “not eligible for margin trading” label can point to a plain technical filter, or it can point to deeper concerns around disclosure, earnings quality, or exchange supervision. If investors fail to separate those buckets, they can overreact to a newly listed product while underestimating the warning signs around a stock already under tighter scrutiny.

Why the same label can mean very different things

Retail investors often think of margin as borrowed cash used to buy more stock or fund units. That is true, but incomplete. Margin is also part of how a broker calculates buying power, gauges account safety, and decides whether a security can sit inside the lending structure at all. That is why the first impact of a margin cut is not necessarily on price. It is often on how much you can still borrow and what kind of order you can still place.

Under Vietnam’s margin-trading rules, the initial margin ratio is set by the brokerage but cannot fall below 50%, while the maintenance ratio cannot drop below 30%. If an account’s margin ratio falls under the maintenance threshold, the broker may issue a margin call and require additional collateral within the requested period, up to three working days.Thư Viện Pháp Luật

Put simply, two securities may both be tagged as “margin cut” while sending completely different signals. One may be too new for the system to assess properly. Another may have already raised concerns around corporate quality or disclosure discipline. One is mostly about waiting for a trading history to build. The other deserves a much harder look at the underlying business and its risk profile.

The two newly added ETFs are a technical case, not a verdict

FUEMITEC and FUEVN50G were listed on HoSE on June 16 and then immediately appeared on the non-marginable list because they have not yet passed the six-month threshold.CafeF For first-time investors, this is exactly the kind of headline that invites the wrong takeaway. It is easy to see a fresh listing lose margin eligibility and assume something is wrong with the product. In this case, the trigger is mainly procedural and time-based, not a judgment on the ETF portfolio itself.

That matters because ETFs are often treated as an easier entry point for beginners. You can buy a fund certificate on the exchange just as you would buy a stock, but that does not mean every lending condition opens on day one. The margin system still needs enough trading history to observe liquidity, price behavior, and day-to-day stability. For newly listed products, a lack of margin eligibility should be read as a waiting period, not as a negative verdict on the fund’s structure.CafeF

But the broader 68-name list is not that simple

The 68-name non-marginable list as of June 16 is not made up only of fresh listings. CafeF reported that it also includes securities under warning or control status, including ABS, APH, BCG, DLG, DQC, HVN, LDG, NVT, OGC, TCD, TDH, TLH, VCA, and VNE.CafeF That is the split new investors need to see clearly.

If a security loses margin eligibility because it is newly listed, the core issue is limited trading history. If it loses eligibility because it has moved into warning or control status, the risk sits much closer to the issuer’s condition and disclosure record. Those are not cases that should be rolled into a single conclusion such as “margin cut means bad” or, at the other extreme, “it is just paperwork, so it does not matter.” The right reading is narrower: same label, very different signal quality.

Seasoned investors often process that difference almost automatically. Beginners usually do not, because the trading screen does not explain the reason. It only shows whether a name is still margin-eligible. The interpretation has to come from the exchange notice and from a second check inside the brokerage app.

The real impact shows up in buying power, not in the headline

Many new investors read a margin-cut notice as a direct bullish or bearish signal for price. A more practical first step is to look at buying power. If you plan to buy entirely with cash, a margin cut may not change your plan right away. The security can still trade normally as long as it has not been halted for some other reason. If you were planning to use borrowed funds, however, the story changes immediately.

A security that has just been removed from the lending list can make a planned margin-backed order fail even when your account looked funded the night before. In some cases, an existing holding may still count as collateral under a broker’s internal policy, but fresh buying power for that name will often be reduced sharply or shut off. That shift happens at the account-operations layer, which is why many investors only notice it once the order ticket says they no longer have enough available buying power.

The broader market was relatively calm on June 17, with the VN-Index closing at 1,806.20, down 0.10%. That calm backdrop is exactly why technical changes such as the non-marginable list are easy to dismiss. For accounts already using leverage, though, a small operational update can be enough to force a change in next morning’s trading plan even before the stock itself makes a big move.

