When a large IPO draws in a long list of funds, the instinctive retail reaction is simple: if professional money is buying, the trade must already be safe. That instinct is understandable. It feels a bit like walking into a crowded restaurant and assuming the hard work has been done for you. In an IPO, though, that logic only gets you halfway.

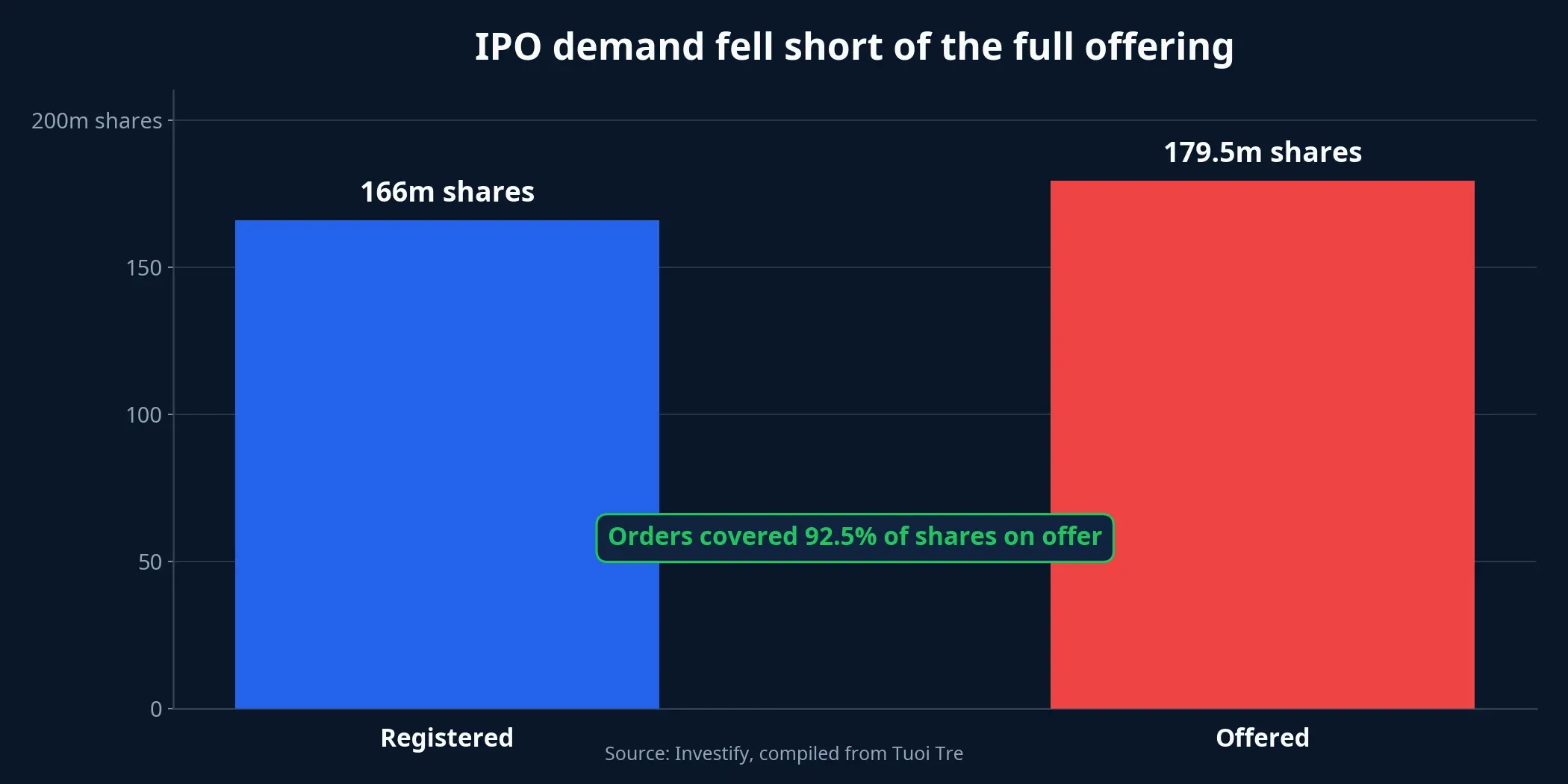

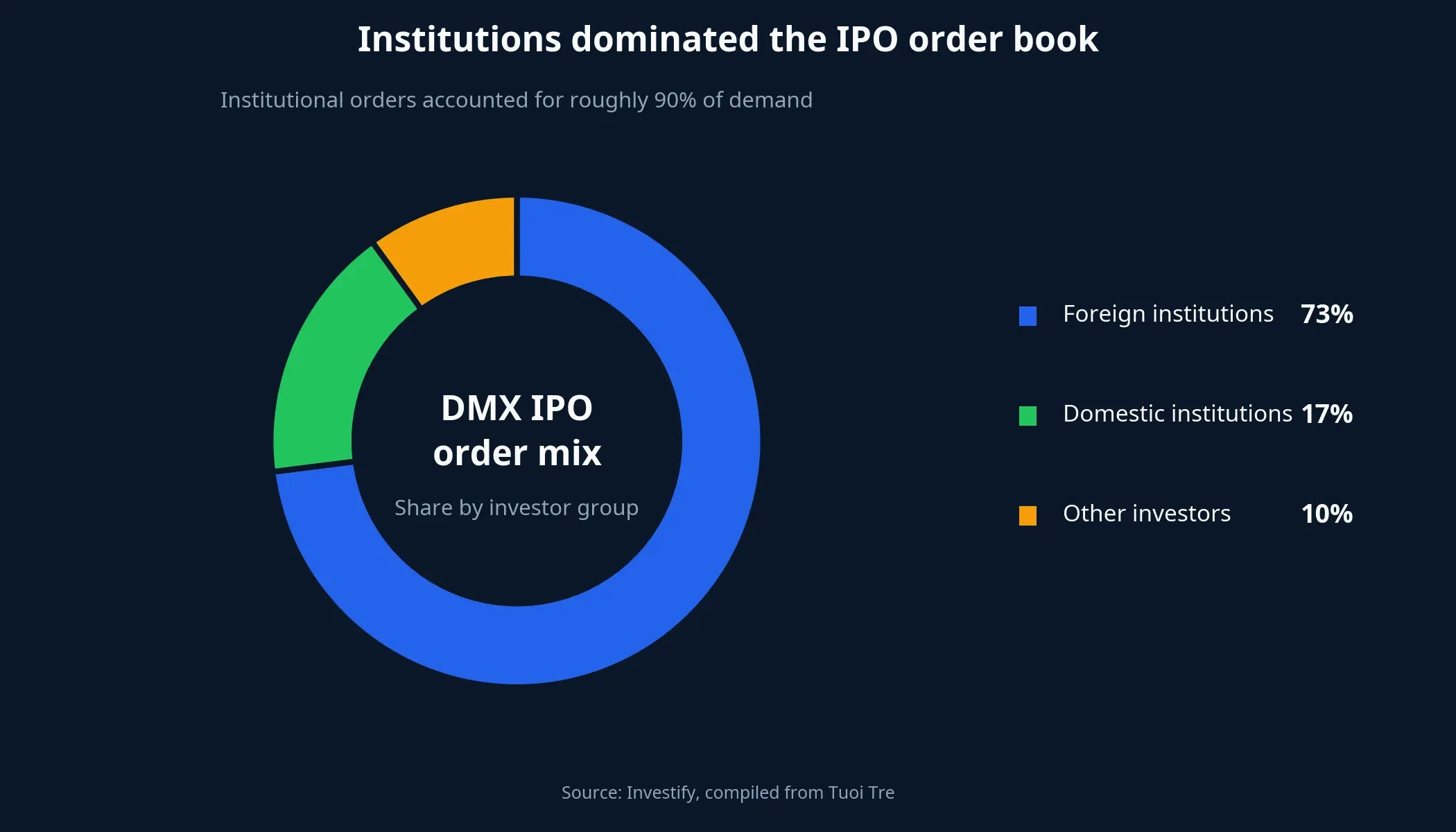

Dien May Xanh is a useful case study. The offering closed with orders for more than 166 million shares, equal to roughly 93% of the shares on offer. Institutional investors accounted for about 90% of total demand, with foreign institutions taking around 73% and domestic institutions around 17%.Tuổi Trẻ That tells you the IPO file was strong enough to attract serious underwriting work and capital. It does not tell you that buyers in the secondary market will enjoy the same margin of safety.

What strong fund participation actually confirms

Funds do not commit capital to a deal like this just because the brand is familiar to consumers. When a large IPO attracts mostly institutional demand, the signal usually sits elsewhere: market size, cash-generation ability, operating quality, and a growth story long enough to survive short-term volatility. Dien May Xanh’s deal already screens as large enough that professional investors would need to underwrite it carefully rather than chase it on sentiment alone.

