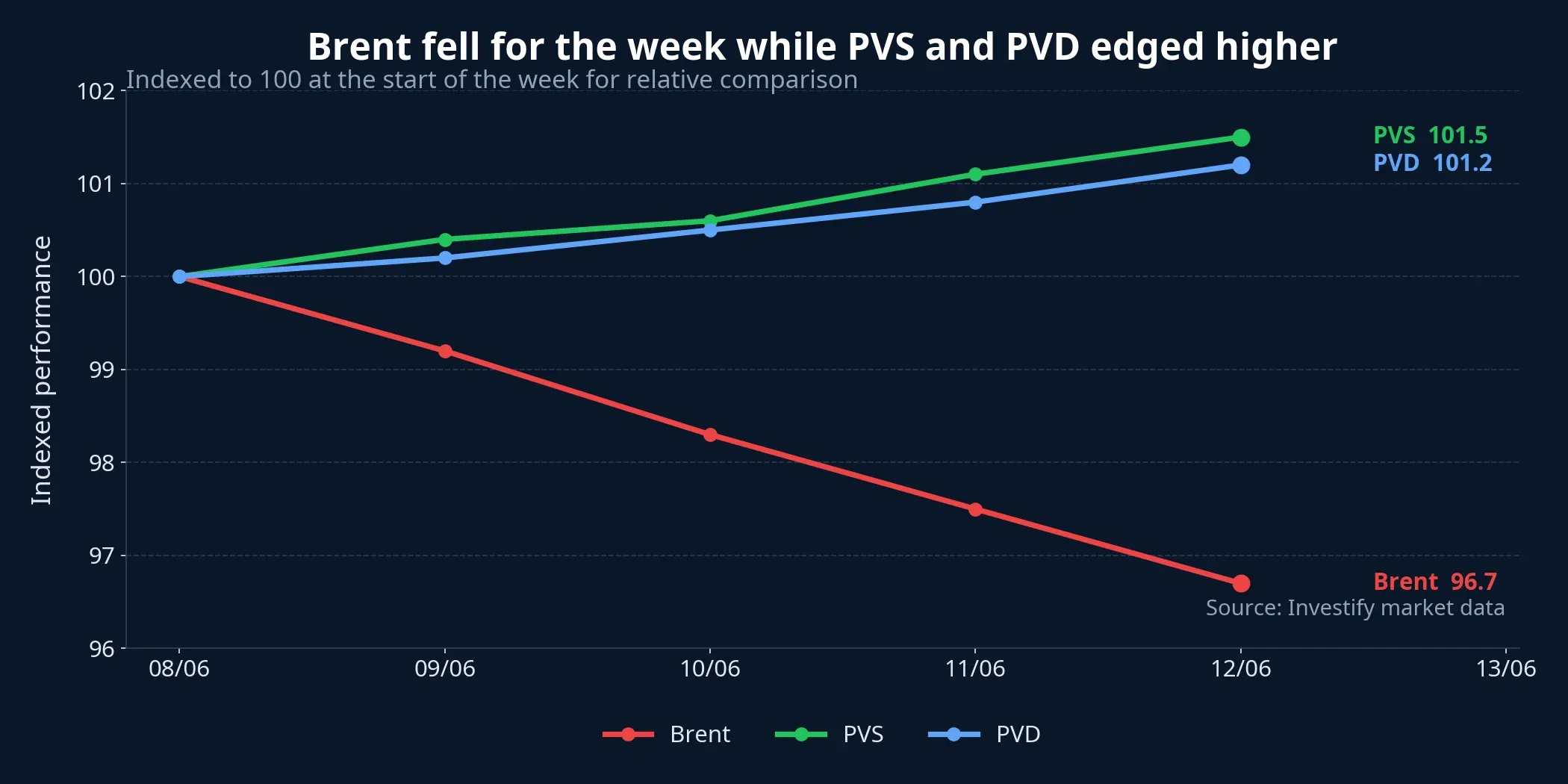

Newer investors often default to a simple rule: if oil goes down, oil stocks should go down too. That instinct is not entirely wrong, but it is too blunt for the whole energy chain. In the week ending June 18, Brent fell from USD 90.38 a barrel to USD 78.08, a decline of 13.61%. Domestic E5 RON92 gasoline prices also slipped from VND 21,330 per liter to VND 20,120, down 5.67%. Yet over the same stretch, PVS still rose from VND 38,600 to VND 39,000, while PVD climbed from VND 30,150 to VND 31,050.

That does not mean oil prices no longer matter. It means the label “oil and gas stocks” bundles together businesses that make money in very different ways. Put simply, some companies live off the price of the commodity itself, while others live off signed contracts, project milestones, and execution. If investors fail to separate those models, they can buy the same sector label for completely different reasons and end up reading the story wrong.

