The 3.5%-3.75% policy band on June 17 was not the part that unsettled Wall Street most. What forced investors to rewrite the script was the combination of unchanged rates today and a higher inflation outlook for the rest of 2026. For newer investors, that distinction matters: markets usually move less on the decision that just happened than on the policy path that now looks more likely.Fed

This meeting did not tell a clean “the Fed is about to hike immediately” story. It told a more uncomfortable one: cheap money is still farther away than many investors hoped. Once that becomes the base case, growth stocks, longer-duration bonds, and even defensive assets all need to be repriced.

What Markets Actually Had to Reprice

In its post-meeting statement, the Fed said the US economy was still expanding, the labor market remained solid, and inflation was still well above the 2% target. That language matters because it signals the central bank does not yet see enough economic weakness to justify a turn toward easier policy. If growth is slowing only modestly, policymakers can afford to stay patient with higher rates.Fed

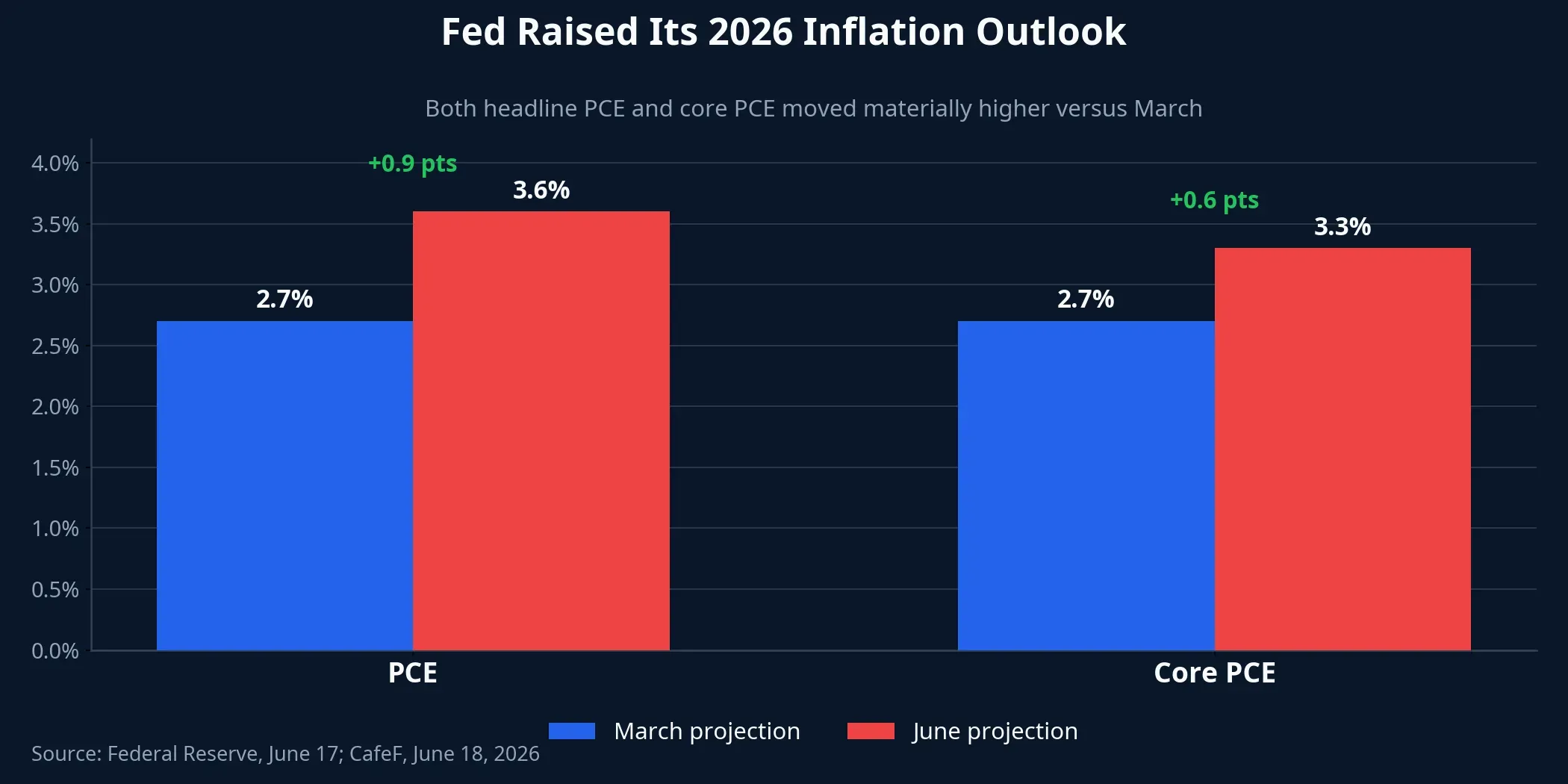

The more important shift came in the new projections. The Fed lifted its 2026 personal consumption expenditures inflation forecast to 3.6% and core PCE to 3.3%, while the median year-end policy-rate projection rose to 3.8%. CafeF’s June 18 recap highlighted how different that was from the March baseline, when both PCE and core PCE were projected at 2.7% and the year-end rate path was still at 3.4%.FedCafeF