The company offered more than 179.5 million shares at VND 80,000 each. If the book had been fully covered, the raise could have reached roughly VND 14,360 billion; with actual orders, the expected proceeds still come in at about VND 13,300 billion.Tuổi Trẻ That is not a deal size the market absorbs on excitement alone. When nearly 30 institutional investors, representing around 60 funds, join the order book, the cleaner reading is that the company has a growth profile worthy of serious due diligence.Tuổi Trẻ

In other words, institutions are answering one question: is this business worth studying at the IPO price? Retail investors usually care about a different one: will buying after the listing be an easy win? Those questions sound close, but they are not the same trade.

The operating story is good enough to draw long-term money

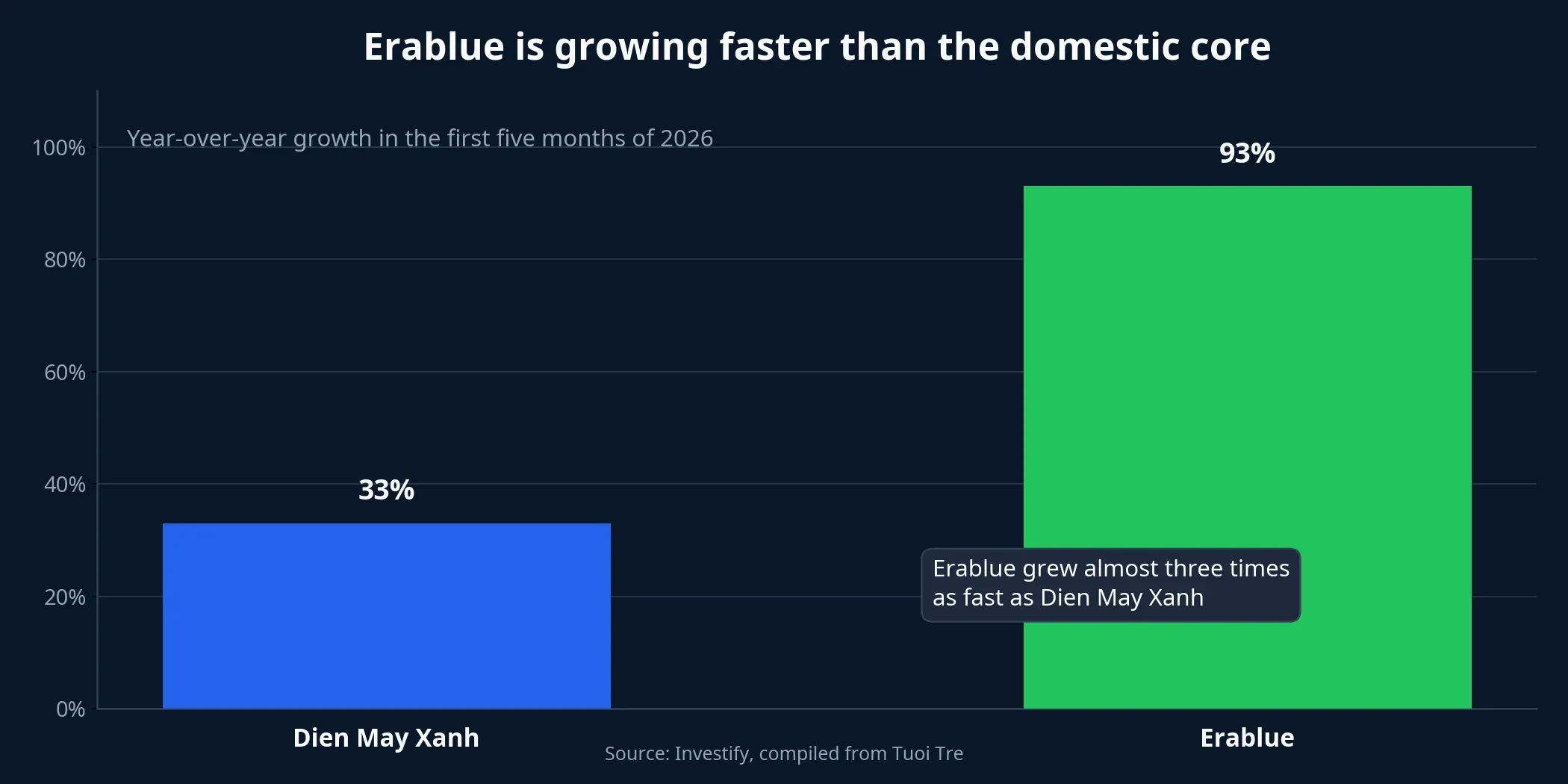

If you look only at the order book and ignore the business underneath it, you will misread why institutions showed up. Dien May Xanh did not come to market with a hollow narrative. In the first five months of 2026, the company reported consolidated revenue of VND 54,644 billion, up 33% year over year and equal to roughly 45% of its full-year plan.Tuổi Trẻ That matters because it shows growth is already visible in operating data, not just in a slide deck.

