Asia has become easy to misread at the headline level. Investors can see Japan’s Nikkei 225 above 71,000, South Korea’s KOSPI at another high, and calmer regional sentiment as oil prices cool. But that does not mean the region is moving as one trade. It means three separate stories are unfolding at the same time.

For newer investors, the key question is not which market looks strongest on the screen today. The more useful question is which engine is actually lifting each index, and which engine is still missing. If the drivers are different, the reversal risks will show up in different places too.

The big picture: same region, different trades

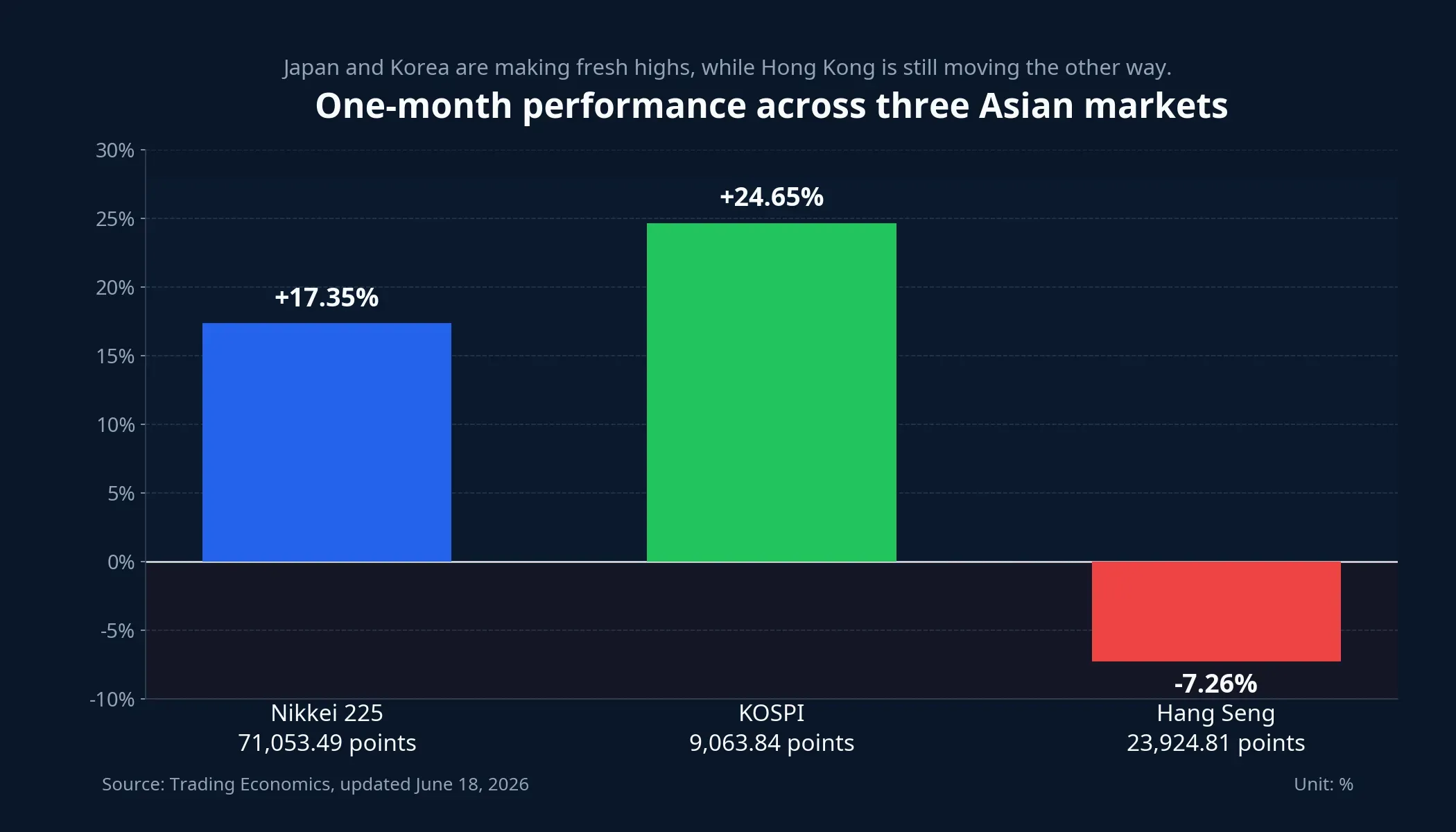

As of June 18, the Nikkei 225 was up 17.35% over one month, the KOSPI had gained 24.65%, and the Hang Seng had fallen 7.26%. The three indexes closed at 71,053.49 points, 9,063.84 points, and 23,924.81 points, respectively.Trading EconomicsTrading EconomicsTrading Economics

Put on a single chart, the divergence is hard to miss. Japan and South Korea are both advancing, but not for the same reason. Hong Kong sits on the other side of that picture, where investors still want clearer proof that China’s domestic economy can support a higher valuation.

