When people read a bond headline, many stop at the phrase “successfully issued” and treat it as a positive signal by default. That instinct is understandable: if a company can raise money, it sounds as if the market has endorsed the business story. In private bonds, though, that is only half the picture.

Tandoland is a useful example of why investors need to slow down. The company has just completed bond lot TDR12601 worth VND 300 billion, with a 60-month tenor and a 12% annual coupon.CafeLand On the surface, that means the deal found buyers. It does not mean the company’s credit risk has become lower.

A successful issue only answers one question

The first thing to separate is the question the news report actually answered. Based on the disclosed information, Tandoland issued TDR12601 on June 4, completed the deal on June 5, 2026, sold 3,000 bonds with a face value of VND 100 million each, and set maturity for June 4, 2031.CafeLand So the question “did the company manage to raise money?” already has a clear answer: yes.

But bond investors are not supposed to stop there. Their first job is to ask where interest and principal will be paid from, and how much balance-sheet protection exists if the operating plan slips. Put simply, the article confirms that the fundraising worked. It does not settle the more important issue of how risky that debt still is.

There is also a basic discipline point here. The available reporting does not tell us exactly who bought the bonds or what their full motivation was. So it would be too much to say Tandoland raised the money because the project outlook is suddenly strong or because the market has broadly reassessed the company. The evidence only shows that some investors were willing to accept the risk at the current yield level.

A 12% coupon is not a gift, it is the price of capital

For new investors, a 12% annual coupon can look very attractive because it is far above deposit rates at Vietnam’s largest banks. In corporate bonds, however, higher yield is usually compensation for credit risk, liquidity risk, and information risk. A higher coupon does not make income safer by itself.

In Tandoland’s case, one of the clearest signals is that the new borrowing cost is higher than on its older outstanding bonds. VnBusiness reported that before TDR12601, the company still had three outstanding bond lots carrying 9.5% annual coupons, while the new lot came at 12% a year.VnBusiness In plain terms, Tandoland appears to be paying a higher price to access fresh funding.

That is not enough to prove the company has deteriorated further right now. Buyers may be comfortable with the collateral package, the project timeline, or private credit relationships that are not fully visible in public reporting. But based on the disclosed data alone, the best-supported reading is still that Tandoland’s cost of capital is elevated, not that the market suddenly sees the risk as lower.

This is also where many first-time investors confuse corporate bonds with “upgraded deposits.” Bank deposits sit behind a regulated banking balance sheet and a limited deposit insurance framework. A corporate bond is a direct loan to the issuing company’s financial condition. Reading 12% a year as a better savings product is one of the fastest ways for inexperienced investors to misprice risk.

