Vietnam’s carbon market just passed a milestone that can be easy to misread. Once broker names started showing up in approvals from VSDC and VNX, the natural instinct for first-time investors was to assume a new tradable product was about to hit the screen. That is not the main story. The real development is that the domestic carbon market has started to acquire real operating rails: trading, custody, settlement, and supervision.VSDCVietstock

Put simply, this looks more like a railway line completing its stations and signaling system than a retail frenzy beginning. A track can be ready before the public has a reason to board. In Vietnam’s case, the first users are emitting companies that need to manage allowances and carbon credits, while retail investors are still several steps away from anything resembling a familiar trading product.

From legal framework to operating system

The foundation rests on two major documents issued in 2025 and 2026. Decision 232/QD-TTg dated January 24, 2025 set the roadmap for Vietnam’s domestic carbon market, while Decree 29/2026/ND-CP, effective from January 19, 2026, laid out how the exchange should operate, from registration and custody to trading and settlement.Chính phủChính phủ

What matters here is that Decree 29 stopped treating carbon as a purely environmental concept. It pulled carbon into capital-market logic. Assets have to be centrally registered, trading has to run through a supervised system, ownership transfers have to be confirmed, and settlement has to follow a formal workflow. According to Báo Đầu tư, HNX is assigned to organize trading, while VSDC is responsible for custody, ownership transfer, and settlement on the domestic carbon exchange.Báo Đầu tư

For beginners, that distinction matters because two different ideas often get mashed together. One is the policy push to reduce emissions. The other is the financial infrastructure that allows emission rights and carbon credits to change hands legally. When brokers enter the picture, carbon is not becoming a stock. A new asset class is simply being placed on a market machine that investors already recognize.

What the June approvals actually tell us

Short headlines can make it sound as if five brokerages are already “trading carbon.” That is not the precise reading. Based on announcements posted on VSDC’s website, VNDIRECT was approved to join the carbon custody and settlement system on June 15, 2026, while names including VPS, VietinBank Securities, DNSE, and PSI were added to the same system on June 17 and June 18.VSDC

At a different layer, Vietstock reported that VNX approved DNSE, VNDIRECT, and VietinBank Securities to participate in the carbon trading system on June 17, 2026.Vietstock VNDIRECT separately disclosed that it had received VSDC approval under Official Letter No. 7411/VSDC-LKCK.NV dated June 15 and VNX approval under Decision No. 31/QD-SGDVN dated June 17.VNDIRECT

That leads to a simple but important conclusion. Five securities firms have entered the custody and settlement layer, while three have been approved at the trading layer. That is a better reading than flattening every participant into the same status. In a new market, being allowed to hold assets, settle cash, and place orders are different functions, with different responsibilities and different readiness requirements.

Why the system runs on stock-market infrastructure

The logic is straightforward. If a company holds emissions allowances or carbon credits, the market has to know where those assets sit, whether they have been deposited, whether they have moved to a new owner, and whether the cash side has settled. Those are the same operational questions a securities market handles every day. Using HNX, VSDC, and member firms is therefore the fastest path from legal design to real execution.

According to Báo Đầu tư, companies can use accounts at securities firms to trade emissions allowances and carbon credits, but the carbon component has to be tracked and accounted for separately, without cross-netting against ordinary securities transactions.Báo Đầu tư In other words, the market may share an operating chassis with securities, but it does not share the same asset bucket. That is a useful corrective to the assumption that retail investors will soon buy carbon the same way they buy an ETF.

Circular 48/2026/TT-BTC, issued on May 12, 2026, shows that the carbon exchange is not merely about order matching. It places monitoring responsibilities on VNX, HNX, and trading members, including surveillance of unusual trades, misleading information, and manipulation risks.LuatVietnam In a new market, the first question should not be whether there is a tradeable “wave.” It should be whether the supervision architecture is credible enough to support one later.

