Passenger growth does not automatically translate into profit growth. ACV is a useful case study for newer investors because infrastructure companies do not behave like retailers. They can serve more customers, put more assets into operation, and still report weaker short-term earnings when capital spending accelerates.

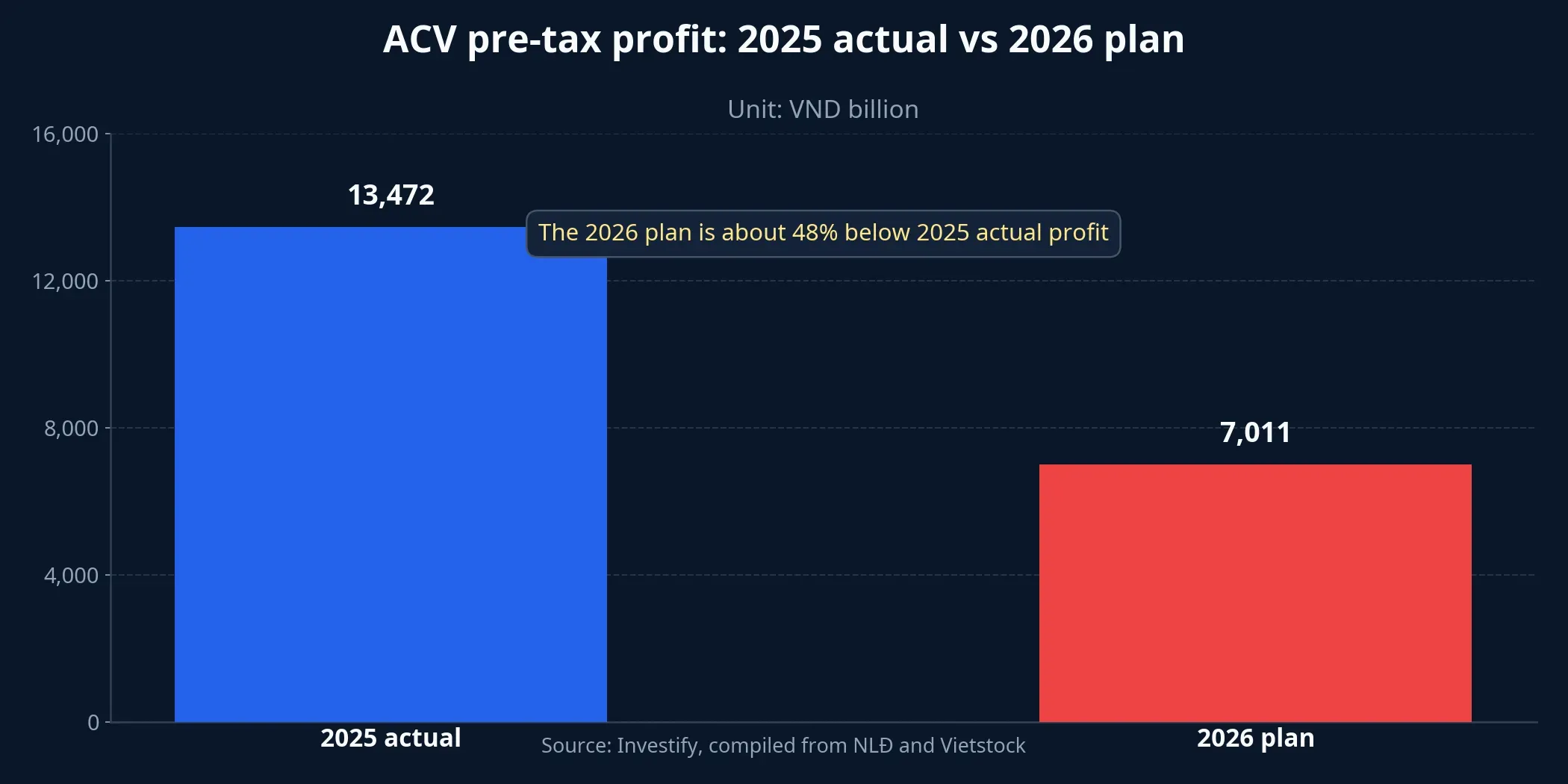

At ACV’s June 19 annual general meeting, the leadership change drew the headlines. But the more important takeaway sat in the numbers released alongside it. ACV is targeting 126 million passengers in 2026 and consolidated revenue of VND 21,141 billion, while planned pre-tax profit is only VND 7,011 billion.Vietstock In other words, traffic is still moving up, but profit is no longer following the same path.