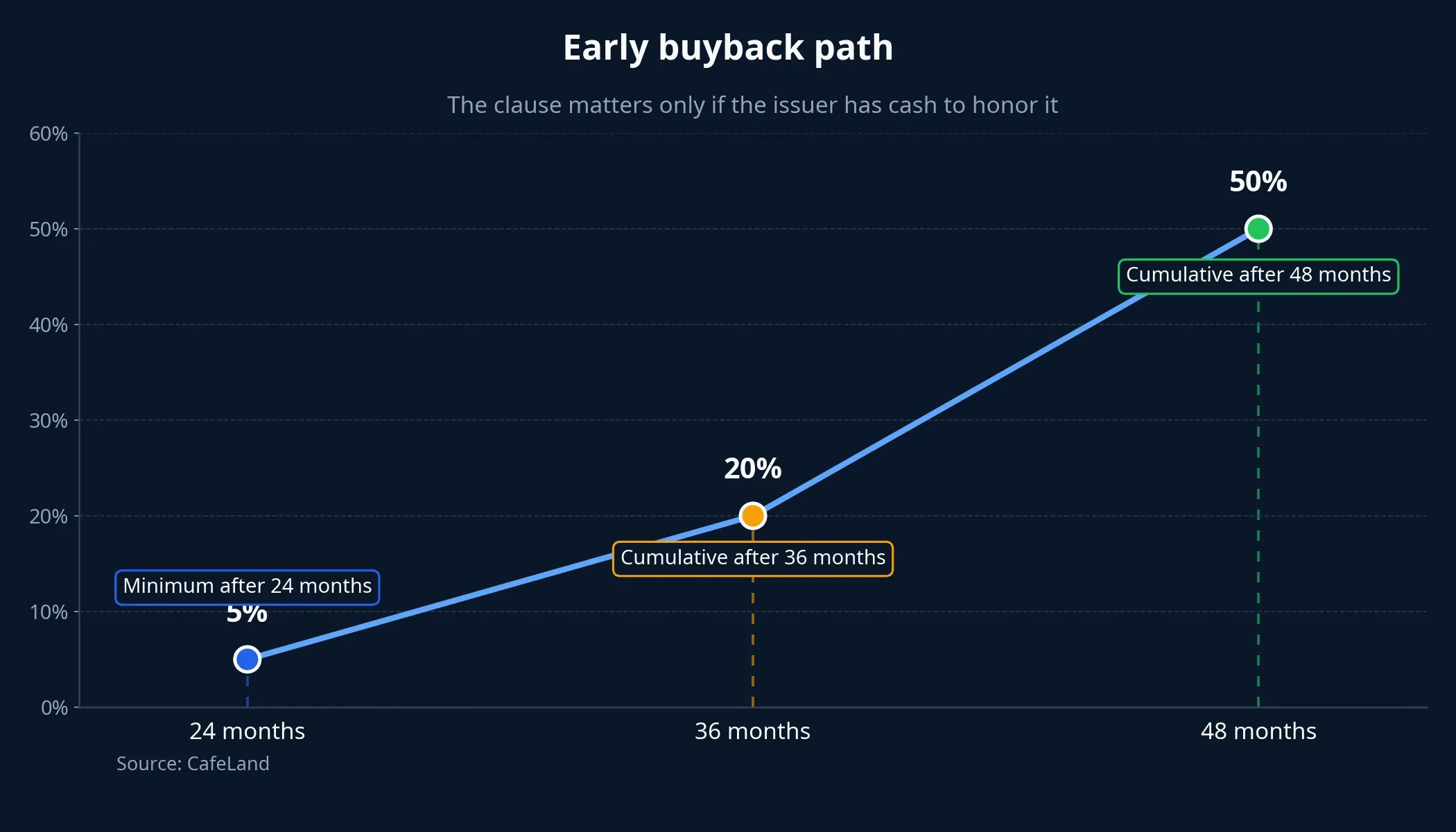

Early buyback terms help the structure, not the cash flow

Tandoland disclosed a fairly specific early buyback schedule: at least 5% of the bond volume after 24 months, 20% cumulatively after 36 months, and 50% cumulatively after 48 months.CafeLand For a new reader, that can sound comforting because it suggests bondholders do not have to wait until final maturity to start recovering capital.

That reaction is reasonable, but incomplete. Good terms are only the legal framework around investor rights. To turn those rights into cash, the issuer still needs the financial ability to perform. If project progress slips, leasing or monetization takes longer than expected, or other obligations move ahead in the payment queue, then a strong clause on paper still does not replace real operating cash flow.

The difference between “protective terms” and “capacity to honor them” matters a lot. Think of it like a rental contract with a very clear deposit refund clause. The tighter the contract, the clearer your rights are. But if the other side does not have cash when the refund is due, getting the money back is still not automatic. Private bonds work under the same logic.

