Dividend stories are often read in the most direct way possible: how much cash is being paid, when the record date is, and whether shareholders are entitled to receive it. In the Vingroup ecosystem, that reading only gets you through the first layer. The more important layer is how cash is moving between listed subsidiaries and the parent company, especially when Vinhomes is paying enough to change how the market thinks about VIC’s capital flexibility.

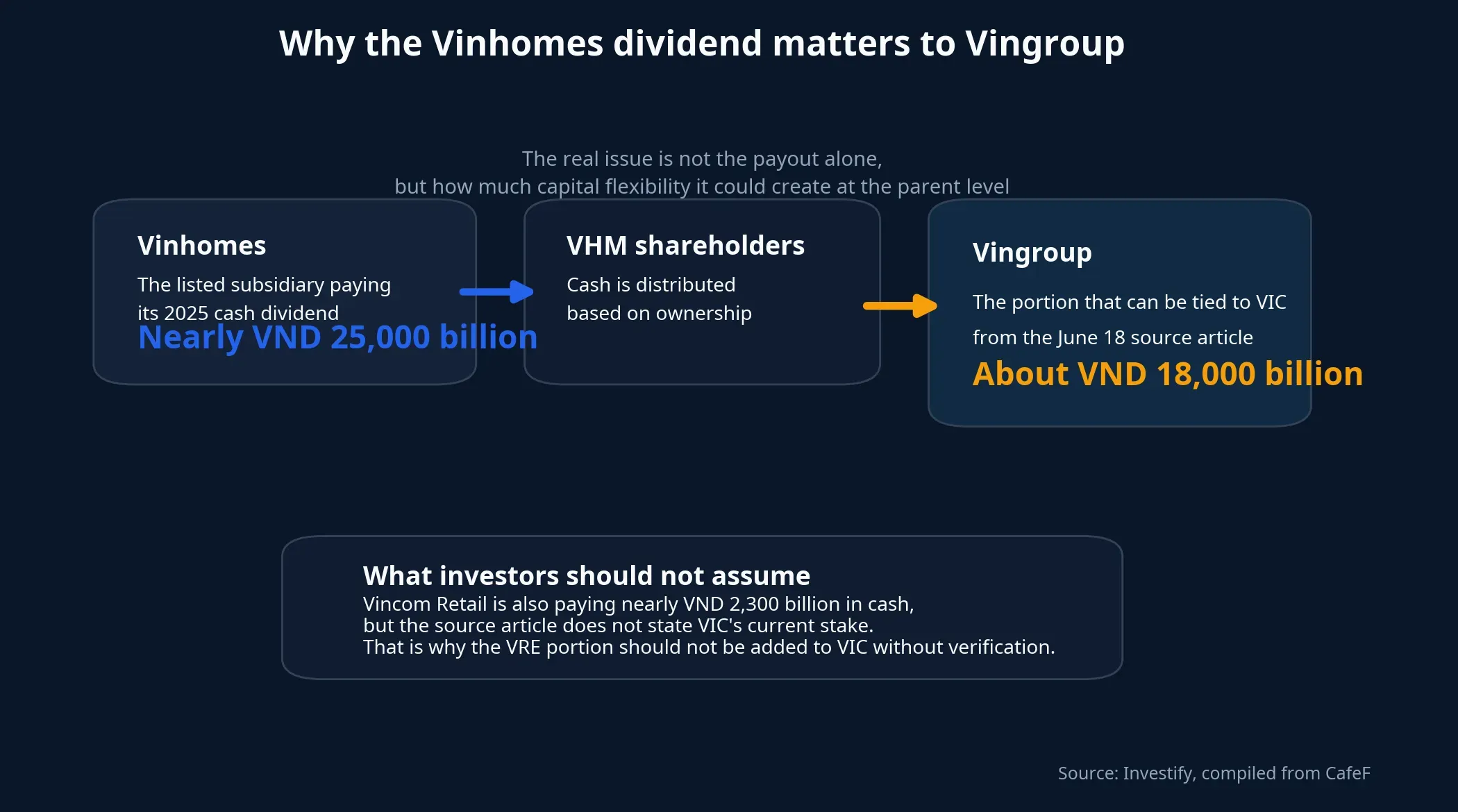

CafeF reported on June 18 that Vinhomes will close its shareholder list on June 30 for a 2025 cash dividend equal to 60% of charter capital, or VND 6,000 per share. With roughly 4.1 billion shares outstanding, the company is set to pay nearly VND 25,000 billion in cash. The same report says Vingroup owns 72% of Vinhomes, implying that about VND 18,000 billion could flow back to the parent from this payout.CafeF

A dividend story with two readings

On the numbers alone, this is a very large payout cycle compressed into a fairly tight window. CafeF also reported on June 18 that Vincom Retail will pay a 2025 cash dividend of 10%, or VND 1,000 per share, with a total value of nearly VND 2,300 billion. Its final registration date is July 1 and the expected payment date is July 22.CafeF

If you add the corporate payout sizes together, the market is looking at roughly VND 27,300 billion being distributed across the two companies. But newer investors need to separate the amount being paid by the subsidiaries from the amount that can actually be tied back to VIC. Those two figures are related, but they are not interchangeable.