The bigger picture is that the Fed has shifted from “holding steady but gradually softening” to “holding steady and ready to stay tougher if inflation refuses to cool.” That is a change in direction, not a technical tweak inside one meeting. For investors, it changes the key question for the second half of the year: not whether the Fed will hold or hike at the next meeting, but whether inflation will cool fast enough to keep further tightening off the table.

One reason markets cannot simply price in an imminent easing cycle is that the Fed is still not describing a recession. The central bank’s 2026 real GDP projection now sits at 2.2%, while unemployment is seen at 4.3%. That is softer growth, but it is not the profile of an economy that is breaking hard enough to force policy relief.Fed

Why Stocks and Bonds Both Felt the Pressure

US equities sold off first. The Guardian reported that the Dow Jones fell by roughly 500 points, while both the S&P 500 and the Nasdaq dropped more than 1.2% after the announcement. That move was not about an unexpected rate hike. It was about investors marking down the odds that easier policy would return soon.Guardian

Growth stocks tend to be the most exposed to this sort of shift. Their valuations depend more heavily on profits that arrive years into the future, so a higher discount-rate path or a longer stretch of elevated rates compresses present values quickly. That is why the same Fed message tends to hit the Nasdaq harder than more defensive or value-heavy benchmarks.

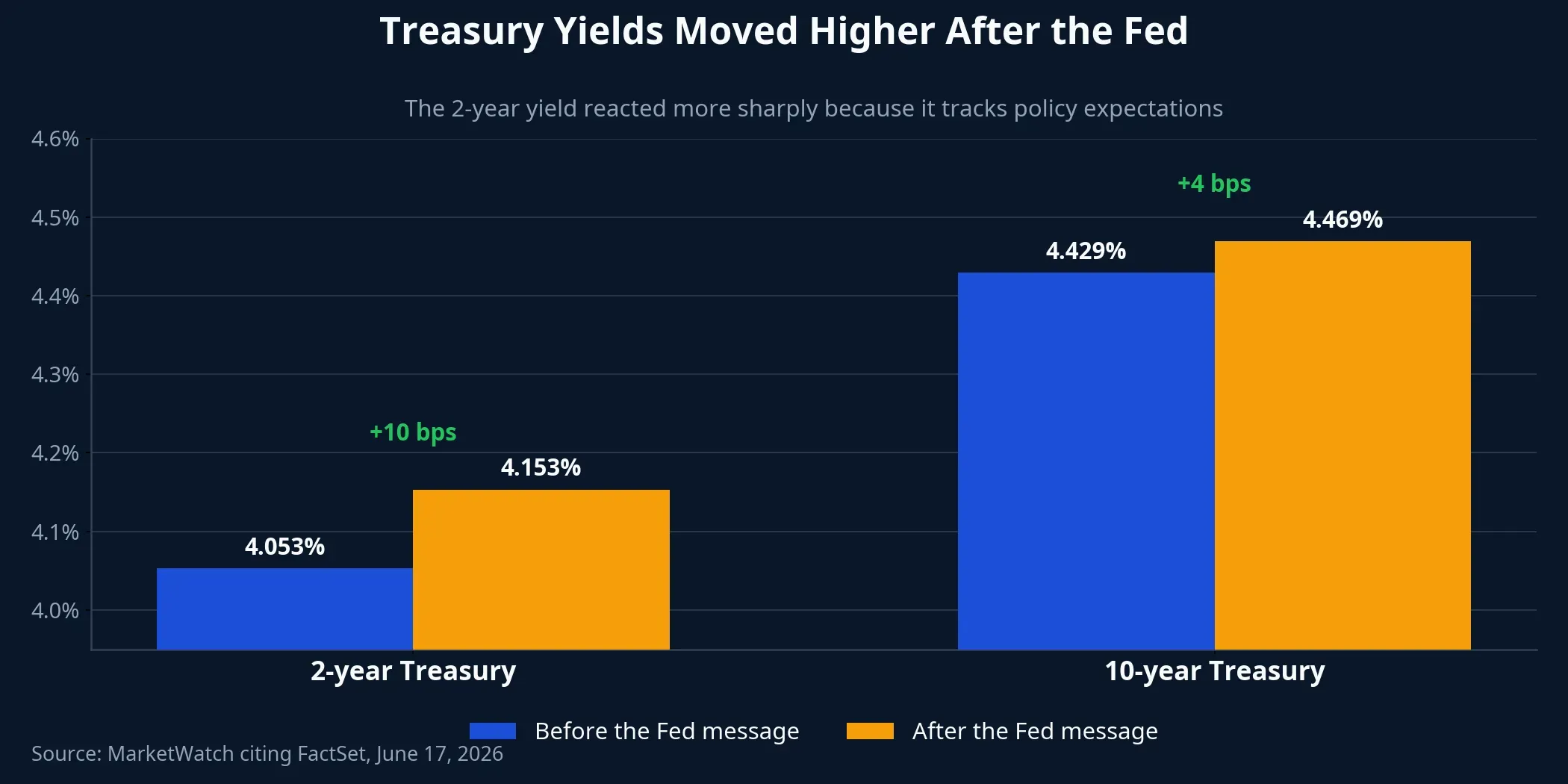

Treasuries reacted even more directly. MarketWatch, citing FactSet, said the 2-year Treasury yield rose about 10 basis points to 4.153%, while the 10-year yield rose about 4 basis points to 4.469%. The sharper move in the 2-year makes sense because that part of the curve tracks near- and medium-term policy expectations most closely.MarketWatch

As short-end yields move up, capital allocation changes with them. Assets offering fixed cash flow, shorter duration, and lower volatility start to look relatively more attractive than equities whose payoff depends on waiting much longer for earnings to arrive. Put differently, the Fed did not drain liquidity from markets overnight on June 17, but it did raise the price of waiting for future growth.

Gold, Oil, and the Inflation Question That Is Still Open

Not every asset class reacted in a straight line. Investify’s internal data showed spot gold was nearly flat on June 17 at USD 4,331.37 an ounce after rising 0.50% the previous session, while DXY stood at 99.52 and slipped 0.19% on the day. That combination suggests gold was not trading only on Fed expectations; it was also still drawing support from defensive positioning while the Middle East remained a live geopolitical risk.