Japan: lower energy pressure and electronics are working together

The Nikkei 225 closed at 71,053.49 on June 18, up 1.65% from the previous session and above both the 70,000 and 71,000 marks for the first time.NipponTrading Economics That matters because Japan is not just seeing a technical breakout. The index is moving in a phase where easing cost pressure and sector leadership are reinforcing each other.

For Japan, oil remains an important part of the backdrop. Brent stood at USD 78.08 per barrel on June 18, down 13.6% from USD 90.38 on June 11. For a major energy importer, softer oil prices usually ease concerns around input costs, corporate margins, and imported inflation. That is not the whole story, but it is clearly removing pressure at the right time.

The other part of the story is electronics and technology. Barron’s reported that Murata Manufacturing rose 8.1% and Tokyo Electron gained 4.7% on June 18, showing that money was not only chasing the headline index but also the stocks most directly tied to the technology investment cycle.Barron’s In other words, Japan’s rally is being supported both by lower energy anxiety and by companies with their own earnings narrative.

What investors should watch next is breadth. If the Nikkei keeps making highs but most of the lift still comes from a narrow group of electronics or financial names, that says something very different from a broader move across sectors. A record index level does not automatically mean the whole market is equally healthy.

South Korea: this is more a chip story than a regional story

The KOSPI rose 2.25% on June 18 and closed at 9,063.84.Trading Economics Compared with Japan, the engine behind South Korea is even clearer. This market is being driven by earnings expectations for semiconductors, especially companies linked to memory chips and AI infrastructure demand.

MarketWatch noted that Samsung Electronics, SK Hynix, and TSMC account for roughly 28% of the MSCI Emerging Markets index. That matters because when international money moves into emerging markets, a large share of that flow is effectively going into Asia’s semiconductor leaders.MarketWatch For South Korea, the upside case is relatively easy to read: if memory-chip pricing, order expectations, and AI-related capital spending stay supportive, the KOSPI still has a solid base.

But that strength comes with a very specific vulnerability. When an index is rising because one sector dominates it, the first reversal signal can come from that same sector before the macro data turn weak. If investors start to doubt the durability of the memory-chip cycle, or if earnings expectations are revised lower, the KOSPI can wobble sharply even while the broader Asia narrative still looks constructive.

That is why reading South Korea simply as “Asia is strong” misses the point. A more accurate frame is that this market is pricing confidence that the chip cycle still has room to run. As long as that thesis holds, the KOSPI has support. If that thesis weakens, the floor can disappear faster than many investors expect.

Hong Kong: the missing ingredient is still China’s domestic demand

The Hang Seng fell 1.59% on June 18 and remained 7.26% below its level a month earlier.Trading Economics This is the most important link if investors want to read Asia correctly right now. If oil is cooling and regional sentiment is less tense, yet Hong Kong still cannot keep up, that suggests this market is waiting for a different type of confirmation.