The balance sheet is where the risk becomes visible

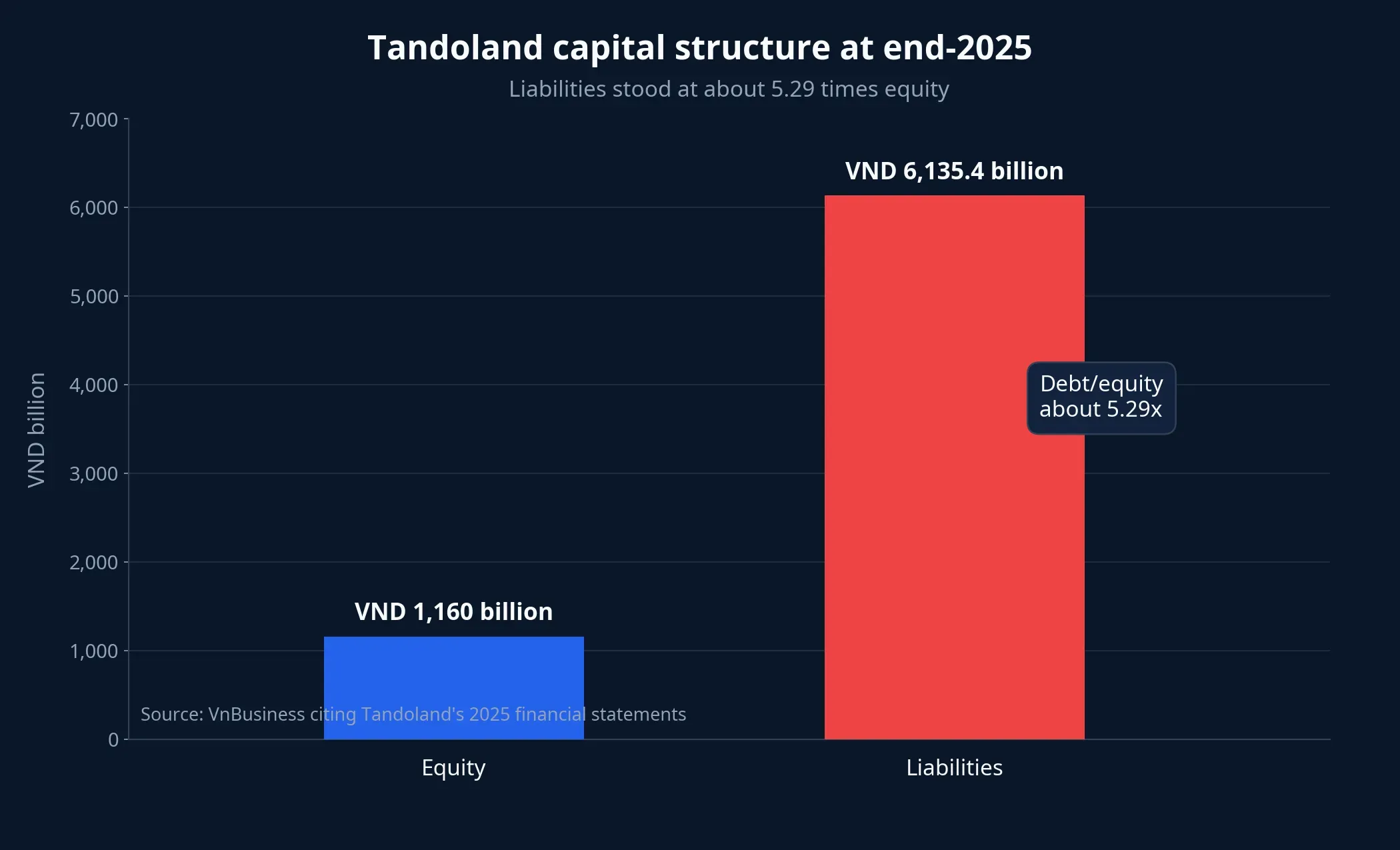

If investors skip the balance sheet, they may easily assume that a VND 300 billion deal is a sign of improving health by itself. But the financial data cited by VnBusiness from Tandoland’s 2025 statements points to a more cautious reading. The company posted a net loss of more than VND 29.2 billion in 2025, still carried accumulated losses of nearly VND 190 billion, and had total liabilities of about VND 6,135.4 billion at year-end.VnBusiness

At the same point, shareholders’ equity stood at about VND 1,160 billion. That means liabilities were roughly 5.29 times equity, while bank borrowings alone exceeded VND 3,521 billion, or about 57.4% of total liabilities.VnBusiness Put plainly, Tandoland is not just a bond borrower. It is already carrying heavy obligations to the banking system as well.

Those figures do not prove the company will run into trouble. What they do is change how the bond issue should be interpreted. When a company with accumulated losses and high leverage raises new debt, fresh cash often buys more time or funds the next stage of a project. It does not automatically make the balance sheet healthier on the day the bonds are sold.

A large project can support the story, but it also demands large capital

According to VnBusiness, Tandoland is associated with the Tandoland industrial park project in the former Long An area of Ben Luc, with a scale of around 250 hectares and total investment of more than VND 3,144 billion.VnBusiness That kind of project size helps explain why the company needs large funding and is willing to accept a high cost of capital to keep moving.

But large projects do not always convert into cash flow quickly. For an industrial infrastructure developer, the important questions are legal progress, site clearance, infrastructure build-out, and eventual occupancy. If those steps move more slowly than the schedule for coupon and principal payments, liquidity pressure remains even after a successful fundraising round.

So it would be too generous to frame this VND 300 billion deal as proof that Tandoland is now in better shape. A more disciplined reading is that the company still has access to capital. Whether that access leads to a more stable phase or merely extends debt pressure will depend on real cash generation in the coming quarters.

What new investors should take away

When you read a similar bond story in the future, three questions are enough to start with. How much interest is the company paying compared with its earlier issues. Is the balance sheet getting lighter or heavier over time. And does repayment depend on existing operating cash flow or mainly on a project story that still needs time to convert into money. Those three questions alone can stop investors from reacting to headlines emotionally.

For Tandoland, the core conclusion should stay clear: a successful placement shows that someone accepted the risk at a 12% annual coupon, but it does not show that the company’s credit risk has fallen. Until updated financial statements and project cash-flow progress point to clearer improvement, this VND 300 billion issuance should be read as a sign of funding access, not as a safety certificate for the bonds. The next data points worth watching are cash flow, debt levels, and project execution in upcoming disclosures.