The First Read: Where 2026 Looks Weaker

The gap becomes obvious when ACV’s 2026 plan is placed next to its 2025 result. Last year, the company handled 120.3 million passengers, posted VND 24,534 billion in revenue, and delivered VND 13,472 billion in pre-tax profit.NLĐ This year, the passenger target is roughly 6 million higher, but planned pre-tax profit is close to half of last year’s actual level.Vietstock

For a consumer business, that kind of mismatch might suggest weak demand. For an airport operator, the equation is different. Passenger volume matters, but earnings also depend on how quickly new assets start depreciating, how operating expenses scale up, and how much cash is being redirected into projects that are still under construction.

That is why this year’s annual meeting did not read like a demand slowdown story. It read like a company deliberately accepting lower near-term profitability while moving through a large capex cycle. For investors, especially those still learning how to read infrastructure names, that distinction matters. Traffic growth measures demand; profit growth measures how efficiently capital is being turned into cash returns.

Why Higher Traffic Is Not Enough

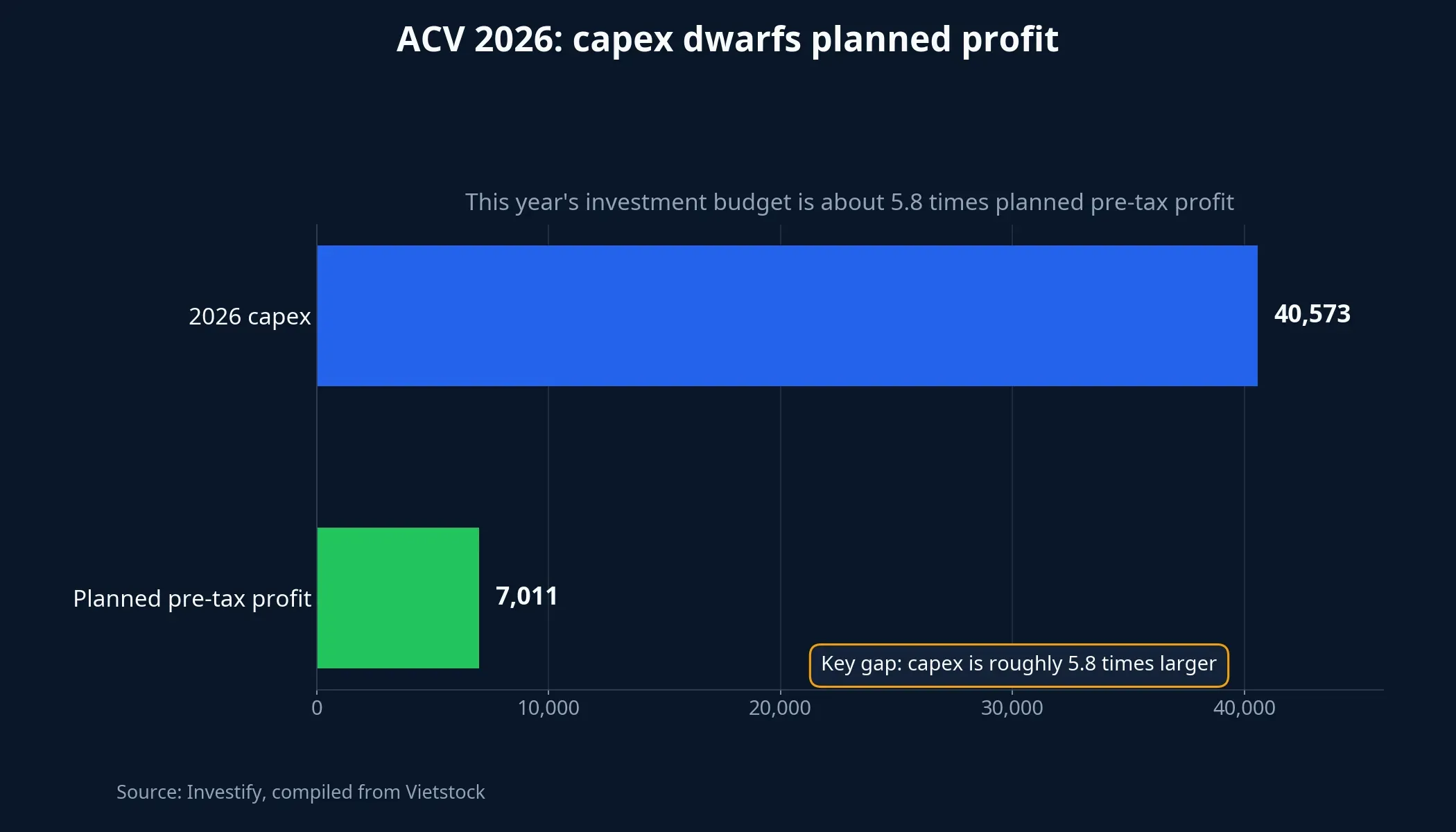

Management was fairly direct about the cost side. ACV plans roughly VND 40,573 billion in investment spending in 2026, while total costs could rise about 60% as major assets such as Tan Son Nhat’s T3 terminal, the expanded T2 terminal in Noi Bai, and Long Thanh move closer to completion or heavier operation.VietstockANTT