A cash dividend is not free money appearing out of nowhere. Cash leaves the subsidiary and is redistributed to shareholders according to ownership. For retail investors, that means money hitting their account. For a controlling shareholder such as Vingroup in Vinhomes, it can also mean more flexibility at the group level: less short-term funding pressure, a thicker liquidity buffer, or more options for the next capital-allocation decision.

What can truly be linked back to VIC

This is where discipline matters. It would be easy to collapse the Vinhomes and Vincom Retail stories into the line that “VIC is about to receive more than VND 20,000 billion.” The June 18 Vinhomes article explicitly states Vingroup’s ownership and the estimated cash it could receive, so the nearly VND 18,000 billion figure is grounded in the latest disclosed source.CafeF

That is not yet true for Vincom Retail. The June 18 article confirms the total dividend pool, but it does not state Vingroup’s current ownership in the same piece. Without a same-period source that verifies the stake, the more defensible approach is to say that VRE is also paying cash while stopping short of assigning a confirmed amount back to VIC. It is a small distinction in wording, but a major one in terms of credibility.

That distinction shifts the story from “is this a high dividend?” to “what does this cash do at the parent level?” If Vingroup receives nearly VND 18,000 billion from Vinhomes and does not need to offset that inflow with fresh borrowing or new fundraising to meet near-term capital needs, the market has one more reason to reassess VIC’s balance-sheet flexibility. If the cash mostly passes through and is quickly absorbed by existing obligations, then the effect is more likely to stay in the realm of sentiment and short-term expectations.

Vinhomes is paying out cash while still expanding its capital base

What stands out in Vinhomes’ capital plan is that the company is not only paying cash. On the same June 30 record date, it will also issue a 100% stock dividend, or roughly 4.1 billion new shares, lifting charter capital to more than VND 80,000 billion.CafeF

That structure shows Vinhomes doing two things at once. First, it is distributing a very large amount of cash to shareholders. Second, it is still expanding its nominal capital base through shares. For experienced investors, that combination is familiar. For first-time investors, the important point is that cash dividends and stock dividends serve different purposes: one distributes earnings, the other reshapes the capital base on paper.

