New investors usually experience the market through the screen: a green morning, a red afternoon, another headline-driven swing. But underneath that noise sits a deeper structural question: why does Vietnam’s capital market still lack a durable pool of money that can hold through multiple cycles. Supplemental pension funds matter because, by design, this is money that should not be trading every hot headline.

That pool is still tiny. By the end of 2025, Vietnam’s supplemental pension funds held only about VND 2,206 billion, or less than USD 88 million and under 0.01% of GDP, even as the country’s labor force had climbed past 50 million people.Thời báo TC The number is far too small to move the equity or bond market in any visible way today, but it highlights a structural gap the market still has not filled.

Why investors should care

Put simply, a market dominated by short-term money tends to overreact to interest-rate shifts, rumors, margin pressure and crowd psychology. A market with more insurance capital, mutual funds, pension assets and other institutional long-term investors usually has a steadier base of demand and less reliance on one trading session at a time.

That does not mean pension capital would eliminate volatility. Vietnam’s swings also reflect market depth, a retail-heavy investor base and the quality of listed companies themselves. But without a meaningful layer of long-duration capital, the market remains more vulnerable to short-term shocks than it needs to be.

That is why supplemental pensions are not just a retirement-policy story. They are also a market-structure story: whether companies gain a more natural buyer base for long-dated bonds, whether equities gain a more patient bid, and whether the economy’s cost of capital can become less expensive over time.