That ratio says a lot about what 2026 really is. It is not a year built around maximizing reported earnings. It is a year built around deploying assets. When large projects are not yet operating at full capacity, costs usually hit the income statement faster than revenue. Cash goes out first. The payoff arrives later, once terminals fill up, flight frequency rises, and spending per passenger improves.

First-half data shows the same timing mismatch. ACV estimates that it served 60.5 million passengers in the first six months, up 6% year on year. Consolidated revenue reached VND 10,745 billion, equal to 51% of the full-year plan, while pre-tax profit came in at VND 5,863 billion, or 84% of the annual target.Vietstock The 84% completion ratio looks strong at first glance, but it mainly reflects how conservatively the full-year profit target was set in the first place.

The constructive detail is that profit from core operating activities still held up. In the first half, pre-tax profit from core business lines reached VND 5,479 billion, up 4% from a year earlier and equal to 70% of the annual plan.ANTT That suggests ACV’s problem is not a lack of passengers. The pressure is coming from a new investment phase in which expenses are scaling up faster than newly added capacity can translate into accounting profit.

Long Thanh and the Time Lag of Big Assets

Long Thanh remains the core of the story. The project carries a total investment value of nearly VND 337,000 billion across roughly 5,000 hectares, with phase one designed for 25 million passengers a year.CafeF In the first quarter of 2026 alone, ACV disbursed around VND 800 billion more into the project, taking the cumulative construction investment there to above VND 35,000 billion.CafeF

This is not the sort of asset investors should expect to pay back on a quarter-to-quarter schedule. A new airport is not an extra storefront. The capital base is much larger, the build-out period is longer, and the economics only become attractive when flights, passenger traffic, cargo volumes, and ancillary services begin scaling together over time.

There are already signs that not every new asset is purely a cost burden. At the annual meeting, ACV said T3 has helped relieve pressure on T1 in Tan Son Nhat, while the expanded T2 terminal in Noi Bai has lifted international-terminal capacity to 15 million passengers a year. Occupancy has already moved above 70%, which management described as the profitability threshold for an international terminal.Vietstock

That matters because the current investment cycle has two sides. One is immediate cost pressure. The other is that, once the fill-up phase is behind them, these assets can meaningfully expand throughput and improve future margins. The long-term growth case for ACV only works if that ramp-up happens on schedule.