The more interesting leg is the overseas expansion story. In Indonesia, EraBlue posted revenue of IDR 1.56 trillion, or about VND 2,260 billion, up 93% from a year earlier. By the end of May 2026, the chain had 245 stores and was targeting 500 stores by 2027.Tuổi Trẻ For long-horizon investors, this is the part that can justify a broader valuation framework, because it gives the company a second growth engine beyond its established domestic retail base.

That distinction matters for newer investors. Many retail buyers see heavy fund participation and assume institutions already know the stock will rally once it hits the exchange. More often, funds are underwriting a two- to three-year story: can the company sustain growth, expand profit pools, and keep compounding cash flow? That is a much longer time frame than the usual hope for a quick listing-day trade.

What institutional demand does not tell you

This is where most retail misreadings happen. Strong institutional interest does not mean secondary-market demand will stay strong at every price level. Even in this IPO, nearly 14 million shares went unsubscribed, equal to about 7.5% of the offer size.Tuổi Trẻ That detail does not negate the appeal of the deal. It does remind you that VND 80,000 per share is still a price point the market is testing rather than embracing without reservation.

The market mechanics also change completely after listing. During the IPO process, investors have time to read the file, think through allocation, and wait for the stock to start trading. Once the shares list on HoSE, price will be set by day-to-day supply and demand, short-term sentiment, profit-taking pressure, and the willingness of later buyers to accept the opening valuation. A strong business does not automatically mean the listing-day price will be easy to buy.

After the offering, Dien May Xanh is expected to have more than 1.28 billion shares outstanding. At the IPO price, implied market capitalization would rise above VND 100,000 billion, or close to USD 3.9 billion, at listing.Tuổi Trẻ Size helps a stock win attention, but it does not guarantee deep liquidity in every session. For a retail buyer, what matters much more is free float, how shares are actually allocated across investor groups, and how willing early holders are to sell once trading begins.

So the correct takeaway is not “funds lined up, therefore retail buyers can relax.” It is closer to “funds validated the IPO file at the offer price.” The gap between those two ideas is where new investors usually pay tuition to the market.

What retail investors should watch before August

Under the current plan, DMX is expected to list on HoSE in August 2026.Tuổi Trẻ Between now and then, three layers of information matter more than simply counting how many funds joined the book.

The first is tradable supply. Investors should look for the actual free float after the IPO, the final allocation split across investor groups, and any transfer restrictions if they exist. Those details do more to shape listing-day behavior than promotional language around demand. A stock can have a strong operating story and still open into a choppy tape if freely tradable supply is larger than the market expected.

The second is fresh operating data ahead of listing. The key question is not just whether Dien May Xanh posted strong numbers in the first five months of the year, but whether that momentum holds into the next reporting window. If revenue, margins, or the overseas expansion story continue to strengthen, the market has more reason to accept a richer valuation. If the pace cools, the exact same offer price may start to look more demanding.

The third is the state of the market when trading begins. On June 18, MWG closed at VND 78,700 per share, while the VN-Index finished at 1,830.47. That backdrop suggests the market still has room for recovery, but stocks in the same ecosystem do not have to move in lockstep with the broader index. A newly listed name is often even more sensitive because the market is discovering both the price and the narrative at the same time.

The cleanest framework for a newer investor is to separate this deal into three tests. First, test the business: Dien May Xanh has enough scale, growth, and regional expansion to deserve serious attention. Second, test the price: VND 80,000 in the IPO does not mean the stock will automatically be attractive at every trading price after listing. Third, test the trading risk: buying after listing is fundamentally different from receiving an IPO allocation.

The most coherent conclusion here is straightforward. Institutional money is helping validate the quality of Dien May Xanh’s IPO story, but it is not validating the safety of buying later in the public market. The constructive stance is on the company; the cautious stance is on post-listing entry price. What could change that view before August is new business data, the actual free-float profile, and how the market reprices the deal once DMX starts trading.