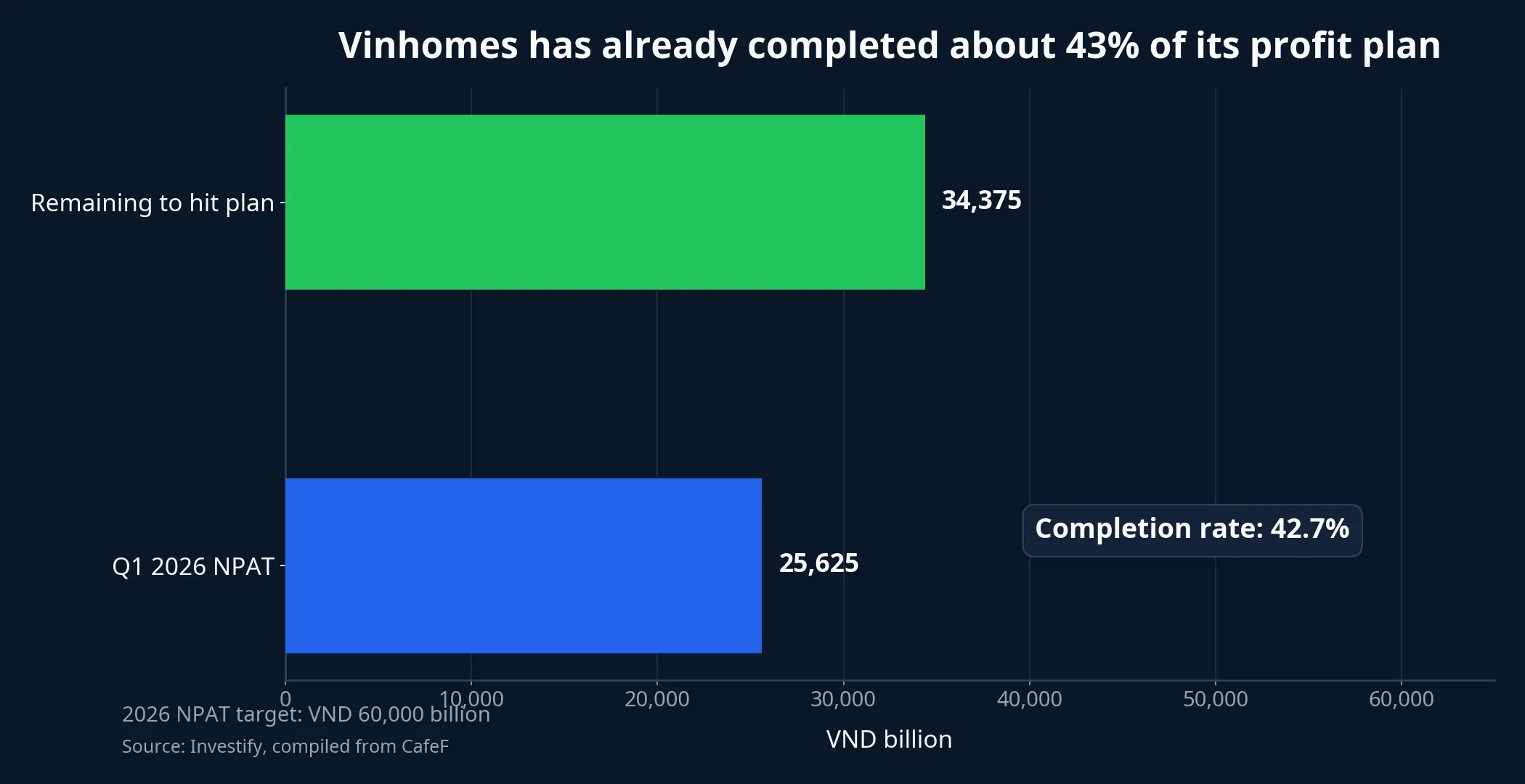

The operating backdrop is also strong enough to support that decision. Vinhomes is targeting VND 285,000 billion in revenue and VND 60,000 billion in net profit after tax for 2026, up 86% and 38% from the prior year. In Q1 2026 alone, consolidated net revenue reached VND 65,114 billion and net profit after tax came in at VND 25,625 billion, equal to about 23% of the revenue target and 43% of the annual profit target.CafeF

Completing 43% of the annual profit plan after one quarter does not guarantee the full year will land exactly on target. It does, however, show that Vinhomes entered 2026 with a profit base strong enough for the market to view a large cash payout as an allocation choice rather than a forced extraction. The real story here is still the company’s ability to generate cash, not just its willingness to distribute it.

VRE is sending a different signal

If Vinhomes represents the ecosystem’s large-scale profit engine and cash distributor, Vincom Retail is sending a different message. According to the June 18 report, this is VRE’s first cash dividend since 2019.CafeF

That matters because it says something about the confidence of the retail-mall business after a long period in which retaining cash and reinvestment mattered more than paying shareholders. The same source says VRE is targeting VND 10,132 billion in consolidated net revenue and VND 5,375 billion in net profit after tax for 2026, up 16% and 15% from the comparable 2025 targets after excluding non-recurring income. After Q1, adjusted consolidated net revenue stood at VND 2,574 billion and net profit after tax at VND 1,606 billion.CafeF

For VRE, the market is reading more than just “the company has enough cash to pay.” It is also reading “the core business is stable enough to resume paying.” That is a higher-quality signal than a dividend ratio viewed in isolation because it is tied to the operating health of the retail asset base. Even so, that signal should stay within VRE’s own story unless a source confirms how much of it belongs in VIC’s.

What the market should watch next

Before the June 18 session, VIC traded at VND 192,000 per share, VHM at VND 135,000, and VRE at VND 28,150, while the VN-Index stood at 1,806.20 points after falling 1.74 points in the previous session. Those price levels show that the Vingroup complex is no longer being valued from a low-expectation base, so any information about capital and cash flow carries more weight in how the market prices the group.CafeF

The cleanest conclusion for now is that this dividend cycle strengthens the case for better capital flexibility at VIC, but the firm evidence is still concentrated in the nearly VND 18,000 billion linked to Vinhomes. VRE adds another positive signal inside the ecosystem, yet the source article does not provide enough ownership detail to treat it as a confirmed inflow to the parent. In short, this is a positive signal with a clear center of gravity, not a blanket promise for the entire group.

That is also why the next checkpoints are concrete rather than abstract. The market will be watching how VIC uses the cash it receives, whether capital pressure genuinely eases, and whether upcoming quarterly reports show a real shift in the balance sheet or simply a one-off distribution after a strong year. Those answers will determine whether this is merely a large dividend headline or a meaningful step in Vingroup’s capital cycle.