The first assets belong to emitting companies

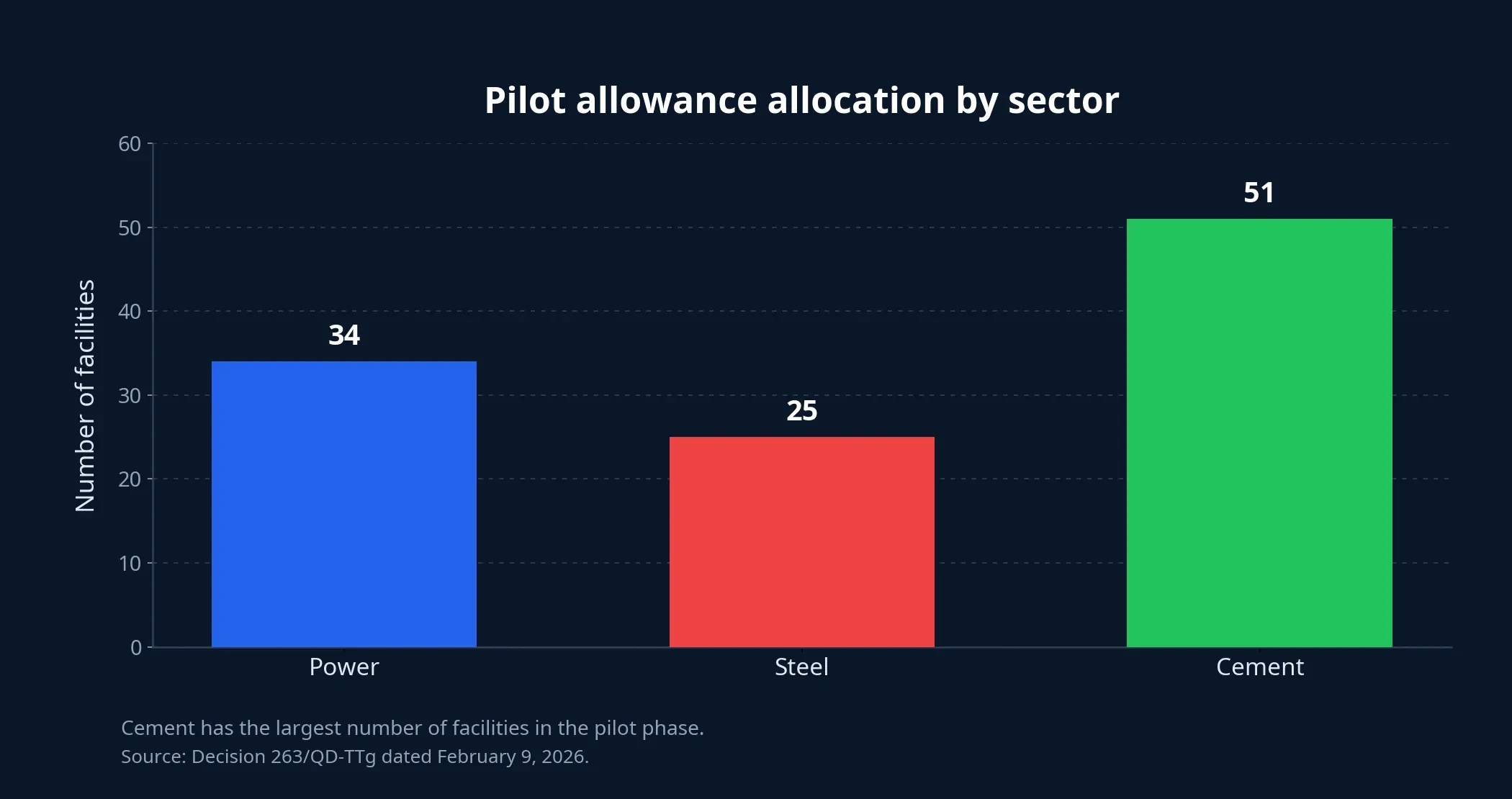

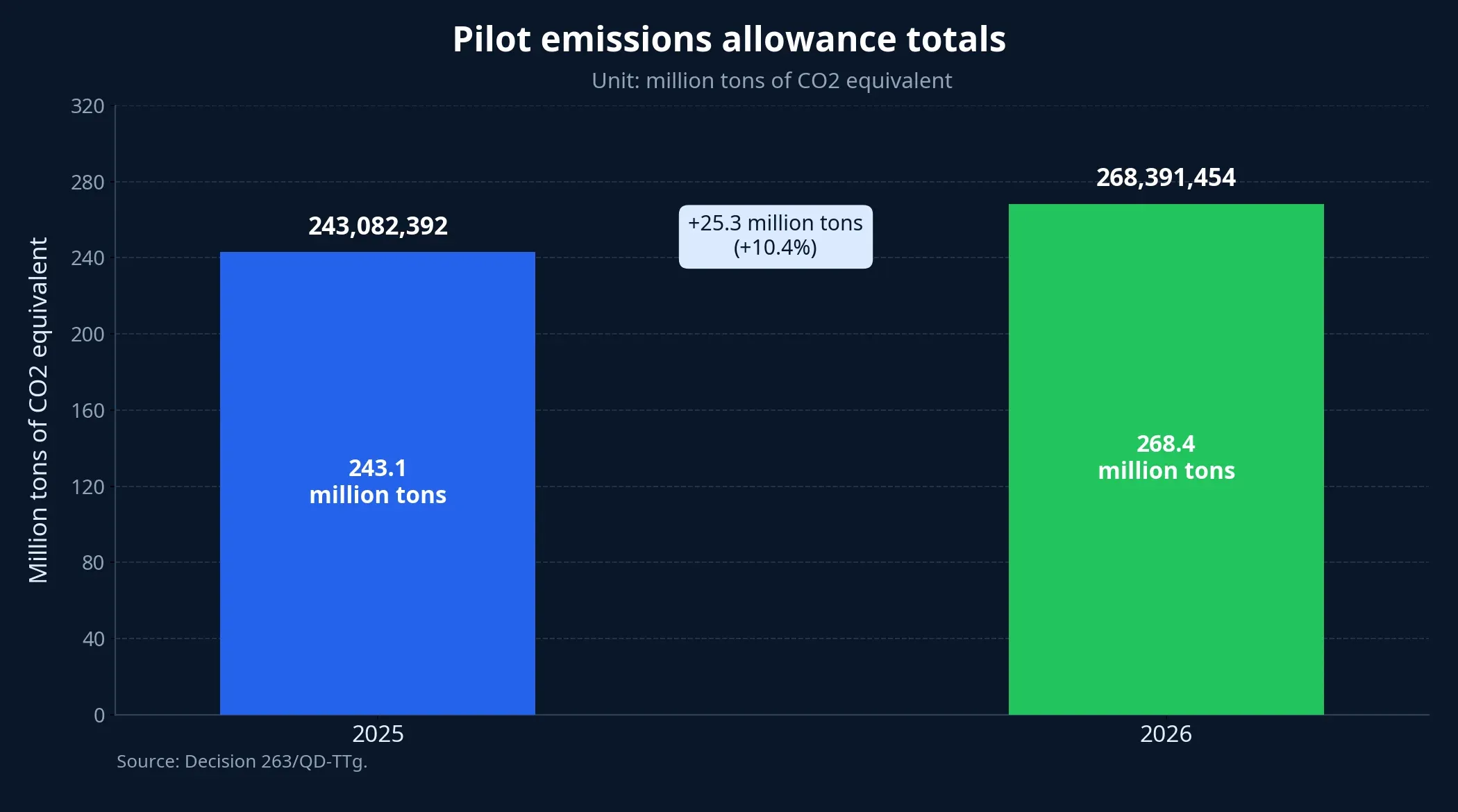

The most overlooked part of the story is the underlying asset itself. Decision 263/QD-TTg dated February 9, 2026 approved pilot greenhouse-gas allowance totals for 2025 and 2026, allocating them to 34 thermal power plants, 25 iron and steel facilities, and 51 cement facilities.LuatVietnam

The total allowance pool stands at 243,082,392 tons of CO2 equivalent for 2025 and rises to 268,391,454 tons of CO2 equivalent for 2026.LuatVietnam Those are structural figures, and they tell you the early carbon market was designed first for heavy-emitting sectors rather than for broad retail participation.

From an investment perspective, the first impact therefore runs through company financials more than through a retail quote screen. A steel, cement, or power producer that emits less than its allocation may end up with assets to sell. A company that overshoots its allowance will have to buy more permits or spend capital on cleaner technology. The same policy can become a cost line for one business and a margin cushion for another.

That is why carbon is not just an environmental story. It reaches into compliance costs, capital expenditure, emissions-data quality, and even export competitiveness as green standards tighten. If retail newcomers want one place to watch from here, it is not a hypothetical carbon ticker. It is the notes on compliance cost, technology investment, and disclosure quality at the companies that actually emit.

How retail investors should read this moment

This is a good example of financial infrastructure arriving before mass-market opportunity. A meaningful infrastructure milestone does not automatically create an immediate retail trade. In Vietnam’s carbon market, the evidence still supports the thesis that the rails are being completed, not that a speculative wave has already started.

International comparison helps frame the point. EU carbon allowances were priced at EUR 79.71 on June 19, 2026, up from EUR 74.97 on May 19, 2026. That shows how emissions can become a daily priced asset once the market is deep enough. Vietnam is at a different stage. It is still building rules, connecting members, and testing transaction flows before depth of liquidity or broad participation become the main questions.

The bottom line is fairly clear. June marks a real step forward for Vietnam’s carbon market, but the first-order impact belongs to emitting companies and the institutions that operate the exchange. For newer investors, the most useful watch list is whether carbon costs begin to show up in corporate margins, which businesses look better prepared for emissions obligations, and how far HNX and VSDC can push the pilot market toward a more complete operating framework. That is where the investment story becomes more concrete.