Why Brent alone is not enough

For upstream producers, refiners, or fuel distributors, Brent usually feeds into earnings much faster. A move in crude can change product spreads, inventory economics, selling prices, and full-year profit expectations. If oil falls hard enough and stays lower long enough, the market has a clear reason to cut its outlook for that group.

Oilfield services work differently. PVS does not sell barrels of oil to end customers. Its core business sits in mechanical fabrication, offshore construction, floating storage, ports, service vessels, and broader energy infrastructure. For companies like this, earnings tend to track signed contracts, billable workload, and the timing of project acceptance rather than every daily move in Brent.

PVD sits closer to the commodity cycle than PVS does, but even there the transmission is not instantaneous. Drilling demand depends on exploration and production budgets set by field operators. When oil stays high for long enough, new drilling plans become easier to justify. When oil stays weak for long enough, those budgets can be reviewed. That lag is the key.

The market is reading PVS through backlog

At its June 18 annual general meeting, PVS said first-half consolidated revenue was estimated at VND 15,815 billion, up 13% year on year, while net profit was estimated at VND 627 billion, up 2%. The company also set a 2026 consolidated revenue target of VND 33,000 billion and a net profit target of VND 990 billion.VietnamBiz

The key point is not whether the stock gained 1% or 2% in a week. The more important point is that the company has already turned enough workload into revenue to cover nearly half of its annual plan by midyear. That is the kind of signal investors tend to use when repricing a service contractor. The question is less “where is oil today?” and more “how much of the booked work is actually moving?”

The project list PVS disclosed helps explain why this story cannot be read off spot oil alone. In the Block B chain, the company said EPCI 1 was about 65% complete, EPCI 2 was 95% complete, the onshore O Mon - Ca Mau pipeline was 40-45% complete, and the FSO package was around 45% complete. In offshore wind, offshore substation packages for Baltic Power were 97% complete, Fengmiao was 95% complete, and Hai Long 4 was above 60%.VietnamBiz

This is the workload book investors need to read. Once a project is already at those milestones, a one-week drop in Brent is not enough to erase revenue that is already being executed and recognized. That is why the market can afford to look past a short-term oil slide as long as workload and delivery schedules remain intact.

There is also a medium-term layer to the story. PVS is targeting consolidated revenue of VND 60,000 billion by 2030. A separate report from Tạp chí Công Thương said management is aiming for VND 210,000-220,000 billion in revenue over 2026-2030, equivalent to roughly USD 7.9-8.3 billion.Công Thương That is not a guaranteed growth outcome, but it does give the market a reason to frame PVS as a multi-year energy infrastructure contractor rather than a stock that should simply track Brent day by day.

PVD still needs Brent, just not in real time

If PVS is mostly a backlog and execution story, PVD sits closer to the drilling cycle. Oil prices that stay high for long enough make it easier for field operators to add drilling plans, extend rig contracts, or raise exploration budgets. Lower prices matter too, but mainly when they persist long enough to change those decisions.

So PVD rising about 2.99% in a week when Brent fell is not proof that oil no longer matters to the company. It only suggests that, in the near term, investors may be focusing more on rig utilization, day rates, and the odds that contracts remain in place. For a drilling contractor, that is the more direct path into earnings.

The difference between PVS and PVD is therefore one of sensitivity. PVS can still be hit indirectly if lower oil eventually slows major projects, but the first read usually comes from the work already in hand. PVD is closer to the industry’s capital spending cycle, so if Brent stays weak for several more weeks or months, pressure on drilling expectations would become more visible.

What newer investors should actually watch

If you trade the whole oil and gas complex off a single Brent line, you are using a very short ruler to measure a very long value chain. For companies that sell oil products, commodity prices and product margins are central. For oilfield services, the better indicators are backlog, new contract value, execution milestones, project disbursement, and margin resilience when input costs move.

PVS itself offered a useful reminder that the story is not one-directional. The company said a 10% rise in fuel costs could cut profit by about 3%.VietnamBiz In other words, higher oil is not automatically good news for a service contractor, because oil can be both an industry investment signal and an input cost.

That is why the right framework is not “oil up means buy, oil down means sell.” A better framework is to separate companies by how they earn money. Once investors know whether a business lives off commodity pricing or off contracted workload, they are less likely to get dragged around by the market’s first reflex.

What the conclusion should be

The clearest takeaway from this week is that the market does not yet see a one-week drop in Brent as enough to rewrite the story for oilfield services. For PVS, the bigger focus remains the work already under execution and the visibility of delivery milestones. For PVD, Brent still matters, but the impact becomes more meaningful if lower prices last long enough to change drilling plans at the operator level.

So the next question is not simply whether oil rises or falls a bit more. The more important questions are whether project execution keeps its pace, whether drilling contracts remain stable, and whether Brent has been weak long enough to force operators to revise their plans. Answer those three questions well, and it becomes much easier to understand why stocks under the same “oil and gas” label can react so differently.