That matters because gold alone does not confirm a clean “the market expects another hike” reading. Defensive demand is still in the mix, and the dollar did not surge in a way that would fully validate an immediate policy shock. A more balanced interpretation is that the Fed pushed the rate path higher while markets are still debating how persistent the current inflation pressure will be.

Oil is the key variable inside that debate. Investify’s internal data showed Brent crude falling from USD 111.28 a barrel on May 19 to USD 79.74 on June 17. If that cooling trend holds for several more months, the Fed could gain room to stay on hold rather than move higher. If energy prices rebound because supply risks return, the inflation channel the Fed is worried about becomes much harder to dismiss.

Three Paths for the Second Half

The first path is a gradual cooling in inflation, especially in energy and other geopolitically sensitive goods. In that case, the Fed could keep a firm tone without needing to act more aggressively, and markets could start adjusting to a world of high but stable rates. That is the most constructive outcome for equities because it would allow valuations to recover without requiring an immediate rate cut.

The second path is stickier inflation. If that happens, the repricing investors reluctantly accepted on June 17 may need to go one step further. Dropping the rate-cut narrative would not be enough; markets would have to reckon with the possibility of one more hike. CafeF’s summary of the dot plot said 9 officials still saw room for a hike this year, 8 leaned toward holding through year-end, and only 1 still projected a cut.CafeF

The third path is a sharper slowdown in growth than the Fed currently expects. If that scenario arrives, Treasuries would likely recover before equities because yields typically fall before corporate earnings stabilize. But that is not the scenario the Fed is describing today, which is why betting too early on a fast easing cycle still looks premature.

For Vietnamese investors, the practical takeaway is not to guess whether the Fed will hold or hike at a specific meeting. The more useful dashboard is PCE, core PCE, oil prices, and the 2-year Treasury yield. If those variables cool together, pressure on risk assets should ease. If they stay elevated, global valuations are likely to remain under strain for longer.

The cleanest conclusion from the June 17 meeting is that the Fed changed markets through expectations rather than through action. The most defensible thesis now is a higher-for-longer rate backdrop, with the odds of an early cut materially reduced. What could still change that picture is the next few months of inflation data, especially in energy and services.