The Next Layer: Non-Aviation Revenue and Retained Earnings

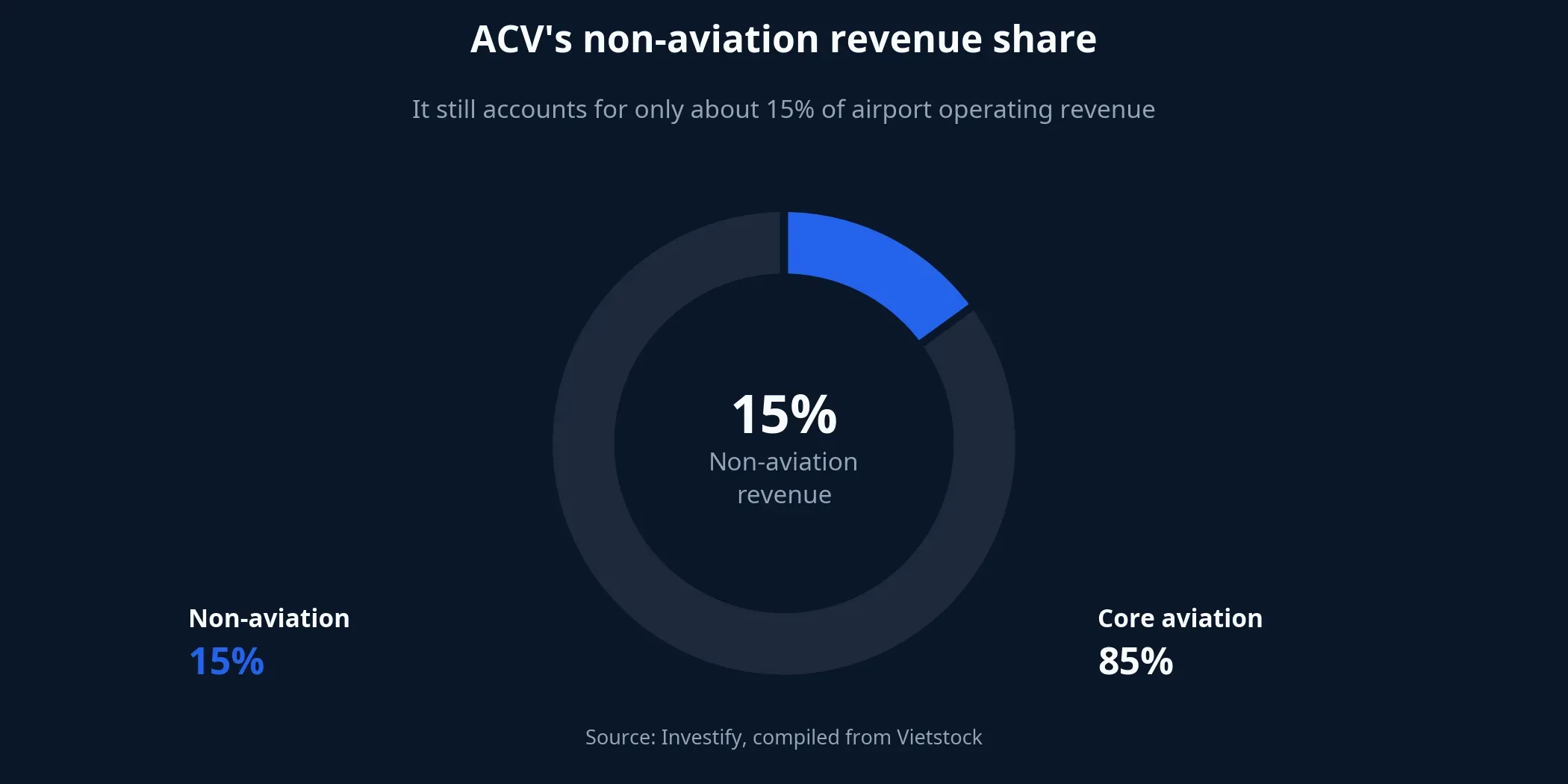

Another number worth watching is non-aviation revenue. According to Vietstock’s AGM coverage, it still accounts for only about 15% of ACV’s airport operating revenue.Vietstock The rest remains tied primarily to core aviation activities.

That split helps explain why ACV is not just a “more passengers equals more profit” story. In well-run airports, commercial rent, duty-free, advertising, food and beverage, and other terminal services often carry more attractive margins than the basic aviation business. If new terminals are adding foot traffic without meaningfully lifting non-aviation spend, returns on capital will take longer to improve.

Dividend policy reflects the same logic. ACV’s management said the company has retained earnings since 2019 to support large investment projects, and undistributed profit stood at roughly VND 12,684 billion at the end of 2025 after fund allocations.Vietstock The company is now seeking to raise charter capital through a stock dividend, while a return to cash dividends is being pushed back until investment needs ease.Vietstock

For investors, that is a familiar infrastructure trade-off. Shareholders give up some short-term cash distribution in exchange for greater long-term operating capacity. That is not inherently negative, but it means ACV has to be judged against the speed at which those assets become productive, not simply on one year’s reported earnings.

How to Read ACV After the AGM

At its latest closing price of VND 44,200 per share, ACV carries a market capitalization of roughly VND 158.3 trillion. Those figures do not settle the valuation debate by themselves. What they do show is that the market is pricing a uniquely positioned infrastructure operator whose near-term efficiency is being compressed by unusually heavy capital spending.

The cleaner thesis after the AGM is not that a new chairman changes the story. The cleaner thesis is that ACV is moving through an accounting profit squeeze caused by investment, even as underlying passenger demand is still rising. If Long Thanh, T3, and T2 continue ramping up on schedule and non-aviation revenue gradually climbs from today’s 15% base, then the earnings pressure in 2026 may prove to be the cost of a longer growth runway.

The risk checklist is also fairly concrete. Investors should watch Long Thanh’s construction and disbursement pace, actual fill rates at the new terminals, and ACV’s ability to lift non-aviation revenue above the current mix. If those variables lag, the same new assets will keep weighing on depreciation and cash flow. If they land on schedule, 2026 may end up looking less like a weak-profit year and more like the transition year that reset ACV’s next phase of growth.