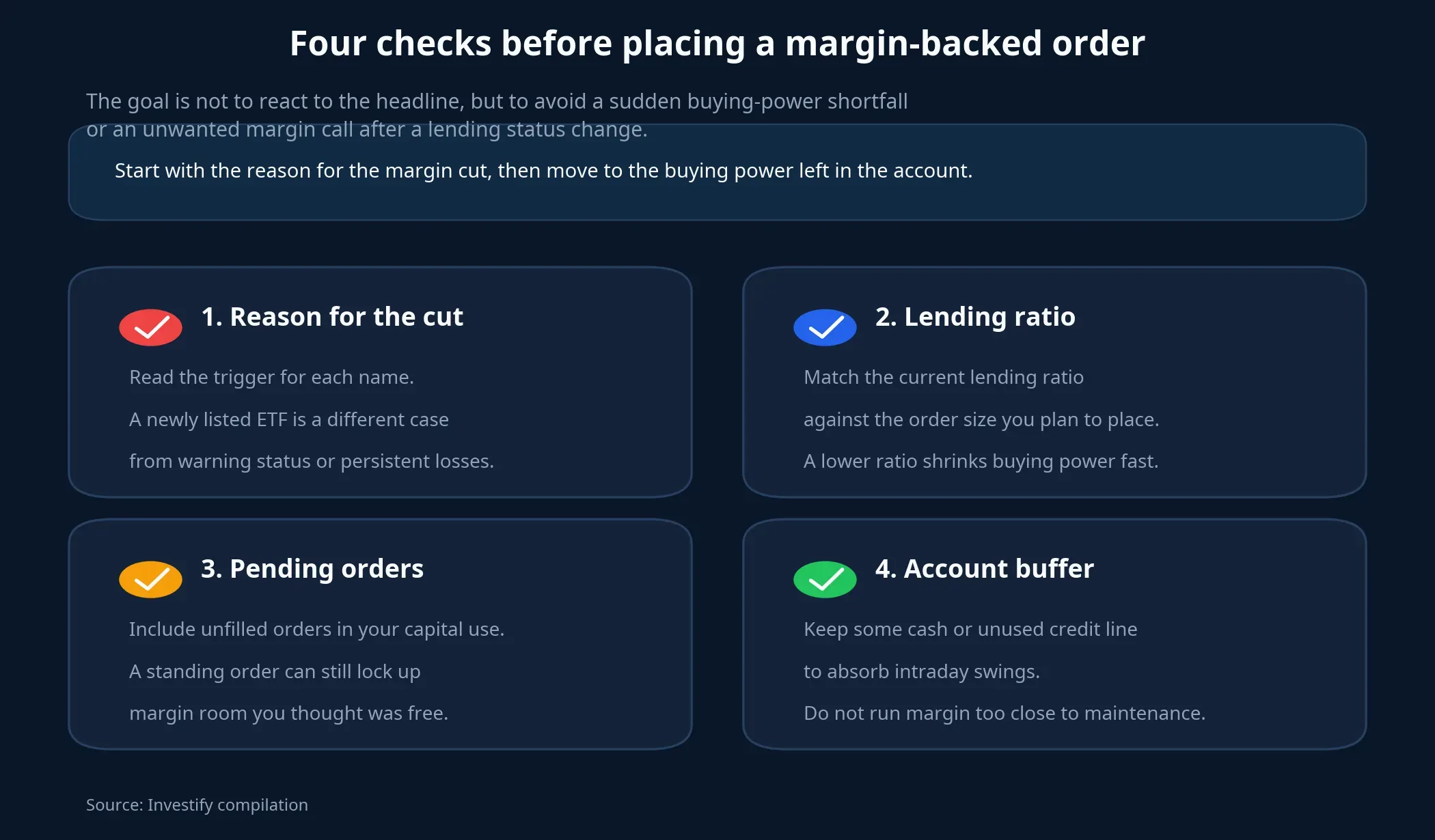

Four checks before the next session

The first step is to identify the actual reason a security lost margin eligibility. If the trigger is the six-month listing rule, the focus should be on liquidity and the waiting period before the product qualifies. If the trigger is warning status, control status, or disclosure problems, the focus needs to shift toward corporate quality and transparency.

The second step is to recheck the current lending ratio in the brokerage app. Do not stop at the account’s total buying power. An account can still show headline buying capacity while the amount available for the specific security you want to buy has already been reduced meaningfully after the lending list update.

The third step is to review any pending orders that have not yet been filled. This is where many beginners get caught. A standing order from the previous night can still tie up borrowing room you thought was free. Combined with a newly reduced lending status, that mismatch can leave you short of usable buying power right at the opening bell.

The final step is to preserve an account buffer. If you are already running leverage close to the maintenance threshold, even a small change in the lending ratio or an early-session dip can create margin-call pressure. That buffer is not a trading recommendation. It is a basic safety layer that helps keep the account from being forced into action when the market moves the wrong way.

Conclusion: React to the reason, not the label

This HoSE notice does not support a single sweeping judgment about all 68 affected securities. What it actually shows is that the margin filter operates across several layers of causes, from technical factors such as listing history to more serious signals such as warning or control status on the exchange.CafeF

That leads to a clean thesis for first-time investors: do not react to the phrase “margin cut” by itself. React to the reason the security lost eligibility and to the way that reason changes your own account’s buying power. Over the next few sessions, the more useful signal will not be whether the list gets a little longer or shorter, but which names are being added for technical reasons and which ones remain on the list because the underlying risk needs closer watching.