Nearly a decade in, the market is still very small

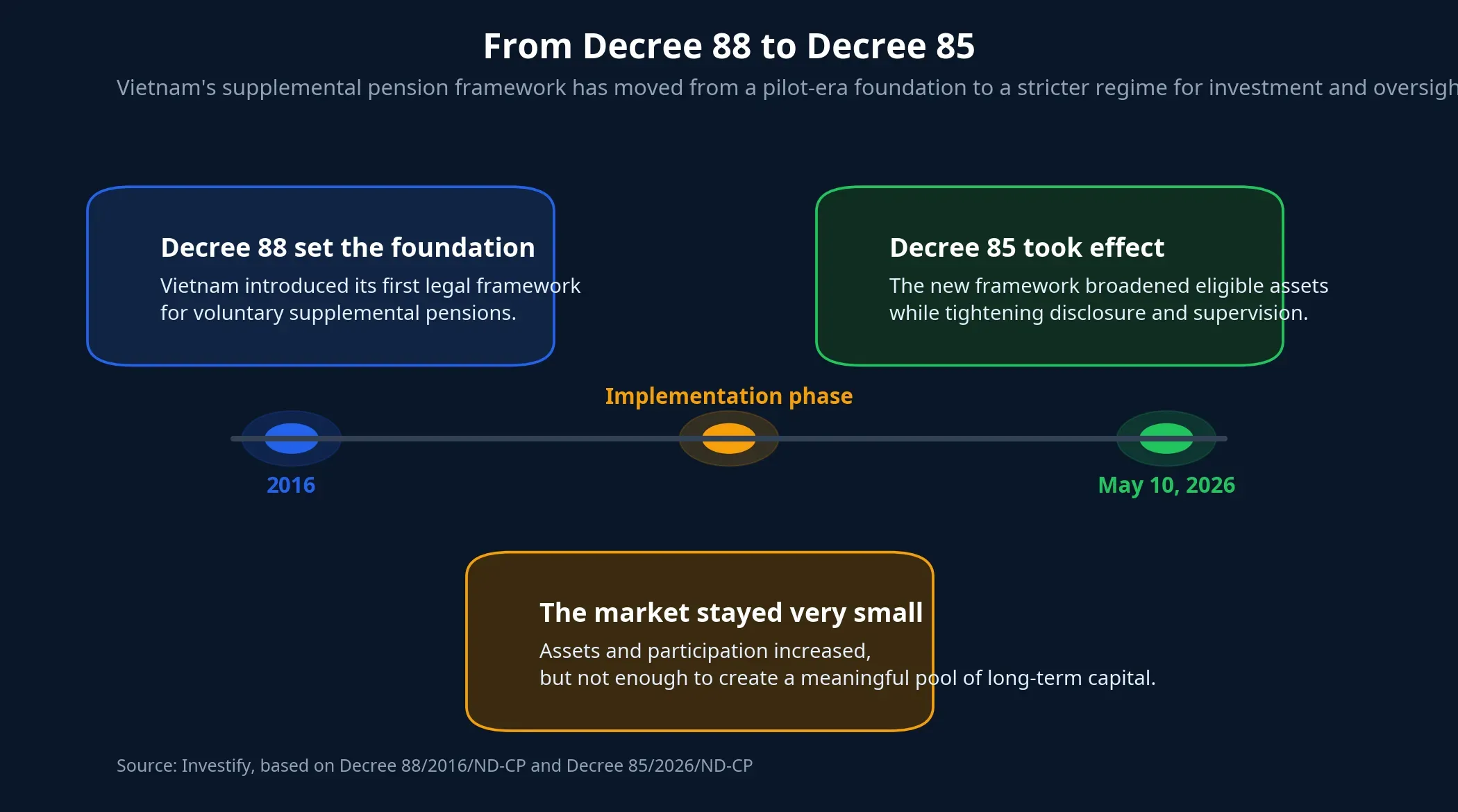

Vietnam’s first legal framework for voluntary supplemental pensions came with Decree 88/2016/ND-CP.Thư viện PL Since then, the market has had time to operate, yet penetration remains low relative to the needs of an economy that is still growing and beginning to age.

The first bottleneck is access. Under Decree 85, participation is structured through employers and applies to employers plus workers who are already part of compulsory social insurance, on a voluntary basis.Chính phủ In practice, that means this is not a product a freelance worker can open as easily as a brokerage account or a mutual fund app.

The second bottleneck is financial behavior. If workers are expected to lock away part of their cash flow for years, the product has to be simple enough to justify trading liquidity today for long-term accumulation tomorrow. In reality, Vietnamese households still compare everything against deposits, gold, property or direct stock investing, where value feels more visible and control feels more immediate.

What Decree 85 actually changes

Decree 85/2026/ND-CP was issued on March 25, 2026 and took effect on May 10, 2026.Chính phủ Its significance is not that it suddenly sends retirement money into stocks. The real shift is that it makes the supplemental pension framework look more like a supervised long-term investment product than a narrow pilot-era savings vehicle.