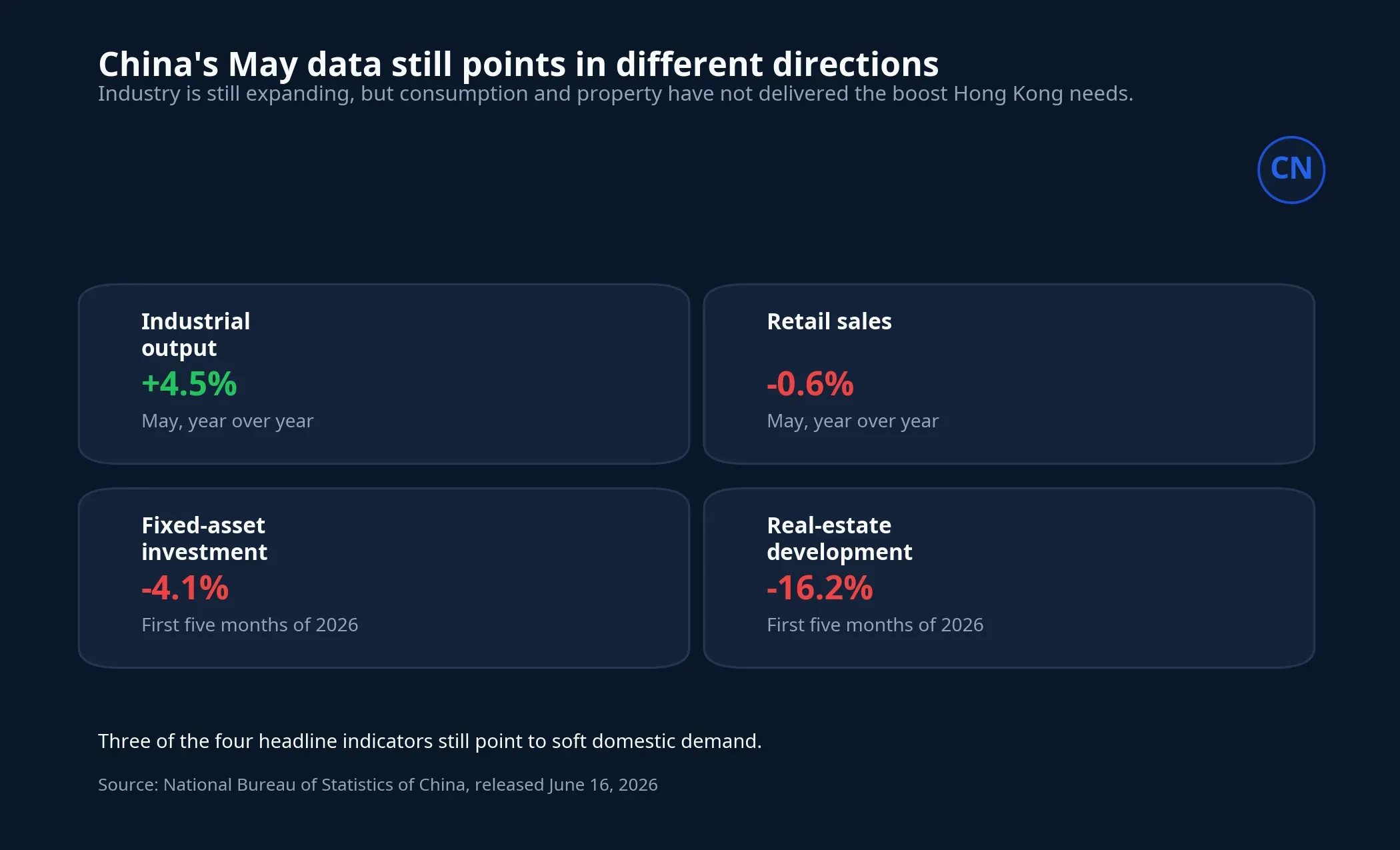

That confirmation sits in China’s data. A June 16 release from the National Bureau of Statistics of China showed May industrial output up 4.5% year over year, with high-tech manufacturing up 15.1%. But the same release showed retail sales down 0.6%, fixed-asset investment down 4.1% in the first five months of the year, and real-estate development investment down 16.2%.NBS China

The important point is that these numbers do not tell one clean story. Industry and high-tech manufacturing have not broken down, but consumption and property are still weak. For Hong Kong, where many listed companies are more exposed to finance, property, consumer demand, and mainland profit expectations, the weaker side of that dataset is the part that continues to cap valuations.

This is also where investors should avoid inference creep. It would be too strong to claim that the Hang Seng is weak because of one variable alone, since global risk appetite, ETF flows, and international positioning still matter. But if one explanation deserves the most weight based on the evidence in hand, it is that China’s domestic-demand story has not improved enough to pull Hong Kong into the same rhythm as Japan and South Korea.

What this means for fund and ETF investors

For Vietnamese investors buying regional funds or Asia-themed ETFs, this is the moment to drop the idea that “buying Asia” automatically spreads risk evenly. A Japan-heavy fund currently carries a large dose of energy-cost sensitivity, currency risk, and electronics exposure. A Korea-heavy fund may in practice be a concentrated bet on the semiconductor cycle. A fund with meaningful Hong Kong or China weight depends much more on whether consumption, property, and domestic policy support really turn higher.

That difference shapes the monitoring framework. If you own a Japan-heavy fund, oil and the yen still matter. If you own a Korea-heavy fund, chip earnings and order visibility are the main variables. If you own Hong Kong exposure, China’s economic releases and policy signals may matter much more than the general feeling that “Asia is green again.”

The higher-probability scenario from here

The higher-probability near-term outcome is not a clean regional rally where all of Asia rises together. A more coherent view is that the divergence continues: Japan keeps an edge from lower oil and electronics leadership, South Korea keeps moving with the chip story, and Hong Kong still needs more evidence from China’s domestic economy before it can stage a durable catch-up move.

The triggers that could change this picture are also fairly clear. If oil rebounds sharply, part of Japan’s support fades. If semiconductor earnings expectations are cut, South Korea loses its main pillar. And if China produces stronger consumption, housing, or policy support signals, Hong Kong would finally have a basis for joining the rest of the region.

So the real thesis is not “will Asia keep rallying or not.” The real thesis is that Asia is not one trade yet. As long as Japan, South Korea, and Hong Kong are still running on three different engines, investors need three different signal sets to read them properly.