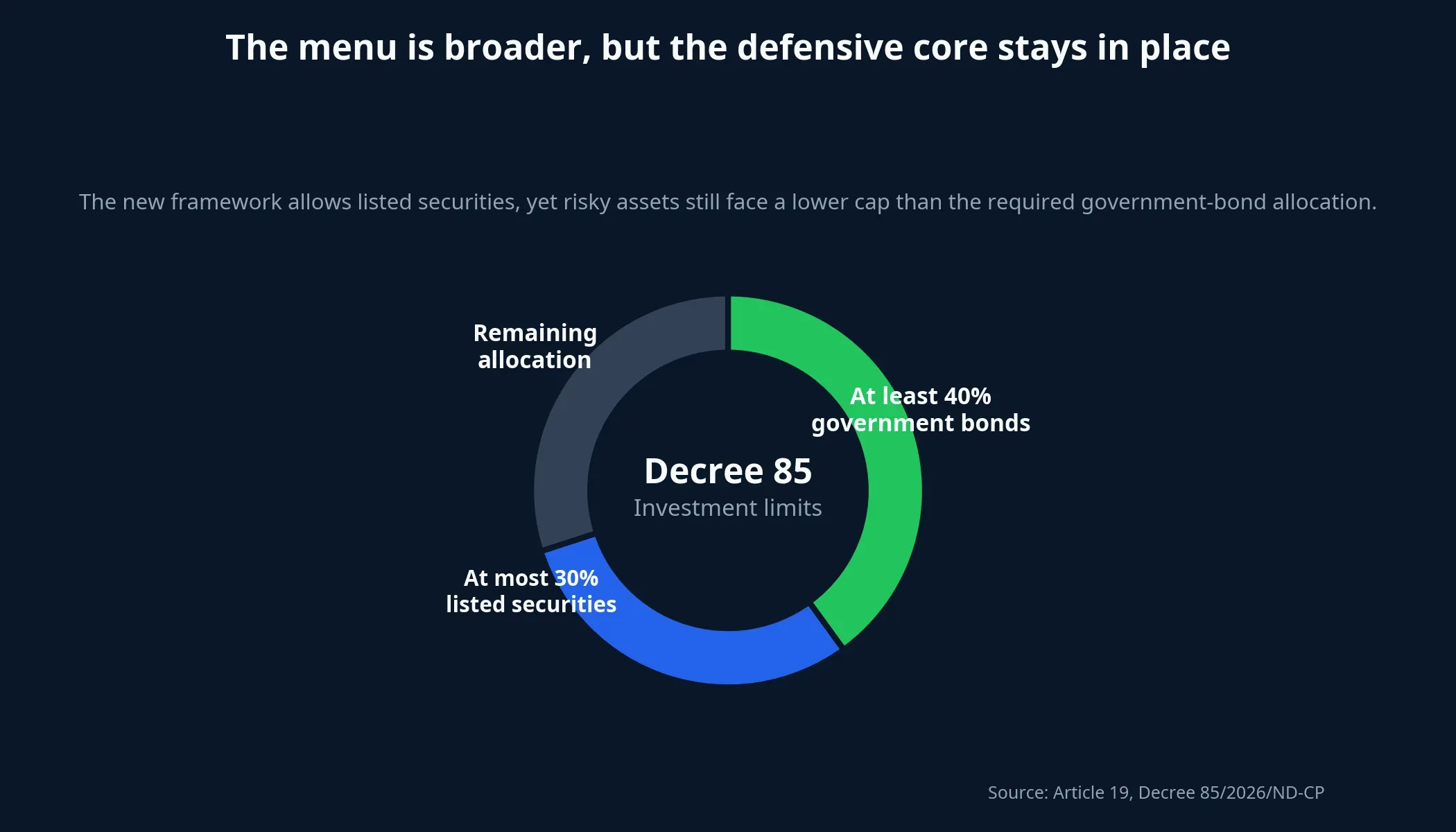

The biggest change is in the investment menu. Supplemental pension funds are allowed to invest in government debt instruments, local-government bonds, government-guaranteed bonds, bank deposits, bank bonds and certificates of deposit, listed equities, listed bonds and securities investment fund certificates.Chính phủ For many first-time investors, that matters because it means retirement assets are not confined to deposits. They can participate in the capital market, but within a much tighter risk framework.

Even so, the defensive core remains obvious. Any fund with net asset value of at least VND 5 billion must keep at least 40% in government bonds, while investment in listed securities, excluding public-sector debt instruments, cannot exceed 30% of total fund assets.Chính phủ That tells investors something important: policymakers are not designing pension funds as a direct stock-buying machine. They are designing them as a long-term pool of capital with safety first.

For retail investors, the implication is straightforward. If pension assets eventually grow, some money can flow into equities, but not at a sudden or aggressive pace. Any market support that emerges is more likely to be gradual and durable than speculative and abrupt.

Protection matters more than a promised return

A long-term product becomes credible only when participants trust that their assets are ring-fenced, supervised and reported clearly. Decree 85 requires pension fund assets to be accounted for separately from the assets of the fund manager.Chính phủ Balances in individual pension accounts also cannot be transferred, pledged as collateral or used in bankruptcy proceedings involving the fund manager, the supervisory bank or the custodian.Chính phủ

That is the part new investors should focus on more than any marketing promise about returns. A product can advertise attractive performance, but if the protection structure is weak, participants still cannot see where the real risk sits. When ownership rights are ring-fenced and assets are legally segregated, trust has a better chance to form.

The decree also requires the supervisory bank to monitor investment activity, trading and the value of each individual pension account. Fund managers must send monthly account-value reports within 10 business days after month-end, showing contributions, withdrawals and accumulated value after investment results and fees are allocated.Chính phủ That kind of repeated, understandable disclosure is what can move the product from being merely legal to being trusted.

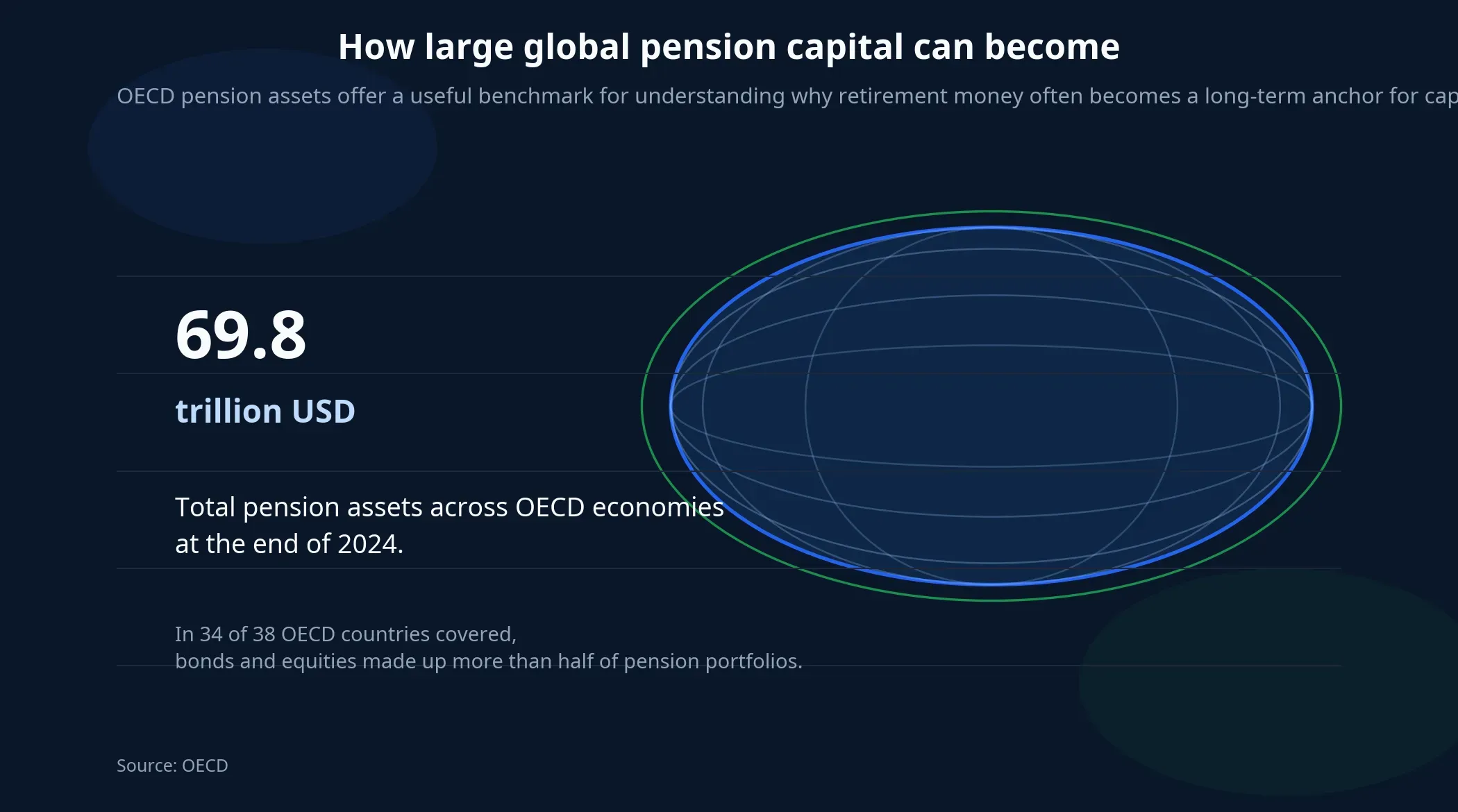

Looking abroad shows how large the gap is

International experience makes clear that pension assets are not a side pocket of the financial system. In many economies, they are one of the main pillars of long-term capital. The OECD says pension assets in member countries reached USD 69.8 trillion at the end of 2024, and in 34 of the 38 OECD countries covered, bonds and equities accounted for more than half of pension portfolios.OECDOECD

Vietnam obviously cannot copy markets that have compounded retirement savings for decades. Income levels, financial-product adoption and capital-market depth are different. But the underlying logic is the same: when workers contribute regularly over long periods, pension funds can invest with a horizon that is far longer than weekly or quarterly trading flows.

That is also why it would be too simplistic to say that the absence of pension money is the only reason Vietnam’s market remains volatile. The evidence does not support that leap. A more defensible conclusion is that pension capital is one of several missing layers; if it grows alongside insurance money and other long-term funds, the market’s structure becomes more balanced than it is today.

What is still missing after Decree 85

The new legal framework opens the road, but the road does not create traffic by itself. The first missing piece is employer adoption. Until more companies treat supplemental pensions as a real benefit used to attract and retain workers, the product will struggle to move beyond a relatively narrow group of higher-income participants.

The second missing piece is the value proposition for workers. They need more than a generic message about retirement security. They need to see how contributions accumulate, what the fee burden is, what happens when they change jobs, and why giving up some liquidity today is worth it.

The last missing piece is trust in execution. Vietnam does not lack regulation in financial products nearly as much as it lacks simple, regular and readable reporting habits. Supplemental pensions become real long-term capital only when participants can open a monthly report and understand where their money sits, why it moved up or down, and what protects them if the manager runs into trouble.

The thesis here is straightforward: Decree 85 is a necessary step forward, but it creates the rails for long-term capital rather than the capital itself. The indicators worth watching over the next few years are not a single up day in the index, but the number of participating employers, the number of new accounts and the pace of asset growth. If those three trends rise steadily enough, Vietnam’s market will finally gain a more patient layer of money to absorb difficult cycles.